2026 How to Improve Your Chances of Student Loan Approval

Student Finance & Loan Expert

Many prospective graduate students face the challenge of securing a student loan despite having an unrelated undergraduate degree. Lenders often scrutinize applicants' credit history, income, and degree relevance, which can lead to denial or high interest rates. This barrier can delay educational and career goals. Understanding these obstacles is crucial to navigating the often complex loan approval process. This article outlines practical strategies to strengthen loan applications, improve creditworthiness, and present a compelling case to lenders, ultimately enhancing the likelihood of successful student loan approval for diverse academic and professional backgrounds.

- How do student loans work? Loan Basics

- What is the difference between federal and private student loans? Federal vs Private

- How do you qualify for student loans? Eligibility

- How do you apply for student loans and FAFSA? FAFSA Steps

- How much can you borrow for school? Borrowing Limits

- What affects student loan interest rates? Interest Rates

- Which repayment plans lower monthly payments? Repayment Plans

- How do loan forgiveness programs work? Forgiveness Programs

- When should you refinance or consolidate student loans? Refinance Options

- What happens if you miss student loan payments? Default Risks

How do student loans work?

Student loans are a key financial resource to cover educational expenses but must be repaid with interest. They come in two primary types: federal and private. Federal student loans, managed by the government, usually feature fixed interest rates, income-driven repayment plans, and potential loan forgiveness programs, making them suitable for many borrowers. In contrast, private loans from banks or lenders tend to have higher, variable rates and fewer borrower protections.

The student loan approval process in the United States varies depending on the loan type. Federal loans commonly don't require a credit check, increasing accessibility. Conversely, private lenders often perform rigorous credit evaluations and may ask for a co-signer if the borrower's credit history is limited.

Loan funds are typically disbursed directly to schools for tuition, fees, and sometimes living expenses. To learn more about how these loans can cover such costs, see can you use student loans for rent. Repayment usually starts after graduation or leaving school, with terms ranging between 10 and 30 years. Knowing how federal student loans work for borrowers can help in planning these payments effectively.

The average federal student loan debt per borrower was $39,547, increasing to $43,333 when including private loans (Education Data Initiative). To improve loan approval chances and manage borrowing wisely, students should:

- Complete the Free Application for Federal Student Aid (FAFSA) accurately and early.

- Check credit scores and improve them before applying for private loans.

- Compare interest rates and loan terms from various lenders.

- Limit borrowing to necessary expenses to reduce overall debt.

- Understand repayment plans to budget accordingly.

What is the difference between federal and private student loans?

Federal student loans, issued by the U.S. Department of Education, offer fixed interest rates set annually by Congress along with features such as income-driven repayment plans and loan forgiveness options. These loans do not require a credit check or co-signer for most students, making them accessible regardless of credit history. Examples include Direct Subsidized and Unsubsidized Loans as well as PLUS Loans for parents and graduate students. This accessibility is a key factor when comparing federal versus private student loans benefits.

In contrast, private student loans come from banks or credit unions with variable or fixed interest rates usually higher than federal loans. Approval often requires credit checks or co-signers, especially for those with limited credit history. Private lenders offer less flexible repayment options and fewer forgiveness programs. Terms and eligibility vary widely, so borrowers must compare offers carefully to find the best option.

Data shows a trend toward cautious borrowing, with only 38% of first-time, full-time undergraduates taking loans in 2020-21 and average loan amounts decreasing when adjusted for inflation. For students weighing how private and federal student loans differ, federal loans typically provide stronger consumer protections and more supportive repayment structures. Those with limited credit should maximize federal loan eligibility to improve approval chances and avoid the challenges private loans can present.

Students and families seeking guidance on borrowing without relying on parental help can learn how to get student loans without parents, an important step in navigating loan options confidently.

How do you qualify for student loans?

Qualifying for student loans in the United States involves meeting specific requirements for federal student loan approval or private lender criteria. For federal loans, applicants must be U.S. citizens or eligible noncitizens with a valid Social Security number, enrolled at least half-time in an eligible degree or certificate program, and maintain satisfactory academic progress. Completing the Free Application for Federal Student Aid (FAFSA) is required to determine eligibility and borrowing limits.

