2026 Best Speech Pathology Student Loans

Student Finance & Loan Expert

Many aspiring speech pathology students face the challenge of funding their graduate education, especially when transitioning from unrelated undergraduate backgrounds. High tuition costs and living expenses can create financial barriers that delay or deter enrollment.

Navigating student loan options adds complexity, from federal to private choices, each with unique terms and eligibility requirements. Without clear guidance, students may take loans that increase long-term debt burdens unnecessarily.

This article examines current student loan programs tailored to speech pathology students and offers strategies to select the most advantageous financing, helping readers manage education costs effectively and minimize financial risk.

- What types of student loans are available for speech pathology majors and graduate students? Loan types

- How do federal and private speech pathology student loans compare on cost and protections? Federal vs private

- How much can speech pathology students borrow, and what interest rates should they expect? Limits & rates

- How do you use the FAFSA to maximize federal aid before taking speech pathology loans? FAFSA steps

- What special considerations apply to loans for speech-language pathology graduate and clinical programs? Grad SLP loans

- Which repayment plans work best for speech pathology salaries at different career stages? Best repayment

- What loan forgiveness and repayment assistance programs exist for speech-language pathologists? SLP forgiveness

- How can speech pathology borrowers refinance or consolidate loans to lower payments or rates? Refinance options

- What deferment, forbearance, and hardship options are available to speech pathology borrowers? Hardship relief

- How do student loans affect a speech pathologist's credit, licensing, and long-term finances? Credit impact

What types of student loans are available for speech pathology majors and graduate students?

Speech pathology students can use various student loans tailored to their needs, including federal direct loans, private loans, and state-specific programs. Federal student loans for speech pathology students are often the first option, featuring the Direct Unsubsidized Loan, allowing up to $20,500 per year without needing to prove financial need-and the Direct PLUS Loan, which covers additional costs but requires a credit check.

Private loan options for speech pathology graduate programs serve to fill funding gaps or offer flexible repayment but usually come with higher interest rates based on creditworthiness. Unlike federal loans, private loans lack borrower protections like income-driven repayment plans, making them a less favorable choice unless necessary.

State loan programs may provide scholarships or loan forgiveness if students commit to working in specific areas after graduation, but these vary significantly by location and often have service obligations.

At institutions like Pacific University of Oregon, speech-language pathology master's programs can exceed $150,000 in tuition and fees over two years; therefore, budgeting must also factor in living expenses and loan origination fees.

Students should prioritize federal options due to lower rates and protections and turn to private loans only when these are exhausted. For urgent funding needs, learning how to get last minute student loans can be beneficial.

How do federal and private speech pathology student loans compare on cost and protections?

Federal speech pathology student loans generally offer lower interest rates and stronger borrower protections than private loans. Federal Direct Unsubsidized Loans for graduate students carry a fixed rate around 7% and include benefits such as income-driven repayment plans and eligibility for public service loan forgiveness.

These features make federal loans appealing for many, especially when considering speech pathology student loan protections and repayment options.

