2026 How Parents Can Compare Student Loan Offers

Student Finance & Loan Expert

Many parents face uncertainty when evaluating multiple student loan offers for their children. The terms, interest rates, repayment options, and potential fees can vary widely, making it difficult to determine which loan best supports their family's financial stability. Choosing an unsuitable loan might lead to higher overall costs or repayment challenges down the line.

This article breaks down key factors parents should examine when comparing student loan offers. It aims to equip readers with clear criteria and strategies to identify the most favorable loan terms, helping them make informed decisions that minimize future financial strain.

- How do federal and private student loans compare? Federal vs Private

- How should parents compare student loan interest rates and fees? Rates and Fees

- What FAFSA steps determine student loan eligibility? FAFSA Steps

- How do borrowing limits differ for undergraduate, graduate, and parent loans? Borrowing Limits

- Which repayment plans lower monthly student loan payments? Repayment Plans

- What student loan forgiveness programs are available? Forgiveness Programs

- When should borrowers choose refinancing or consolidation? Refinance or Consolidate

- What deferment and forbearance options help during financial hardship? Deferment Options

- What happens if a student loan goes into default? Loan Default

- How can parents choose the best loan offer for college costs? Best Loan Offer

How do federal and private student loans compare?

Federal and private student loans differ significantly in interest rates, repayment options, and borrower protections. Federal loans, including Parent PLUS loans, offer fixed interest rates set annually by the government and flexible repayment plans such as income-driven repayment with forgiveness options under specific circumstances. Private loans tend to have variable or fixed rates based on creditworthiness and market conditions, which can make them more expensive or cheaper depending on timing and credit.

A key factor for many is the distinction in eligibility: federal student loans vs private loans for parents often hinges on credit checks. Federal loans require no credit check, granting wider access, while private lenders usually demand a strong credit score or co-signer, potentially limiting options for families with less established credit.

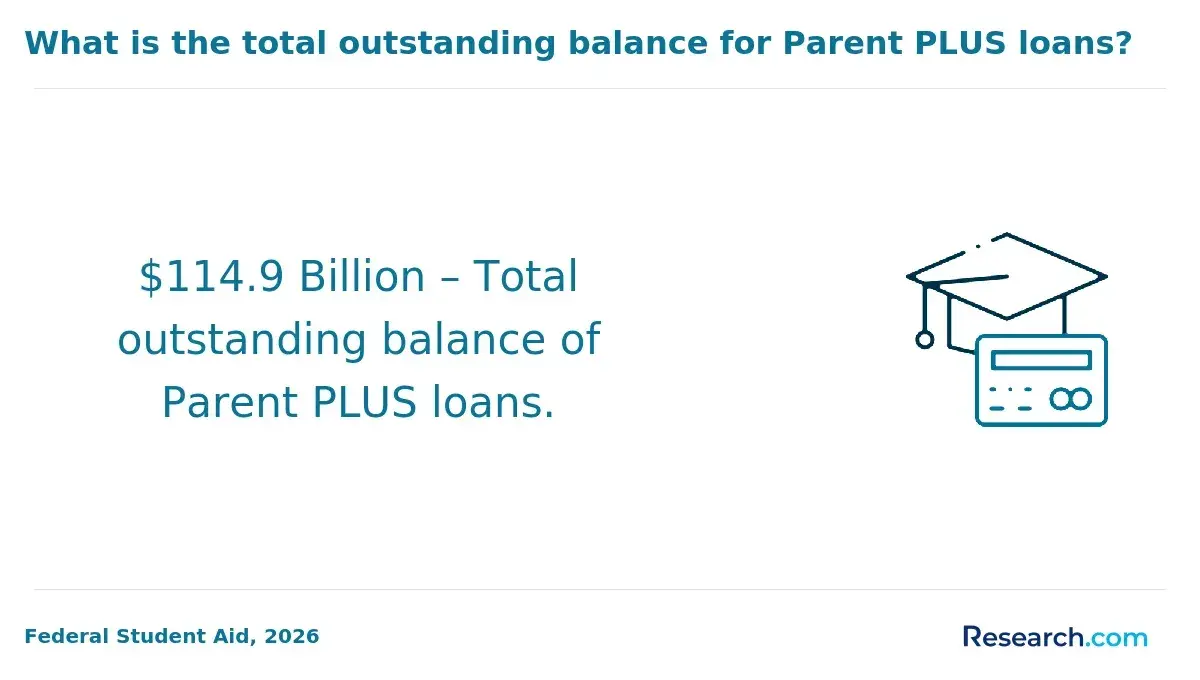

Other differences include loan fees and disbursement. Federal loans charge origination fees withheld from the loan amount; private loans may have fewer fees but sometimes apply prepayment penalties. Private loans often process faster, benefiting urgent funding needs. Parents hold about 12% of total federal student loan debt, or roughly $124 billion in Parent PLUS loans, emphasizing the importance of informed decisions.