Private student loans assess credit history, income, and debt-to-income ratio more closely. Borrowers with strong credit scores or a creditworthy cosigner improve their chances and may receive better interest rates. As of 2025 Q4, 10.0% of federal student loan dollars were delinquent, compared to 1.62% of private loans in default, highlighting lenders' focus on credit risk. Applicants with limited credit may have difficulty qualifying but can explore federal options, which typically do not require credit checks for most loans.

Documentation such as proof of enrollment, identification, and financial information is essential. Some private lenders may require collateral or minimum income thresholds. To increase approval likelihood, prepare necessary paperwork and understand each loan's specific eligibility conditions. For families considering alternative funding, researching parent loans for college can offer additional support options to borrowers.

How do you apply for student loans and FAFSA?

To apply for federal student loans in the US, start by completing the Free Application for Federal Student Aid (FAFSA) online via the official government site. This step is crucial as it calculates your Expected Family Contribution (EFC) and determines eligibility for federal grants, work-study, and loans. Accurate financial details about you and your family are essential. If you're an independent student or a professional seeking graduate loans, include your income and employment information. Applications showing validated income and stable employment often receive better consideration, especially for Direct Unsubsidized loans. According to LendingTree's analysis of U.S. Department of Education data, borrowers with graduate and professional Direct Unsubsidized loans owe a combined $627.9 billion, emphasizing the need to demonstrate financial reliability at advanced levels.

After submitting FAFSA, review your Student Aid Report (SAR) carefully. Contact your school's financial aid office to correct errors or provide additional documents like tax returns or job verification. Learning the step-by-step guide to completing FAFSA application ensures a smoother process and reduces delays.

Private loans require extra research since lenders often check credit and income. Many lenders ask for a cosigner if credit is limited. Submitting all paperwork on time helps secure approval and ensures funds arrive by tuition deadlines. Students can also explore student loan refinance lenders for potential savings after borrowing.

Keep your information updated and report income changes during enrollment. Maintaining employment records supports ongoing eligibility for income-verified loan programs, maximizing your chances in a competitive lending environment.

How much can you borrow for school?

The amount you can borrow through federal student loans varies by loan type and educational level. Direct Subsidized Loans provide between $3,500 and $5,500 annually for undergraduates, depending on their year of study. Direct Unsubsidized Loans allow undergraduates to borrow up to $7,500 per year, while graduate students may borrow up to $20,500 annually. Direct PLUS Loans let parents or graduate students borrow up to the full cost of attendance minus other aid received.

- Federal loan limits are designed to prevent excessive debt while covering essential costs such as tuition, fees, housing, and supplies.

- Approximately 82% of U.S. student loan debt is federal, so most borrowers start here before considering private loans.

- Private loans lack standardized limits; lenders base borrowing caps on creditworthiness and income, leading to variation across borrowers.

An undergraduate student might reach a federal borrowing cap near $31,000 during their degree but can extend funding through PLUS loans if needed. Graduate students, who do not qualify for subsidized loans, often rely on higher unsubsidized limits and PLUS options.

It's important to evaluate your total educational expenses and borrow only what you need. Prioritizing federal loans first is wise because they usually provide better borrower protections and repayment options compared to private loans.

What affects student loan interest rates?

