2026 How to Pay for College If Your Aid Package Is Too Small

Student Finance & Loan Expert

Many graduate students face the challenge of insufficient financial aid packages to cover tuition and living expenses. This shortfall often forces students to seek alternative funding methods while avoiding excessive debt.

Without clear guidance, navigating loans, scholarships, and employer assistance can be overwhelming and discouraging. Understanding available options becomes crucial to making informed decisions about financing advanced education.

This article examines practical strategies to supplement inadequate aid packages, focusing on loan types, repayment options, and other resources to help students manage costs effectively while minimizing financial strain.

- What should you do first if your financial aid package doesn't cover college costs? First steps

- How can you appeal or negotiate a larger financial aid offer with your college? Aid appeal

- What federal student loan options can fill the gap when aid is too small? Federal loans

- When does it make sense to use private student loans for unmet college costs? Private loans

- How can you reduce your college bill through budgeting, cheaper schools, or extra credits? Cut costs

- What scholarships, grants, and work-study options can you still apply for after aid? Extra aid

- How do parent loans and family contributions fit into paying for college shortfalls? Parent options

- How much should you safely borrow, and how do projected payments affect affordability? Safe borrowing

- What repayment plans, forgiveness programs, and protections apply to gap-filling loans? Repayment & relief

- How can refinancing or consolidation help manage loans you took to cover aid gaps? Refinance & consolidate

What should you do first if your financial aid package doesn't cover college costs?

If your financial aid package doesn't fully cover college costs, start by appealing your aid offer. Contact the financial aid office directly to request a reassessment and provide updated documentation of changes in your family's financial situation, such as job loss or medical expenses. This professional judgment review can lead to additional aid.

Evaluate the total cost of attendance, including tuition, fees, room, board, and personal expenses. Community college tuition averaged $3,990, in-state public universities $11,260, and private nonprofit colleges $41,540. Considering these differences can guide your educational path effectively.

Cost-saving options include beginning at a community college before transferring to a four-year institution. This approach maintains academic credits while reducing expenses.

Be sure to apply for additional scholarships and grants from private organizations, employers, or community groups to supplement your aid package. These funds typically don't require repayment.

If more funding is necessary after appealing and seeking scholarships, explore federal and state financial aid options first. Federal student loans generally provide lower interest rates and stronger borrower protections compared to private loans.

When negotiating or appealing aid, ask if there have been income changes, special circumstances affecting payment ability, or if the college offers emergency funds or payment plans. Understanding these details can unlock more assistance.

For those considering dental school, learning how to pay for dental school is crucial to manage loan options wisely.

How can you appeal or negotiate a larger financial aid offer with your college?

To negotiate a larger financial aid package at your university, start by contacting the financial aid office with a clear explanation of your current financial situation.

Provide updated documents such as recent pay stubs, termination notices, or medical bills, emphasizing any changes that impact your family's ability to pay. Many schools consider professional judgment requests that adjust aid based on unforeseen hardships.

Nearly half of undergraduates face recent financial disruptions like job loss or income cuts, but less than one-fifth formally seek aid adjustments, missing potential support. When appealing, submit a written letter or form outlining:

- Reasons for changed finances, such as job loss or unexpected expenses

- Household size and number of dependents

- Any assets or income not reflected in the original application

- A comparison of your Expected Family Contribution (EFC) to actual available resources

Request information about institutional aid options like emergency grants or merit scholarships that may not have been included initially. If your appeal is denied, inquire about further appeals or outside scholarships.

Effective appeals that reflect current realities improve your chances of additional aid. For students seeking more financial flexibility, researching independent student loans can be a valuable step.

Knowing how to appeal for more financial aid at college empowers you to make informed decisions during your education funding process.

What federal student loan options can fill the gap when aid is too small?