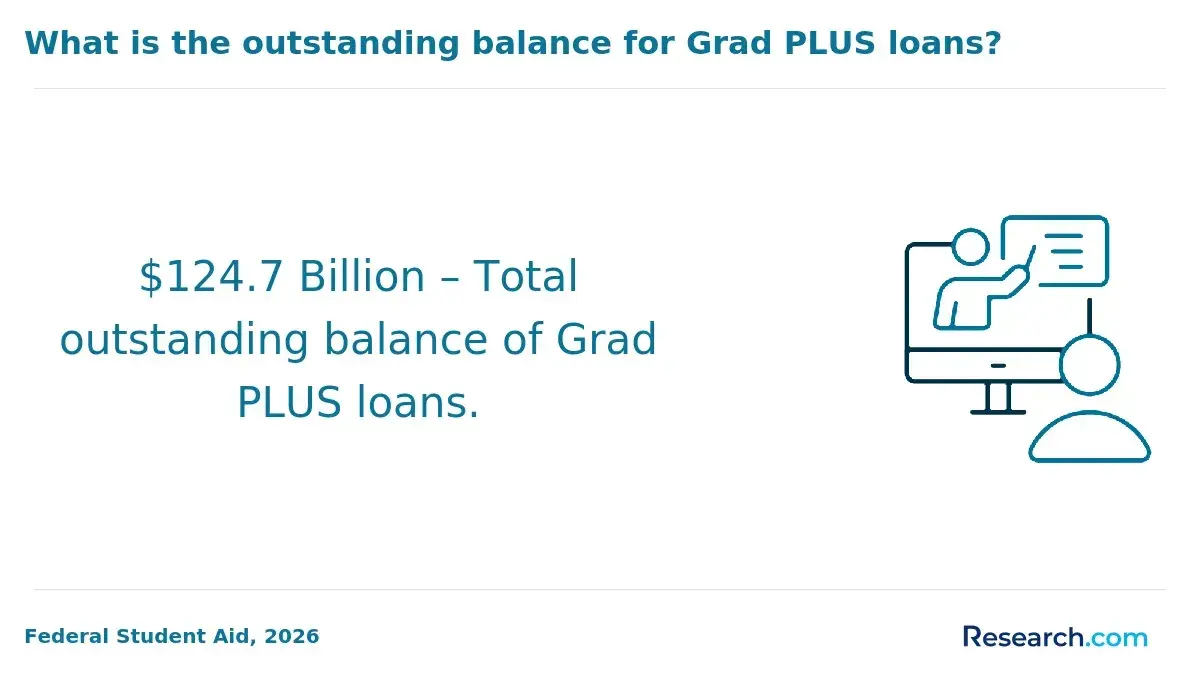

Starting July 1, 2026, new federal borrowing limits cap graduate students at $20,500 annually for Direct Unsubsidized Loans, with a $100,000 aggregate lifetime maximum. Previously, Grad PLUS loans allowed borrowing up to nearly the full cost of attendance.

Key differences include:

- Federal loans offer deferment and forbearance during hardship or unemployment.

- Private loans often require a creditworthy cosigner and lack flexible forgiveness programs.

- Federal loans have fixed interest rates; private loans may have variable rates that can increase.

Students exceeding federal loan limits must carefully evaluate private loan terms, including interest rates, fees, and protections, to avoid long-term financial strain. Federal loans remain the safer choice when available, but private loans might be necessary. For more detailed insights, see this ascent student loans review.

How much can speech pathology students borrow, and what interest rates should they expect?

Speech pathology students can borrow up to $20,500 annually through federal graduate Direct Unsubsidized Loans, with a total maximum of $138,500 across all federal student loans, including undergraduate debt. The fixed interest rate on these loans is 7.54% starting in 2026, reflecting average interest rates on speech pathology student loans.

Notably, the One Big Beautiful Bill Act ends the Graduate PLUS Loan program for new borrowers as of July 1, 2026. This program once provided an option to borrow up to the full cost of attendance but is no longer available, limiting borrowing to Direct Unsubsidized Loans only.

Without Graduate PLUS Loans, students must budget carefully or explore other funding options such as private loans, scholarships, or employer tuition assistance. Private loans typically have variable interest rates ranging between 6% and over 13%, often higher than federal rates. Many students also balance part-time work to manage expenses beyond the federal loan limits.

Strategies to address the funding gap include applying for scholarships and understanding Income-Driven Repayment plans, which tie repayment rates to the original loan interest. For those seeking to reduce loan costs after graduation, researching student loan refinancing bonus offers may provide valuable options.

These maximum loan amounts for speech pathology students require proactive financial planning to cover tuition, fees, and living costs under the new borrowing restrictions.

How do you use the FAFSA to maximize federal aid before taking speech pathology loans?

Submit the Free Application for Federal Student Aid (FAFSA) as early as possible to maximize your federal aid eligibility before pursuing speech pathology loans. Early FAFSA submission is crucial since Pell Grants and campus-based funds operate on a first-come, first-served basis, which helps reduce out-of-pocket costs.

Accurate income and asset details improve your Expected Family Contribution (EFC), increasing access to need-based aid. Update FAFSA annually to maintain continuous eligibility, as many states and schools rely on this data for their aid programs.

Maximizing federal student aid before speech pathology loan applications includes exploring specific programs like the TEACH Grant and Public Service Loan Forgiveness.

Mississippi's Speech-Language Pathologist Forgivable Loan program is a notable example, covering tuition and fees for eligible master's students at public institutions but awarding only four spots per cohort each year. Meeting early deadlines is essential to secure this limited aid.

Use your FAFSA results to determine eligibility for Direct Subsidized Loans, which don't accrue interest while you're in school. Borrow only what's necessary after exhausting grants and scholarships.