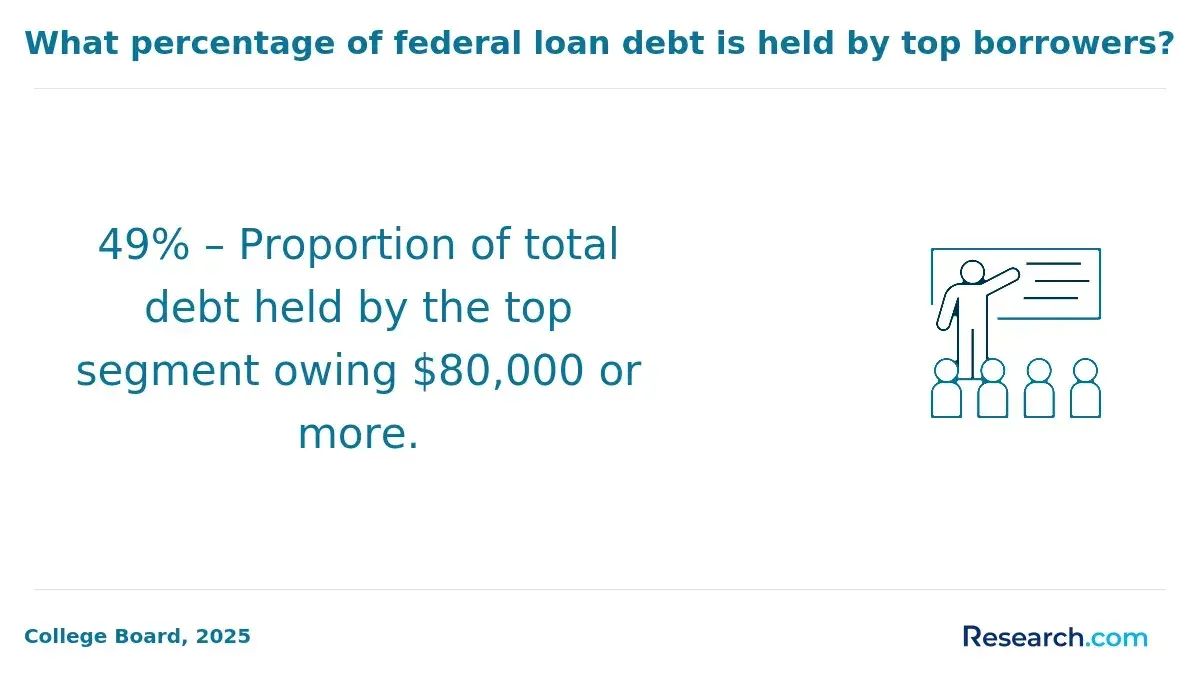

Student loan interest rates depend largely on factors lenders assess to gauge borrowing risk. A strong credit score can secure lower rates by showing a lower chance of default. Similarly, a manageable debt-to-income (DTI) ratio-ideally under 36%-improves loan terms since lenders favor borrowers with stable finances. Those eligible for Public Service Loan Forgiveness often carry an average debt of $88,260, suggesting that higher balances can be acceptable with steady qualifying employment (Education Data Initiative).

Loan type plays a significant role. Federal loans typically offer lower, fixed rates, while private loans may have variable rates influenced by credit profile and market conditions. Loan term length also impacts rates: shorter terms usually bring lower interest, while longer terms increase risk and rates.

Economic factors like the prime rate and inflation affect private loan rates indirectly. Borrowers who enroll in autopay or have creditworthy co-signers often benefit from additional rate reductions. Key strategies include:

- Maintaining or improving credit scores above 700

- Lowering DTI ratio below 36%

- Choosing federal loan options when possible

- Selecting shorter repayment terms

- Securing a creditworthy co-signer if needed

Which repayment plans lower monthly payments?

Income-driven repayment plans (IDR), including Income-Based Repayment (IBR), Pay As You Earn (PAYE), and Revised Pay As You Earn (REPAYE), lower monthly federal loan payments by capping them at a percentage of your discretionary income. Payments can drop to as low as 10-15% of adjusted gross income, sometimes under $100 monthly, based on income and family size.

Graduated repayment plans begin with smaller payments that increase biennially, ideal for borrowers expecting income growth. Extended repayment spreads loan repayment up to 25 years to reduce monthly amounts, suitable for larger balances.

Private student loans rarely offer IDR options. Instead, lower monthly payments often come from longer loan terms or a creditworthy co-signer, which improves approval chances and can lead to better interest rates. Nearly 90% of undergraduate private loans require co-signers, according to The Institute for College Access & Success, Private Student Loans: Facts & Trends.