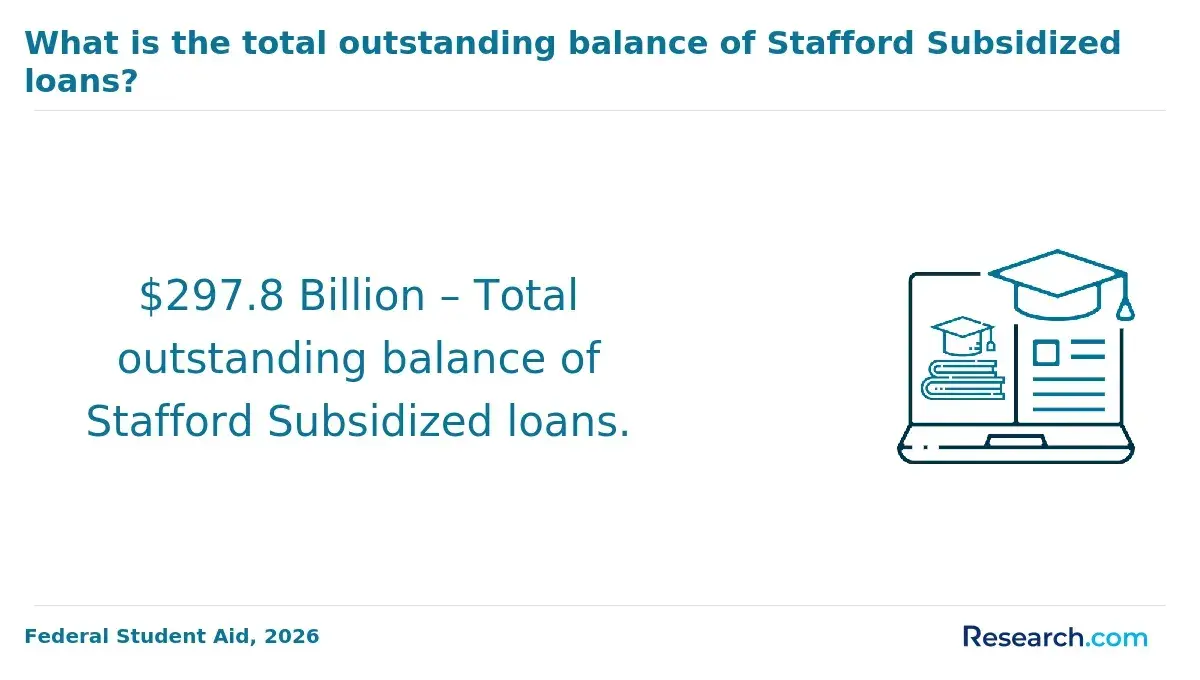

Federal student loan options for covering college costs include the Direct Subsidized Loan, which is available to undergraduates with demonstrated financial need. The government covers interest while you're in school and during deferment, reducing the overall loan cost. Annual limits range from $3,500 to $5,500 depending on year, with a lifetime cap of $23,000.

For students without demonstrated need, the Direct Unsubsidized Loan allows undergraduates to borrow up to $7,500 per year (including subsidized amounts) with a lifetime maximum of $31,000. Interest starts accruing upon disbursement, so paying periodically helps avoid extra debt.

Graduate students can borrow up to $20,500 annually in unsubsidized loans, with a combined total limit of $138,500 including undergraduate loans, helping cover tuition and living expenses.