Considering the key differences between federal and private student loans can guide families to the best choice for their situation. It's also wise to explore how can financial aid pay for rent to manage overall educational expenses more effectively.

How should parents compare student loan interest rates and fees?

Parents comparing student loan interest rates and fees should start by distinguishing between federal and private loans, as their terms and protections vary greatly. Federal loans make up 81.96% of all student loan debt and usually have fixed interest rates with lower fees, while private loans, covering 18.04%, often come with variable rates and different fee structures. These differences influence repayment costs and experiences over time.

When assessing rates, note whether they are fixed or variable: fixed rates offer predictable payments, whereas variable rates may begin lower but can increase, potentially raising long-term costs. For example, a private loan with a variable rate starting at 6% might rise to 10%, which parents must weigh against a typical federal fixed rate near 5%.

The origination fees also matter; federal Direct Loans charge between 1% and 1.06%, whereas private lenders might impose higher fees or none at all. Interest capitalization during deferment or forbearance can increase the total repayment amount-federal loans often limit capitalization, while private loan policies vary. Borrower protections like income-driven repayment plans and forgiveness options mostly apply to federal loans and are scarce for private ones.

Comparing the total repayment cost by estimating monthly payments over the term helps clarify financial advantages. For specialized options, parents might investigate ascent non cosigned student loans as part of a broader student loan interest rate comparison for parents. Requesting detailed loan terms and using official calculators ensures an accurate parent guide to student loan fees and interest rates.

What FAFSA steps determine student loan eligibility?

FAFSA steps that determine student loan eligibility start with accurately completing the Free Application for Federal Student Aid on time. A crucial factor is the Expected Family Contribution (EFC), which is calculated based on reported income, assets, and household size. This EFC influences the types and amounts of federal loans a student qualifies for under federal loan eligibility criteria for federal student loans through FAFSA.

Schools use FAFSA data to create financial aid packages, often including subsidized loans-need-based and awarded only if the EFC indicates financial need-and unsubsidized loans, which are available regardless of need. Enrollment status and cost of attendance also affect eligibility limits. Verification requests, such as tax return submissions, must be promptly handled to maintain loan eligibility, and any changes in family income or dependency status should be reported through FAFSA updates.

Federal Direct Loans offer a fixed 6.39% interest rate for undergraduates, providing predictable repayment terms. Private lenders may offer rates as low as 2.54% fixed or 3.65% variable APR but lack federal borrower protections, presenting a trade-off between lower rates and borrower security.

Applicants should compare offers carefully, including options like student loans for MBA programs, to find the best fit for their needs. Timely and accurate FAFSA completion is essential, as missed deadlines or incomplete applications can disqualify students from federal aid opportunities.

How do borrowing limits differ for undergraduate, graduate, and parent loans?

Borrowing limits vary notably between undergraduate, graduate, and parent loans due to their unique purposes and eligibility criteria. Undergraduate students qualify for Direct Subsidized and Unsubsidized Loans with annual limits from $5,500 to $12,500 based on year and dependency status, such as first-year students typically eligible for $5,500.

Graduate students face higher borrowing caps, up to $20,500 annually, but only through Direct Unsubsidized Loans since subsidized options are unavailable. These loans accrue interest immediately, increasing repayment costs over time. These differences in student loan borrowing caps for parents and students in the US reflect the varied cost of advanced education.

Parent PLUS Loans have no preset annual limit. Parents can borrow up to the total cost of attendance minus other financial aid. However, these loans include an upfront fee of 4.228%, so a $30,000 loan may incur about $1,268 in fees before interest. This is an important consideration for parents evaluating borrowing options.