If more funds are needed, consider federal Grad PLUS Loans, which offer favorable terms compared to private loans. Prioritizing federal aid can minimize long-term debt and repayment challenges.

For borrowers looking to reduce existing debt, learning how does student loan refinancing work can offer valuable options after graduation.

What special considerations apply to loans for speech-language pathology graduate and clinical programs?

Loans for speech-language pathology graduate and clinical programs require careful consideration due to the specialized nature and extended duration, typically two to three years. Clinical placements often include unpaid internships, delaying workforce entry and affecting loan repayment timelines.

Eligible federal loans include Direct Unsubsidized Loans and Grad PLUS loans, but borrowing limits can be high, so budgeting is essential to prevent excessive debt. Private loans may fill gaps but usually carry higher interest rates and fewer protections. Loan forgiveness programs like Public Service Loan Forgiveness (PSLF) offer relief for those working in qualifying health or educational settings.

Scholarships and grants targeting communication sciences and disorders students significantly reduce loan dependence. For example, the American Speech-Language-Hearing Foundation awards graduate scholarships from $1,000 to $25,000 annually. Early application for these funds can ease financial burdens during study.

Key points to consider:

- Program length and unpaid clinical hours delay repayment start.

- Federal loans offer higher limits but require prudent budgeting.

- Private loans have higher costs and fewer borrower safeguards.

- Loan forgiveness is available for qualifying clinical service.

- Scholarships can reduce loan reliance substantially.

Confirm your school's federal funding eligibility and carefully review all loan terms. Consult financial aid offices and leverage resources specific to speech pathology to optimize borrowing and ensure manageable repayment plans.

Which repayment plans work best for speech pathology salaries at different career stages?

Income-Driven Repayment (IDR) plans, such as Income-Based Repayment (IBR) and Pay As You Earn (PAYE), are well-suited for entry-level speech pathologists earning between $60,000 and $75,000.

These plans adjust monthly payments based on income, helping manage cash flow early in a career. A graduate earning $65,000, for instance, may pay about 10% of discretionary income, easing financial pressure while gaining experience.

Mid-career speech pathologists with salaries from $85,000 to $100,000 might prefer the Standard Repayment Plan or Graduated Repayment Plan. The Standard Plan offers fixed payments to repay loans within 10 years, while the Graduated Plan starts with lower payments that increase every two years, aligning with salary growth. Both plans typically reduce total interest compared to longer or income-driven plans.

Experienced professionals earning over $100,000 may benefit from refinancing to secure lower interest rates, especially when switching from federal to private loans with fixed APRs ranging from 4% to 14%.

However, refinancing should only be pursued if it lowers the rate without sacrificing federal loan protections. According to Forbes Advisor, private lenders' rates can be nearly twice those of federal Direct Unsubsidized Loans, so comparing rates is crucial.

Public Service Loan Forgiveness (PSLF) is another option for speech pathologists in public or nonprofit roles. By enrolling in IDR and making 120 qualifying monthly payments on time, they can achieve loan forgiveness and significantly reduce their debt.

What loan forgiveness and repayment assistance programs exist for speech-language pathologists?

Speech-language pathologists may access several federal programs to ease student loan debt. The Public Service Loan Forgiveness (PSLF) program is the most prominent, forgiving remaining federal Direct Loans after 120 qualifying monthly payments while employed full-time by a qualifying government or nonprofit employer. Over 800,000 borrowers in education and public service fields have benefited from PSLF, with more than $56 billion in relief.

Qualification for PSLF requires holding federal Direct Loans, full-time work at eligible organizations like government agencies or nonprofit hospitals, and making on-time payments under an income-driven repayment plan. Private loans are excluded.

Additional options include Perkins Loan Cancellation, which forgives a portion of Perkins Loans for certain public service roles, mainly for older loans, and the National Health Service Corps (NHSC) Loan Repayment Program, which offers up to $50,000 in repayment assistance for practitioners in designated Health Professional Shortage Areas.

Income-driven repayment plans such as Income-Based Repayment (IBR) and Revised Pay As You Earn (REPAYE) adjust monthly payments based on income and family size. They also provide loan forgiveness after 20 to 25 years of qualifying payments.

How can speech pathology borrowers refinance or consolidate loans to lower payments or rates?

Speech pathology borrowers have options to lower monthly payments or reduce interest rates by refinancing or consolidating their federal and private student loans. Federal Direct Consolidation Loans combine multiple federal loans into one, simplifying payments and often extending the repayment period.