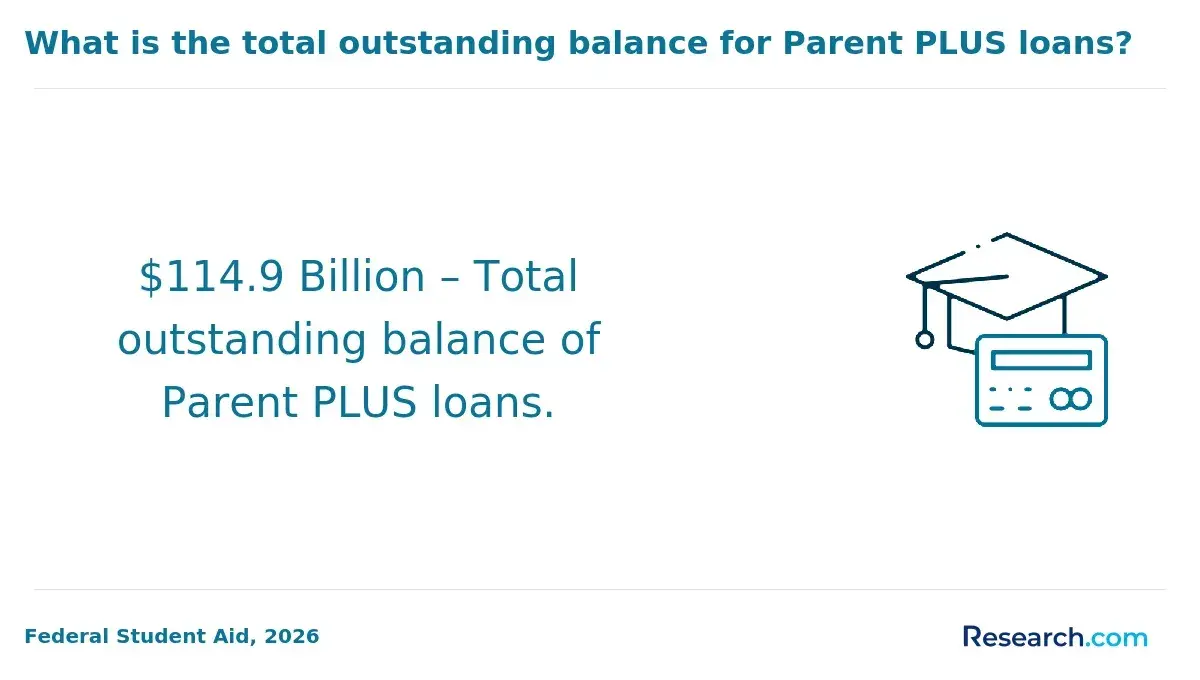

Federal Parent PLUS Loans let parents of dependent students borrow up to the full cost of attendance minus other aid, with repayment flexibility but higher interest rates and credit check requirements.

Many students miss out on aid completely-unclaimed Pell Grants totaled at least $4.0 billion in 2023-24 according to the Education Data Initiative's "Financial Aid Statistics 2025." Completing the FAFSA is essential to access all federal loans.

How to use federal loans to bridge financial aid gaps often involves borrowing up to subsidized limits first, then unsubsidized loans, and reserving Parent PLUS loans as a last option. Combining federal loans strategically can help cover remaining costs while managing repayment responsibly.

Those considering alternatives should explore MBA private student loans as part of a comprehensive funding plan.

When does it make sense to use private student loans for unmet college costs?

Private student loans for college expenses can be a reasonable choice when other aid options are exhausted, yet essential costs remain. These include tuition, housing, books, and necessary fees not covered by scholarships, grants, or federal loans.

For instance, students at private nonprofit four-year colleges may still face high unmet costs despite an average aid package of $20,860, according to the College Board's Trends in Student Aid 2024.

Consider private loans when federal Direct Loans and grants have been fully used but financial shortfalls persist, or if the family's expected contribution is fixed with no affordable credit alternatives. They also help when attendance costs increase unexpectedly, such as higher housing or technology fees.

Students attending institutions with lower average aid, like public four-year colleges providing only $4,170 on average, may encounter greater out-of-pocket expenses, highlighting when to consider private loans for unmet college costs.

For those comparing options, checking the best bank student loan refinance rates can provide insights into managing debt responsibly. Private loans fill gaps left by federal aid but require careful borrowing decisions to avoid excessive debt.