Federal borrowers on IDR plans must submit annual income documentation for payment adjustments. Private loan borrowers should negotiate directly with lenders for term extensions or payment reductions, though these options vary widely.

To reduce monthly payments, consider these strategies:

- Applying for federal income-driven repayment plans.

- Opting for graduated or extended repayment schedules.

- Securing a strong co-signer for private loans.

- Discussing payment options with private lenders.

How do loan forgiveness programs work?

Loan forgiveness programs cancel all or part of your student loan debt once you meet specific eligibility requirements. These programs include Public Service Loan Forgiveness (PSLF), Teacher Loan Forgiveness, and income-driven repayment plan forgiveness. PSLF requires 120 qualifying monthly payments under a qualifying plan combined with full-time employment at a government or nonprofit organization. After this, the remaining federal loan balance is forgiven tax-free.

Income-driven repayment forgiveness cancels debt after 20 to 25 years of qualifying payments without employment requirements, but borrowers must update income documentation annually. Teacher Loan Forgiveness offers up to $17,500 for educators meeting service criteria in designated low-income schools.

Key factors for success include:

- Making qualifying payments consistently

- Maintaining accurate employment and income records

- Providing necessary documentation on time

Missing proper paperwork or lapses in qualifying employment can delay or disqualify forgiveness. Continuous enrollment in eligible programs, like the 64% of Walden University students using federal Title IV loans (Walden University, Student Loan Metrics 101, 2024), connects borrowers to federal aid and forgiveness opportunities. Staying in regular contact with loan servicers ensures you select the best federal forgiveness option for your career and repayment needs.

When should you refinance or consolidate student loans?

Borrowers with federal student loans disbursed between July 1, 2025, and June 30, 2026, face interest rates of 6.39% for undergraduate Direct loans, 7.94% for graduate Direct Unsubsidized loans, and 8.94% for PLUS loans, according to the Education Data Initiative. If a private lender offers significantly lower rates, refinancing could reduce your monthly payments or overall loan cost.

Refinancing benefits those with stable income and strong credit, as private lenders assess credit history. It replaces federal protections such as income-driven repayment plans and loan forgiveness. For borrowers seeking to simplify loan management without losing federal benefits, consolidating through a Direct Consolidation Loan remains a viable option.

Consider refinancing or consolidating if:

- You want to move from variable to fixed interest rates.

- Your credit score has improved since first borrowing.

- You aim to lower monthly payments by extending the loan term.

- You prefer one monthly payment instead of managing multiple federal loans.

- You prioritize savings on interest over maintaining federal protections.

Comparing interest rates and loan terms carefully is crucial. For example, refinancing a PLUS loan at 8.94% with a private lender's offer of 5.5% fixed rate may yield significant long-term savings. However, consolidating when rates remain steady might not reduce costs. Evaluate your credit, finances, and repayment goals to choose the most effective approach for your needs.

What happens if you miss student loan payments?

