2026 Best Student Loans for Adult Students

Student Finance & Loan Expert

Adult students returning to school often face unique financial challenges, including balancing family expenses and managing existing debts. Securing the right student loan can be daunting amid various interest rates, repayment plans, and eligibility criteria. Making an uninformed choice can lead to higher costs and long-term financial strain. This article examines the best student loan options available to adult learners seeking graduate education, highlighting key features and benefits to support informed borrowing decisions that align with individual financial situations and career goals.

- What types of student loans are available to adult students returning to school? Loan types

- How should adult learners choose between federal and private student loans? Federal vs private

- What are the key eligibility requirements for adult students to get federal loans? Eligibility

- How do interest rates, fees, and borrowing limits work for adult student loans? Rates & limits

- How do you apply for student loans as an adult, including the FAFSA steps? Apply & FAFSA

- Which federal repayment plans work best for adult borrowers with existing obligations? Best repayment

- What loan forgiveness and discharge options can adult students realistically qualify for? Forgiveness options

- How can adult borrowers refinance or consolidate student loans to lower payments? Refinance & consolidate

- What hardship options exist for adult students, like deferment and forbearance? Hardship relief

- How do student loans affect an adult borrower's credit, default risk, and finances? Credit impact

What types of student loans are available to adult students returning to school?

Adult learners returning to college have multiple student loan options for adult learners, including federal direct loans, private loans, and parent PLUS loans available under certain conditions. Federal direct loans consist of subsidized loans-which are need-based and where the government pays interest during enrollment-and unsubsidized loans that accrue interest from disbursement but are accessible regardless of financial status.

Private loans, typically offered by banks or credit unions, require credit approval and may carry higher interest rates and less flexible repayment plans. These loans can help students who reach federal loan limits or need extra funds, but careful comparison of terms and credit impact is essential.