How can you reduce your college bill through budgeting, cheaper schools, or extra credits?

Reducing college expenses starts with a detailed budget that tracks tuition, fees, housing, textbooks, and daily costs. Limiting discretionary spending and using student discounts can significantly lower overall spending.

Opting for community colleges or in-state public universities often provides substantial savings compared to private or out-of-state schools. For instance, public four-year universities typically have much lower tuition fees.

Many students save thousands by completing general education credits at a community college before transferring.

Earning extra credits each semester shortens time to degree completion, cutting tuition and living costs. Taking 15-18 credits instead of the standard 12 or earning credits through Advanced Placement exams, dual enrollment, or summer courses allows earlier graduation.

Part-time employment also helps offset expenses. The median wage for young U.S. workers is around $15.38 per hour, and working about 15 hours weekly during the academic year can generate over $6,900. This income can cover essential costs or reduce reliance on student loans.

Strategies to reduce college costs include:

- Creating and sticking to a strict budget

- Choosing affordable schools like community colleges or public universities

- Enrolling in extra courses for faster graduation

- Working part-time to supplement income

What scholarships, grants, and work-study options can you still apply for after aid?

When financial aid falls short, many students can tap into multiple scholarship, grant, and work-study options beyond federal offerings. Local scholarships from community groups, employers, or civic organizations often face less competition than national awards, making them worth pursuing.

Maximize federal grants like the Pell Grant by submitting an updated FAFSA annually to reflect changes in your financial situation. Additionally, some states provide their own need-based grants separate from federal aid.

Institutional scholarships, including departmental or merit-based awards, may become available mid-year or for continuing students. Contact your college's financial aid office to inquire about these opportunities.

Federal work-study programs offer flexible on- or off-campus jobs, sometimes with higher pay. Some institutions also provide additional work-study or emergency relief options.

Online learners should consider scholarships designed specifically for distance-education students, an increasingly common demographic. According to NCES data, 59% of undergraduates took at least one online course, with 28% enrolled exclusively online.

Private scholarships from corporations, foundations, and professional associations remain a valuable but frequently overlooked resource. Use specialized online platforms and scholarship search engines to discover awards matching your interests and background.

Employer tuition reimbursement programs can help working students reduce loan debt by supplementing financial aid packages.

How do parent loans and family contributions fit into paying for college shortfalls?

Parent loans like federal Parent PLUS loans can cover the full cost of attendance minus financial aid but require a credit check and have fixed interest rates.

These loans increase family debt and typically must be repaid by the parent soon after disbursement, so it's important to evaluate repayment ability carefully. Combining them with family contributions helps manage overall costs more effectively.

Family contributions often come from savings, income, or assets. One popular option is the 529 college savings plan, which families use to pay for qualified education expenses without incurring loan interest.

In recent years, 529 withdrawals have seen substantial growth, reflecting their increasing role in funding college. Additional family funds may include gifts or payment plans arranged directly with colleges to ease the student's loan burden after graduation.

Key considerations when using these tools include:

- Evaluating repayment capacity to avoid long-term financial strain from Parent PLUS loans.

- Using 529 plan withdrawals strategically to maximize tax benefits and meet immediate college costs.

- Balancing current family financial stability with future obligations by combining savings and loans.

- Exploring alternative loans or scholarships before relying heavily on parent borrowing.

By blending family savings and carefully selected parent loans, families can reduce the need for excessive student borrowing and manage college expenses more smoothly.

How much should you safely borrow, and how do projected payments affect affordability?

Limit your total student loan debt to a level that results in manageable monthly payments after graduation.

Affordability depends on your expected starting salary, loan terms, and repayment plan. A common guideline is to keep monthly payments below 10%-15% of your anticipated take-home pay.

For example, if you expect a $40,000 annual salary (about $2,800 monthly after taxes), your monthly student loan payment should ideally be between $280 and $420. Borrowing around $25,000 to $35,000 at a 5% interest rate on a 10-year standard repayment plan typically fits this range.