While this can reduce monthly costs, it may increase the total interest paid over time. Private refinancing might offer lower interest rates based on creditworthiness and income, such as refinancing a $60,000 loan from 7% to 5% interest, potentially saving significant money in the long run.

It is important to consider career plans before refinancing. Federal benefits like income-driven repayment plans and Public Service Loan Forgiveness are lost when loans are refinanced through private lenders. Refinancing usually benefits graduates with steady incomes and good credit scores who want to minimize interest costs.

Employers have increased student loan repayment assistance programs by about 43% since 2019. Speech-language pathologists should explore these workplace benefits, as employer contributions can directly reduce loan balances and monthly payments.

Additional strategies include:

- Enrolling in income-driven repayment plans before consolidating to keep payments affordable.

- Researching state or professional association refinancing programs specifically for healthcare workers.

- Comparing fees, terms, and protections between federal and private refinance options to match personal financial goals.

What deferment, forbearance, and hardship options are available to speech pathology borrowers?

Speech pathology student loan borrowers have access to deferment, forbearance, and hardship options to manage repayment challenges effectively.

Deferment allows postponement of payments during qualifying periods like half-time enrollment in graduate speech pathology programs, unemployment, or economic hardship. Federally backed loans usually do not accrue interest during deferment periods.

Forbearance offers temporary relief when borrowers don't qualify for deferment but face financial difficulties or medical issues. Interest continues to accrue during forbearance, increasing overall loan costs. It comes in two types: discretionary, granted at the lender's discretion, and mandatory, required under circumstances such as high medical expenses. Forbearance terms typically last 3 to 12 months and can be renewed up to 36 months.

Hardship options include income-driven repayment plans such as Income-Based Repayment (IBR) and Pay As You Earn (PAYE), which adjust payments based on income and family size. These plans can reduce monthly payments to as low as $0 for borrowers experiencing reduced income or temporary unemployment.

Additionally, Public Service Loan Forgiveness (PSLF) allows loan forgiveness after 120 qualifying payments for those working in eligible public health roles, including speech pathology.

With the median salary for speech-language pathologists reaching $89,290 and a projected 19% job growth through 2032, these flexible repayment options are essential for managing loans while advancing careers.

How do student loans affect a speech pathologist's credit, licensing, and long-term finances?

Student loans play a critical role in the financial and professional lives of speech pathologists. Timely repayments help build a strong credit history and score, while missed payments can severely damage credit and increase future borrowing costs.

Defaulting on loans may lead to wage garnishment, tax refund offsets, or collections actions that linger for years, complicating access to housing or additional financing.

Although licensing boards usually do not directly penalize speech pathologists for student loan debt, financial difficulties stemming from unpaid loans can undermine professional stability.

Some states require disclosure of financial or legal issues during license renewal, making unresolved defaults a potential obstacle. Keeping loans in good standing supports both career longevity and professional credibility.

Large student loan balances often lead to high monthly payments. For example, a standard 10-year repayment plan on $150,000 of student debt can exceed $1,800 per month, which might consume over 25% of take-home pay in many areas. This strain reduces disposable income and affects overall financial well-being.

- Higher payments increase the risk of financial hardship.

- Income-driven or extended repayment plans lower monthly bills but result in more interest over time.

- Loan forgiveness programs offer relief but require strict adherence to qualifying criteria.

Refinancing for better interest rates and strategic budgeting is vital to maintain credit health and professional stability in speech pathology. Ignoring loans can jeopardize both financial and career goals.

Other Things You Should Know About

Yes, student loans for speech pathology studies often cover more than just tuition and fees. These loans can be used to pay for books, supplies, equipment, and living expenses during your program. Be sure to budget carefully to avoid borrowing more than necessary.

If you withdraw, you may need to repay any disbursed federal loans according to specific timelines and exit counseling requirements. Private lenders may have different policies, often requiring immediate repayment or continued monthly payments. Contact your loan servicer promptly to understand your options.

Interest paid on federal and many private student loans may be tax-deductible up to a certain limit, reducing your taxable income. To qualify, the loan must have been used for qualified education expenses in a speech pathology program. Keep records of your payments and consult IRS guidelines or a tax professional.

Your enrollment status can impact the type and amount of loans available. Most federal loans require at least half-time enrollment, while some private lenders may have different requirements. Dropping below half-time status could lead to loan repayment obligations starting sooner.