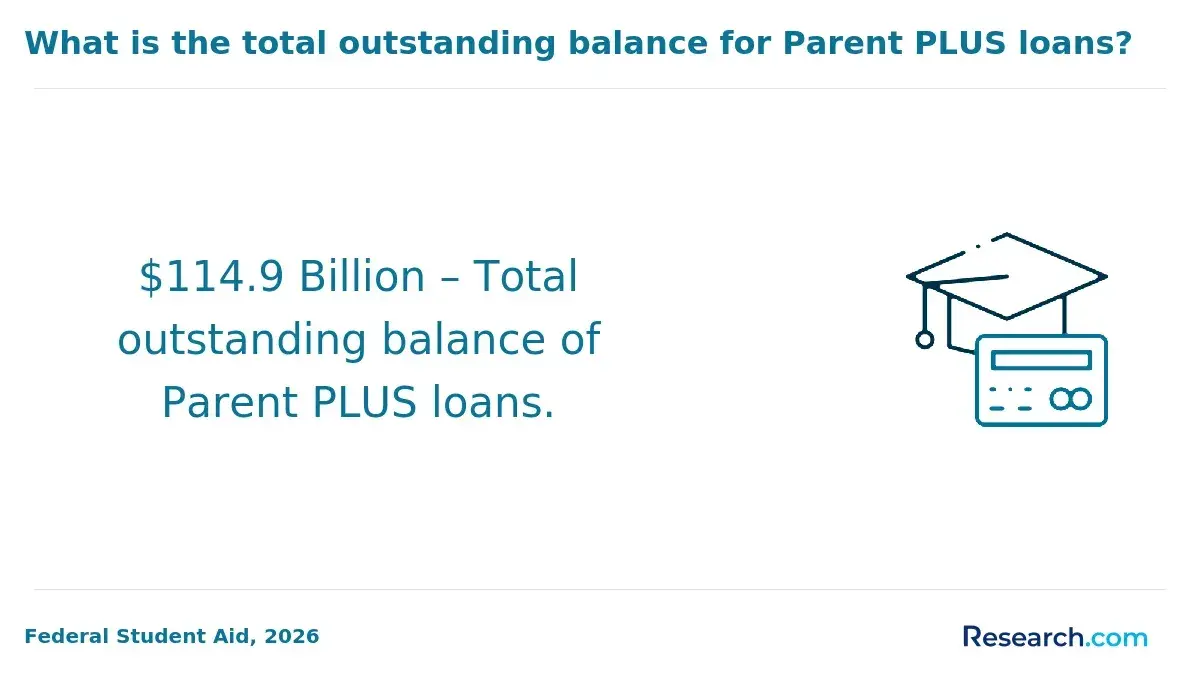

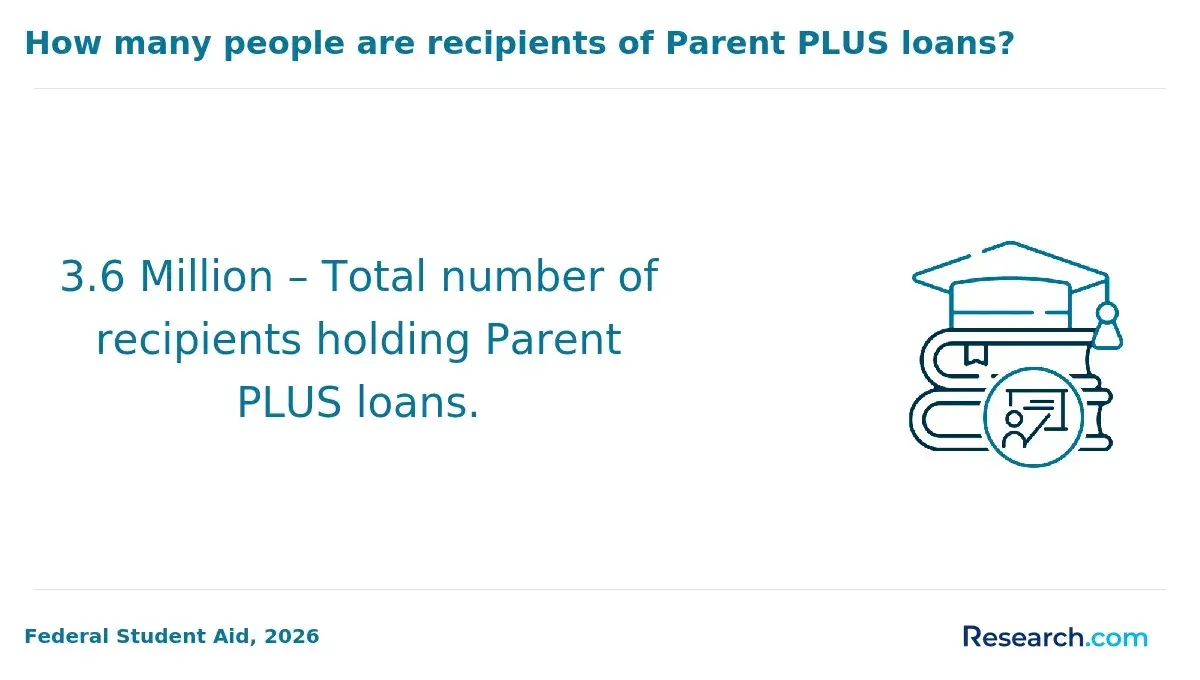

Parent PLUS loans may also assist adult students when a parent is willing and qualifies to borrow on their behalf, providing additional borrowing capacity beyond federal limits.

Many adult students balance full-time work with studies; about 57% work 30 or more hours weekly according to the National Center for Education Statistics. This makes income-driven repayment plans linked to federal loans attractive for managing debt with variable income. Financial aid programs for adults returning to college often emphasize these adaptable repayment options.

To explore flexible funding quickly, some may seek quick student loans. Federal direct loans generally offer the safest and most flexible terms, while private loans should be considered only after maximizing federal aid options.

How should adult learners choose between federal and private student loans?