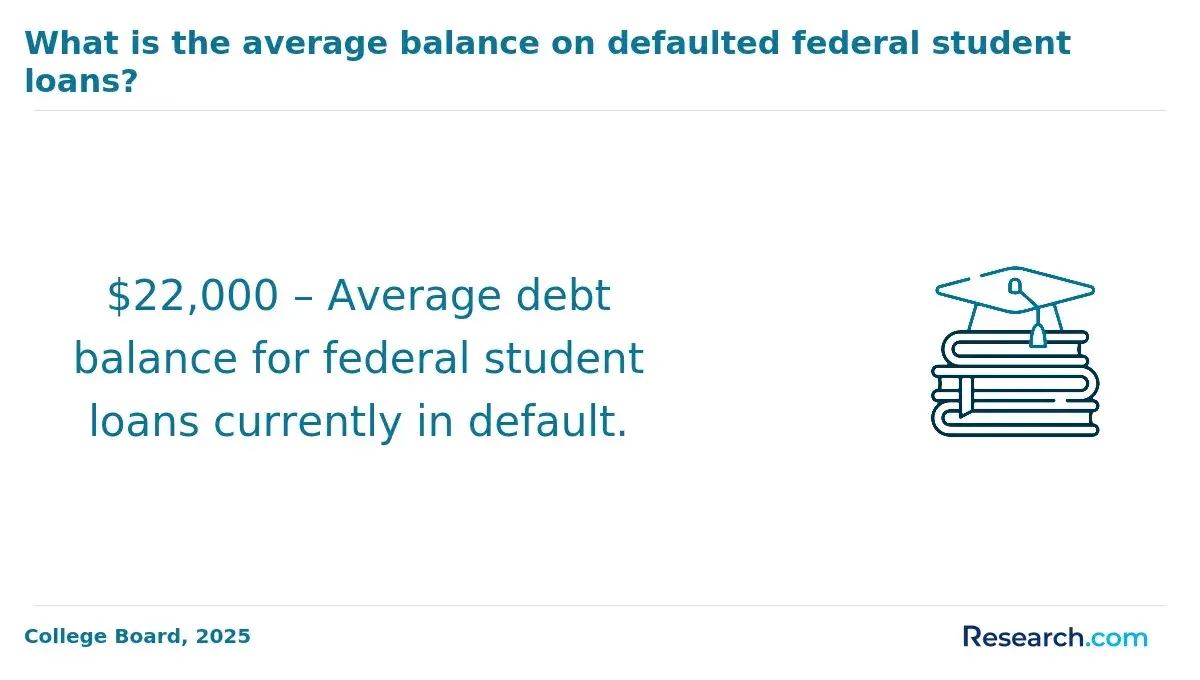

Missing student loan payments trigger immediate financial and credit consequences. After a missed payment, your loan becomes delinquent, which is reported to credit bureaus and lowers your credit score. After roughly 270 days of missed payments, the loan enters default. Default can lead to wage garnishment, tax refund withholding, and higher collection fees-actions taken without court involvement.

Borrowers struggling to pay should contact their loan servicer promptly to discuss options like income-driven repayment plans or forbearance. These solutions can pause or reduce payments temporarily and help prevent default and its severe consequences.

Defaulted federal loans lose eligibility for benefits such as income-driven plans and Public Service Loan Forgiveness (PSLF). Despite over $46.8 billion forgiven overall, only about 3.3% of PSLF applications have been approved (Education Data Initiative). This low approval rate emphasizes the importance of staying current on payments and strictly following program requirements.

Missed payments also increase the principal balance through capitalized interest, which raises long-term costs. Private loans differ, often imposing immediate late fees and possibly accelerating loan due dates.

Students and graduates facing financial hardship should evaluate repayment alternatives, including deferment, forbearance, or switching to income-driven repayment. Acting early can preserve credit standing and maintain eligibility for forgiveness programs.

- Delinquency reported after one missed payment

- Default after about 270 days of non-payment

- Income-driven plans and forbearance can offer relief

- Only 3.3% PSLF approval rate highlights strict criteria

- Private loans may have immediate fees and accelerated due dates

Other Things You Should Know About

Yes, having a cosigner can significantly improve your chances of getting approved for a private student loan. Lenders often require a cosigner with a strong credit history and stable income to reduce their risk, especially if the borrower has limited credit or income. This can lead to higher loan approval rates and potentially better loan terms.

Credit history plays a critical role in private student loan approval, as lenders evaluate your ability to repay based on past financial behavior. A strong credit history, with on-time payments and low debt levels, increases the likelihood of approval and better interest rates. Federal student loans generally do not require credit checks, but private loans almost always do.

Part-time students can qualify for certain student loans, although eligibility and loan amounts may differ from full-time students. Federal loans typically require at least half-time enrollment, while private lenders vary in their criteria. It's important for part-time students to confirm eligibility with their school's financial aid office or the loan provider.

Yes, student loans impact your credit score because they appear as debts on your credit report. Making timely payments can improve your credit history, while missed or late payments can damage your score. Managing student loans responsibly is important for maintaining good credit over time.