Families should consider repayment terms and fees carefully, especially since parents are co-signers responsible for the loan. For those looking to reduce debt burdens, exploring private student loan refinancing can be a valuable strategy after initial borrowing.

Parent loan borrowing limits compared to undergraduate and graduate loans illustrate these distinct structures and financial impacts, helping borrowers to choose loans aligned with their financial capacity.

Which repayment plans lower monthly student loan payments?

Income-driven repayment (IDR) plans adjust monthly student loan payments based on your income and family size, often reducing payments to 10%-15% of discretionary income. Federal options like Income-Based Repayment (IBR), Pay As You Earn (PAYE), and Revised Pay As You Earn (REPAYE) help borrowers with limited cash flow avoid unaffordable payments.

Graduated repayment plans begin with lower monthly payments that increase every two years, benefiting those expecting higher future income by starting payments 50%-75% below standard fixed amounts. Extended repayment plans lengthen repayment up to 25 years instead of the typical 10, lowering monthly payments but increasing total interest. This option suits federal Direct Loans over $30,000 and some private loans.

Private lender repayment terms depend on credit profiles; most require minimum credit scores in the mid-600s. About 90% of new private undergraduate loans are cosigned by parents, impacting repayment options and interest rates. Refinancing with a cosigner can reduce monthly payments through lower interest rates or extended terms, though longer terms raise overall costs. Choosing the best plan involves considering income, credit history, loan type, and financial goals. Early consultation with federal loan servicers and private lenders ensures awareness of all available repayment options.

What student loan forgiveness programs are available?

Federal student loan forgiveness programs in 2026 focus mainly on loans held by borrowers employed in public service, low-income education, and specific government sectors. The Public Service Loan Forgiveness (PSLF) program is pivotal, offering forgiveness after 120 qualifying monthly payments while working full-time for government or nonprofit organizations. Maintaining accurate records of payments and employment status is essential to ensure eligibility.

Income-driven repayment (IDR) plans like Income-Based Repayment (IBR), Pay As You Earn (PAYE), and Revised Pay As You Earn (REPAYE) adjust monthly payments based on income and family size. These plans offer forgiveness after 20 or 25 years of qualifying payments and often reduce monthly bills significantly. For example, federal borrowers using IDR average payments near $89 monthly, compared to over $300 on standard plans, highlighting the financial relief these options provide (Education Data Initiative).

Teacher Loan Forgiveness grants up to $17,500 for educators serving five years in qualifying low-income schools. Other specialized forgiveness options may be available for healthcare workers, military personnel, and public sector employees, usually requiring specific service commitments.

Consistent, on-time payments and annual income verification are critical for forgiveness. Tax treatment varies: IDR forgiveness may be taxable, while PSLF forgiveness is tax-free. Carefully evaluating eligibility, payment history, and potential tax consequences is vital before pursuing these options.

When should borrowers choose refinancing or consolidation?

Refinancing student loans is best for borrowers seeking lower interest rates or better loan terms that reduce overall costs or monthly payments. It requires strong credit and financial stability, as private lenders prioritize applicants with good credit profiles. However, refinancing federal loans with private ones eliminates important federal benefits, such as income-driven repayment plans and loan forgiveness, so borrowers relying on these should avoid refinancing.

Consolidation suits those who want to combine multiple federal loans into a single, manageable monthly payment. This often extends the repayment term up to 30 years, lowering monthly payments but significantly increasing total interest paid. For example, increasing repayment from 10 to 25 years on a $40,000 federal loan at a 6.39% interest rate can raise total interest from about $14,000 to over $40,000, based on data from FinAid and the Education Data Initiative. This trade-off highlights the balance between affordability and long-term cost.

Refinance if reducing overall cost and interest is the priority and if federal protections are not needed. Consolidate if simplifying payments and improving immediate cash flow matter more than total cost. Key factors to consider include:

- Credit score and financial stability for refinancing eligibility.

- Need for federal benefits like deferment, forbearance, or forgiveness.

- Willingness to increase repayment time and interest expenses through consolidation.

- Current versus potential loan interest rates.

Borrowers should calculate the total repayment costs, not just monthly savings, to avoid costly mistakes over the loan's life.

What deferment and forbearance options help during financial hardship?

Deferment and forbearance are essential options for borrowers facing financial difficulties, allowing them to temporarily pause or reduce student loan payments. Federal student loans provide deferment for specific situations such as unemployment, economic hardship, half-time enrollment, or active military service. During deferment, the government typically covers interest on subsidized loans, preventing balance growth.