Adult learners deciding between federal and private student loans should weigh cost, repayment flexibility, and borrower protections carefully. Federal loans have significantly lower average interest rates-around 5.5% fixed for undergraduates-compared to private loans, which in early 2025 averaged 9.02% variable and 6.85% fixed. This gap can mean paying thousands more over the life of a private loan. Knowing how to compare federal and private student loan options is crucial for making an informed choice.

Federal loans provide important benefits like income-driven repayment plans, deferment, and forbearance, which help adults balancing work and family obligations. Private lenders rarely offer such flexibility or forgiveness programs. Adults with limited or no credit history generally qualify more easily for federal loans without a cosigner, while private loans usually require strong credit or cosigners.

- Interest rates and total cost: Federal loans are typically fixed and lower; private loans may increase, causing unpredictable monthly payments.

- Repayment flexibility: Federal loans adjust payments based on income changes; private loans usually do not.

- Credit requirements: Private loans require stronger credit or cosigners but may offer competitive rates.

- Loan limits: Federal loans have limits, sometimes requiring supplemental private loans.

Those choosing the best student loan for adult learners in the United States should maximize federal options first. Use private loans only when federal aid is insufficient, after carefully reviewing terms and conditions. Also, pay attention to student loan application deadlines to optimize funding opportunities.

What are the key eligibility requirements for adult students to get federal loans?

To meet the eligibility criteria for federal student loans for adult learners, applicants must be U.S. citizens or eligible non-citizens with a valid Social Security number. Enrollment at least half-time in an accredited degree or certificate program is required, impacting loan eligibility and amounts. Many adult students attend community colleges, universities, or vocational schools with part-time status allowed if half-time enrollment is maintained.

Satisfactory academic progress, as defined by the institution, must be maintained; failure to do so can lead to loss of federal loan eligibility. Borrowers cannot have federal student loan defaults or owe refunds on federal grants. Financial need influences eligibility for certain federal loans, such as subsidized Direct Loans, which consider the cost of attendance minus other aid. Unsubsidized loans are available regardless of financial need.

Federal loan requirements for adult students in the United States include completing the Free Application for Federal Student Aid (FAFSA) annually. Accurate reporting of income and household information is essential, especially since adult learners may be considered independent students. Notably, students aged 30 and older usually have higher loan balances, with a median federal loan amount about 25% greater than that for borrowers under 24, reflecting longer enrollment or attendance at more expensive schools.

Adult students exploring funding options may also want to consider college loans for parents as a potential resource.

How do interest rates, fees, and borrowing limits work for adult student loans?

Interest rates on adult student loans depend heavily on loan type and lender, which directly affects total repayment costs. Federal student loans usually feature fixed interest rates from roughly 4.99% to 7.54%, varying by program. Private loans may offer fixed or variable rates typically starting between 5% and 12%, influenced by factors like credit score and income. Fixed rates offer predictability, while variable rates carry the risk of increasing over time. This variability shows how interest rates affect adult student loans in significant ways.

Fees and borrowing limits for adult student loans also play important roles. Federal loans generally have origination fees around 1% to 1.06% deducted upfront, lowering the amount initially disbursed. Private lenders might charge application, origination, or late payment fees, which vary widely, so it is crucial to review these details carefully. Borrowing limits differ by loan type and borrower status: federal Direct Subsidized and Unsubsidized Loans range annually from $5,500 to $20,500, with aggregate debt caps between $31,000 and $138,500. Private loans often offer higher limits but may require proof of income or cosigners.

Adults returning to education after age 25 can boost median annual earnings by about $18,000 compared to those with some college but no degree, eventually earning nearly $720,000 more over a lifetime, according to Georgetown University Center on Education and the Workforce. Choosing a loan with manageable rates, fees, and borrowing limits can enhance long-term financial outcomes. For those considering adjustments, student loan refinancing might offer additional options to improve repayment terms.

How do you apply for student loans as an adult, including the FAFSA steps?