Half of bachelor's degree recipients carried an average student debt balance of $29,300, according to the College Board's Trends in Student Aid 2024. This provides a realistic benchmark, though your major and career prospects may affect your personal situation.

Use repayment calculators early to estimate monthly payments. If these seem too high, consider options such as:

- Increasing scholarships and grants

- Participating in work-study programs

- Attending lower-cost schools

Borrow only what aligns with your expected earnings to avoid long-term financial issues. Prioritize federal loans when possible, as they usually provide more flexible repayment options compared to private loans.

What repayment plans, forgiveness programs, and protections apply to gap-filling loans?

Federal student loans provide several repayment options to help borrowers manage balances that aid packages don't fully cover. Income-Driven Repayment (IDR) plans like Income-Based Repayment (IBR), Pay As You Earn (PAYE), and Revised Pay As You Earn (REPAYE) adjust monthly payments based on your income and family size, sometimes reducing payments to $0 per month for those facing financial hardship.

Loan forgiveness programs benefit borrowers working in public service or non-profit roles. The Public Service Loan Forgiveness (PSLF) program cancels remaining balances after 120 qualifying payments under an IDR plan while employed full-time by eligible employers. Additionally, Teacher Loan Forgiveness offers up to $17,500 in forgiveness for educators in low-income schools.

Protections like deferment and forbearance provide temporary relief by pausing or reducing payments. Economic Hardship Deferments are critical if monthly payments on gap-filling loans exceed your budget. Avoiding default is vital since it harms credit and increases the total cost of repayment.

The College Board reports that on-campus room and board costs average $12,770 at public four-year colleges, while living off-campus with family averages $9,400, saving about $3,370 annually. These savings can reduce loan reliance and ease repayment stress.

Explore repayment plans, forgiveness options, and protections early to maintain financial stability and make informed loan decisions.

How can refinancing or consolidation help manage loans you took to cover aid gaps?

Refinancing student loans allows borrowers to replace multiple loans with a single new loan, often at a lower interest rate.

This can reduce monthly payments and overall interest costs, easing financial strain. For example, someone with federal and private loans averaging 7% interest might refinance to a private lender offering 5%, saving hundreds of dollars monthly over time.

Consolidation merges multiple federal loans into one Direct Consolidation Loan, simplifying payments and potentially extending repayment terms to lower monthly outflows. However, consolidation locks in a weighted average interest rate and may eliminate benefits such as loan forgiveness or flexible repayment plans.

Both options help borrowers struggling with high payments or multiple servicers. Students with extended enrollment should consider these strategies carefully, particularly since only about 64% of students starting a bachelor's degree finish within six years, according to the National Student Clearinghouse Research Center, increasing debt over time.

Other Things You Should Know About How to Pay for College If Your Aid Package Is Too Small

Yes, student loans can impact your credit score both positively and negatively. Making on-time payments can help build a positive credit history, while missing payments or defaulting can significantly damage your credit. It's important to monitor your loan accounts and stay current with payments to maintain good credit.

Yes, federal student loans have annual and aggregate borrowing limits depending on your year in college and dependency status. Private loans typically have fewer restrictions but often require credit approval and sometimes a co-signer. Understanding these limits can help you avoid borrowing more than you can reasonably repay.

Deferment and forbearance are options that allow you to temporarily pause or reduce loan payments during financial hardship. Interest may continue to accrue on some loans during these periods, especially on unsubsidized federal and private loans. It's important to contact your loan servicer to discuss eligibility and the terms before choosing these options.

Defaulting on student loans can lead to serious consequences including damage to your credit score, wage garnishment, and loss of eligibility for additional federal aid. Default usually occurs after 270 days of nonpayment on federal loans. If you are at risk, it's crucial to communicate with your loan servicer to explore rehabilitation or repayment plans that can help avoid default.