Forbearance, by contrast, lets borrowers temporarily suspend or lower payments but usually accrues interest on all loan types, increasing total costs. It's often used when deferment isn't available, for short-term issues like medical expenses or temporary financial strain.

Private student loans generally offer fewer deferment and forbearance options. Policies vary widely by lender, with some permitting hardship forbearance and others not, while interest accrual rules differ significantly. Borrowers should carefully review their lender's specific terms.

Duration and eligibility differ: economic hardship deferment can extend up to 36 months, while typical forbearance lasts 6 to 12 months with possible extensions. According to Education Data Initiative, 10.0% of federal student loan dollars were delinquent in Q4 2025, compared to a 1.62% private loan default rate in Q3 2025, underscoring stronger protections for federal loans. These options help borrowers avoid default, but it is crucial to understand terms and eligibility to apply the right relief during financial hardship.

What happens if a student loan goes into default?

Defaulting on a federal student loan triggers immediate financial and legal repercussions. After about 270 days of missed payments, the full loan balance is due, and borrowers lose access to deferment, forbearance, and additional federal aid. Federal authorities can garnish wages, taking up to 15% of disposable income without a court order. Additionally, tax refunds and Social Security benefits may be seized to cover the debt.

Default severely impacts credit, staying on reports for up to seven years and affecting borrowers and co-signers alike, such as parents with Parent PLUS loans, which average balances near $29,528 (Education Data Initiative). Poor credit can hinder qualifying for mortgages, car loans, or rental housing.

Options to address default include:

- Loan rehabilitation by making nine on-time payments within 10 months, which removes default status from credit reports.

- Loan consolidation to create a new loan with manageable terms, though it does not erase default from credit history.

Ignoring default risks escalating penalties and collection fees. Borrowers should promptly contact loan servicers or HUD-approved housing counselors for assistance. Federal agencies also provide income-driven repayment plans that may prevent default if accessed early. Proactive management of student loans safeguards credit health and financial stability over time.

How can parents choose the best loan offer for college costs?

Parents evaluating student loan offers should focus on interest rates, loan terms, repayment options, and borrower protections. Federal loans generally have lower interest rates and flexible repayment plans versus private loans. For example, federal Direct PLUS Loans offer income-driven repayment options that help manage payments after graduation.

It is important to consider the total cost over the lifetime of the loan, not just monthly payments. Loans with low initial rates might have high fees or balloon payments, increasing overall expense. Using online calculators to estimate total repayment can clarify the best choice.

Loan forgiveness programs require careful scrutiny. Despite their appeal, as of April 2018, only 0.28% of Public Service Loan Forgiveness applications were approved, according to the Education Data Initiative. Relying on forgiveness as a primary repayment method can lead to unexpected debt.

Repayment flexibility varies. Federal loans often allow deferment, forbearance, and income-driven plans, while private loans usually do not, increasing financial risk if circumstances change. Additional considerations include co-signer requirements and credit impact. Private loans often need co-signers with strong credit, which can affect credit scores and borrowing costs.

Before choosing, clarify these questions:

- What is the interest rate and is it fixed or variable?

- Are there fees or penalties for early repayment?

- What repayment plans and protections are offered?

- How does cosigning affect credit?

- Is loan forgiveness realistically attainable based on approval rates?

Other Things You Should Know About

Yes, parents can take out loans known as Parent PLUS loans to help cover college costs. These loans are borrowed in the parent's name, and the parent is responsible for repayment, not the student. It is important for parents to consider their own financial situation and credit history before applying.

Parents may qualify for certain tax benefits, such as the student loan interest deduction, which can reduce taxable income by up to $2,500 of interest paid annually. However, eligibility depends on income limits and the loan must be in the parent's or the student's name. Consulting a tax professional can clarify specific benefits based on individual circumstances.

Parent loans generally do not affect the student's federal financial aid eligibility because they are considered separate debt. However, large parent loans may influence future borrowing capacity or financial decisions. It's important to weigh how such loans fit into the overall college funding plan.

Most parent student loans allow early payments or full repayment without prepayment penalties. Making extra payments can reduce overall interest costs and the loan term. Parents should confirm the loan terms to ensure no fees apply for early repayment.