To apply for student loans as an adult, begin by completing the Free Application for Federal Student Aid (FAFSA). Creating an FSA ID on the Federal Student Aid website is essential since it serves as your electronic signature. Prepare necessary documents, including your Social Security number, recent federal tax returns, bank statements, and records of untaxed income.

Complete the FAFSA for the 2026 academic year at the official website, reporting accurate tax information. Adults may need to include spouse income if married. Using the IRS Data Retrieval Tool within the FAFSA can simplify the process by importing tax data automatically and minimizing errors.

Once submitted, a Student Aid Report (SAR) summarizes your application-review it carefully and correct any mistakes to prevent delays. Schools will use this to design your financial aid package, possibly including federal student loans.

Federal Direct Unsubsidized Loans are common for adult borrowers. Income-driven repayment plans may help reduce monthly payments, but be mindful that borrowers aged 35 and older have a 20% serious-delinquency or default rate, compared to about 13% for younger borrowers, according to the Federal Reserve Bank of New York. Budgeting and understanding loan terms are crucial before borrowing.

Private student loans require separate applications and often a good credit score or cosigner. It's important to shop around for competitive interest rates and repayment options that match your financial situation.

Which federal repayment plans work best for adult borrowers with existing obligations?

Federal repayment plans that adjust payments based on income provide crucial relief for adult borrowers managing various financial responsibilities. Income-Driven Repayment (IDR) options like Income-Based Repayment (IBR), Pay As You Earn (PAYE), and Revised Pay As You Earn (REPAYE) cap payments at 10% to 15% of discretionary income, accommodating those balancing loans with mortgages, childcare, or other debts.

Graduated repayment plans are another option, starting with lower payments that gradually increase, fitting for adults expecting income growth. Fixed repayment plans, while straightforward, may pose financial strain due to their higher monthly amounts and are less suitable for those with tight budgets.

Borrowers with Direct PLUS Loans face increased fixed interest rates, now at 9.08%, making repayment more expensive. For instance, a $40,000 PLUS loan over ten years could accrue $4,000-$5,000 more in interest than before (Federal Student Aid, "Interest Rates and Fees for Federal Student Loans," 2024). This rise highlights the benefit of IDR plans limiting monthly payments for these borrowers.

Key points for adult borrowers to consider include:

- Evaluating eligibility for IDR plans to lower monthly payments based on current income.

- Utilizing Public Service Loan Forgiveness when working in qualifying fields, which pairs well with IDR plans.

- Recognizing that longer repayment periods under IDR plans mean more interest accrues over time.

What loan forgiveness and discharge options can adult students realistically qualify for?

Adult borrowers have several federal loan forgiveness and discharge options based on their profession, loan type, and financial status. Public Service Loan Forgiveness (PSLF) is available for those working full-time in government or qualifying nonprofit jobs. After making 120 qualifying payments on an income-driven repayment plan, the remaining federal loan balance is forgiven.

Income-Driven Repayment (IDR) forgiveness applies to plans such as PAYE, REPAYE, and IBR. Payments are based on income and family size, with any remaining balance forgiven after 20 or 25 years, though forgiveness may be taxable.

Loan discharge options include Total and Permanent Disability (TPD) discharge, for borrowers unable to work due to disability, and borrower defense discharge for those defrauded by their schools.

Federal Parent PLUS loan borrowers may qualify for discharge in case of the student's death or permanent disability, and sometimes bankruptcy under recent legal changes.

Private student loans generally lack forgiveness options. However, 92% of new private undergraduate loans had creditworthy cosigners recently. Adults over 30 represent the fastest-growing group approved without a cosigner, increasing 14% year-over-year, showing a rise in credit independence among adult borrowers.

How can adult borrowers refinance or consolidate student loans to lower payments?

Refinancing and consolidation are key strategies adult borrowers can use to reduce student loan payments based on their financial situations. Refinancing combines multiple loans into one, usually with a lower interest rate, leading to smaller monthly payments. To qualify, borrowers generally need good credit and steady income. However, refinancing federal loans into a private loan may cause loss of federal benefits like income-driven repayment plans or loan forgiveness.

Federal loan consolidation merges multiple loans into a single payment, often extending the term to lower monthly costs. The Federal Direct Consolidation Loan is a popular choice for managing various federal loan types. Longer repayment terms may increase total interest paid, so comparing terms is important before proceeding.

For borrowers with limited credit or income, income-driven repayment plans offer payment adjustments based on earnings without refinancing. Employer tuition assistance programs also help reduce loan burdens; although nearly half of U.S. employers offer tuition assistance, only a small percentage of employees use this benefit, according to the Society for Human Resource Management Employee Benefits Survey.

Key steps to lower payments include:

- Checking eligibility for federal consolidation versus private refinancing.

- Comparing interest rates and repayment terms carefully.

- Utilizing employer tuition assistance to reduce costs.

- Considering income-driven repayment if refinancing is unsuitable.

What hardship options exist for adult students, like deferment and forbearance?

Adult students facing financial hardship can access deferment and forbearance options to manage their student loans. Deferment pauses payments without interest accruing on subsidized loans, typically granted for reasons like half-time enrollment or unemployment. For example, a full-time returning student may request deferment to temporarily halt repayment.

Forbearance allows reduced or paused payments, usually up to 12 months, but interest accrues on all types of loans during this time, increasing total costs. It suits those with short-term financial issues such as medical expenses or emergencies, especially if they don't qualify for deferment. Both federal and some private lenders offer this, but terms vary, so contacting your loan servicer directly is crucial.

Income-driven repayment plans also help by adjusting monthly payments based on income and family size, easing financial pressure while maintaining loan status. Strategies to minimize debt, like starting at community colleges before transferring, can save significant tuition costs-on average, $11,400 according to the College Board, reducing loan burdens.

- Contact your loan servicer promptly for personalized guidance

- Evaluate eligibility and impacts of each hardship option carefully

- Focus on reducing overall debt and avoiding default

How do student loans affect an adult borrower's credit, default risk, and finances?

Student loans directly affect adult borrowers' credit by adding debt visible on credit reports, impacting credit scores based on payment history. Timely payments boost creditworthiness and ease future borrowing, while missed payments harm scores and increase the risk of default. Defaulting can lead to wage garnishment, tax refund offsets, and significant credit damage, restricting access to other credit or housing.

Adult borrowers often face heightened default risk by managing education costs alongside mortgages, childcare, or medical bills. Income fluctuations or job changes can lead to payment inconsistencies and missed deadlines.

Financially, student loans limit disposable income during repayment, complicating budgeting and savings efforts. For example, households led by someone aged 40-49 with active student debt show a median retirement account balance 30% lower than those without, according to the Federal Reserve's Survey of Consumer Finances. This highlights the balancing act between funding education and saving for retirement.

Strategies to reduce negative impacts include:

- Using income-driven repayment plans to lower monthly payments.

- Prioritizing repayment on loans with higher interest rates.

- Maintaining consistent payments to protect credit scores and avoid default.

These approaches help borrowers manage their finances more effectively while safeguarding credit health and reducing default risk.

Other Things You Should Know About

Yes, adult students can qualify for student loans without a co-signer, especially when applying for federal student loans. Federal loans do not require a credit check or co-signer, making them accessible to adult learners. However, private lenders often require a co-signer if the borrower has limited credit history or income.

Adult students may be eligible to deduct up to $2,500 of student loan interest on their federal income tax returns, provided they meet certain income limits and file appropriately. This deduction applies only to interest paid on qualified student loans and can reduce taxable income, benefiting borrowers during repayment.

Part-time adult students may still qualify for both federal and private student loans, but loan amounts could be lower compared to full-time enrollment. Federal loan eligibility often depends on the number of credits taken each term, which can affect borrowing limits and repayment timelines.

If an adult student drops out, loan repayment typically begins after a grace period, usually six months for federal loans. Leaving school early does not cancel the loan; interest may continue to accrue, and borrowers must repay according to their loan terms to avoid default and negative credit consequences.