2026 Can Student Loans Pay for Professional Equipment?

Student Finance & Loan Expert

Imagine enrolling in a graduate program that requires costly specialized equipment, such as cameras for film studies or software for design courses. Many students wonder if federal or private student loans can cover these essential professional tools. Understanding which expenses qualify can prevent financial pitfalls and ensure appropriate funding.

This ambiguity often delays enrollment decisions or burdens students with unexpected out-of-pocket costs. This article clarifies the rules around using student loans for professional equipment, helping prospective students make informed financial decisions and avoid complications related to loan disbursement and legitimate expense coverage.

- Can student loans be used to buy professional equipment for school or training? Student Loans for Professional Equipment

- What types of professional equipment qualify as allowable education expenses under federal rules? Allowable Professional Equipment Types

- How do federal and private lenders define "cost of attendance" for equipment purchases? COA Equipment Rules: Federal vs. Private

- Are laptops, cameras, and tools for my major treated differently from general electronics? Funding Rules for Laptops, Cameras, & Specialized Major Tools

- What documentation do schools or lenders require to approve equipment paid with student loans Required Documentation for Funding Approval

- How do borrowing limits and financial aid packaging affect funding for professional equipment? Impact of Borrowing Limits & Financial Aid Packaging

- Can I use student loan refunds to buy equipment, and what are the risks? Risks of Using Loan Refunds for Equipment

- Are professional licensing exam fees, software subscriptions, and online tools covered by loans? Loan Coverage for Exams, Software, and Digital Tools

- How should I compare financing options for equipment: student loans vs. 0% cards or payment plans? Student Loans vs. Interest-Free Credit for Equipment Purchases

- How does borrowing for equipment impact repayment, forgiveness eligibility, and long-term costs? Repayment and Forgiveness for Equipment Debt

Can student loans be used to buy professional equipment for school or training?

Student loans can cover the purchase of professional equipment if it is essential for your course or training program. This applies to items necessary for completing coursework or acquiring skills tied to your academic or vocational goals. Examples include laptops for computer science students, cameras for film studies, or lab tools for engineering and medical training.

Using student loans to purchase training equipment is generally allowed when the equipment is approved as part of your cost of attendance.

Professional equipment needs vary by field but often include tools, technology, software, or machinery that support learning. Art students might finance high-cost materials or software licenses, while culinary students could buy specialized kitchen appliances. However, equipment unrelated to your education, such as personal electronics or items not mandated by your program, should not be bought with loan funds.

According to the College Board, the average total cost of attendance for full-time graduate students reached $29,160, covering tuition, fees, room, board, and required equipment. This highlights that non-tuition expenses like professional equipment form a substantial part of what loans can cover. Make sure to verify your school's cost of attendance allowance for supplies by consulting your financial aid office and maintaining receipts for compliance and budgeting.

For broader financial planning, you might wonder if can FAFSA cover rent or similar expenses beyond tuition and equipment.

What types of professional equipment qualify as allowable education expenses under federal rules?

Professional equipment purchased with federal student loans must be a direct requirement of your program of study to qualify as allowable education expenses under federal guidelines. Eligible items typically include essential tools demanded by coursework or licensing, such as stethoscopes and medical references for nursing students or laptops and secure devices for social work field placements.

Allowable education expenses for student loans federal guidelines require that equipment be explicitly required or recommended by your school or accrediting body. This includes lab instruments, drafting tools for architecture, cameras for media studies, and specialized calculators for engineering or finance. Items that support hands-on skill development in your profession qualify; personal or general-use items do not.

Maintaining documentation, like receipts and school communications, is critical to prove these expenses are necessary. This protects you during loan servicing reviews and audits. Since the One Big Beautiful Bill Act limits federal graduate loan borrowing to $20,500 annually and $100,000 total starting July 1, 2026, students in costly fields should plan purchases carefully.

Students seeking options to finance essential professional equipment with less-than-ideal credit may explore resources like best student loans for bad credit to supplement federal funds when needed.

In summary, professional equipment eligible for student loans in the US must be indispensable, well-documented, and aligned with federal loan restrictions to qualify as allowable education expenses.

How do federal and private lenders define "cost of attendance" for equipment purchases?

Federal lenders define cost of attendance equipment expenses in the US federal student loans strictly. These include tuition, fees, housing, food, transportation, and necessary supplies or equipment required for coursework. Purchases like stethoscopes for medical students or software for graphic design students qualify only if mandated by the academic program and approved by the school's financial aid office.

By contrast, private student loan guidelines for professional equipment are more flexible. Private and nonfederal lenders often allow a broader range of tools and technology supporting education or career goals, even if not explicitly required by the institution. This may cover laptops, cameras, or vocational training machines. However, these loans bear higher interest rates and less favorable repayment terms, increasing financial risk.

Private and other nonfederal loans currently make up about 14% of the $102.6 billion borrowed for postsecondary education, showing a significant share falls outside federal rules on allowable costs. Students should confirm equipment eligibility with their financial aid office when considering federal loans and carefully compare terms before borrowing privately.

Those interested in financial aid for adults returning to college will find it crucial to understand these distinctions. Awareness of differences between federal and private lenders helps students responsibly finance necessary professional equipment.

Are laptops, cameras, and tools for my major treated differently from general electronics?

Laptops, cameras, and tools related specifically to your major often qualify for student loan funding when they are essential to your coursework. Federal student loans cover necessary educational expenses, including specialized equipment required for your field of study. For example, a nursing student's medical instruments or a film student's professional camera can be eligible. This is a key consideration when assessing student loans coverage for major-specific equipment.

General electronics, such as a basic laptop or standard accessories, may face closer scrutiny unless clearly vital to your program. In contrast, professional tools linked directly to your curriculum or clinical assignments usually justify the expense. Art majors might finance advanced design tablets, while journalism students could use loans for cameras needed for reporting. The important factor is proving the item's academic necessity.

Graduate students in fields demanding extensive gear often borrow to cover these costs; about 61% of graduate students use federal loans, with average debts around $280,000 in intensive programs like medicine and law. This highlights the investment in both tuition and professional tools eligibility for student loan expenses.

To ensure coverage, keep these tips in mind:

- Review your school's financial aid definition of educational expenses.

- Keep receipts and documentation linking purchases to program requirements.

- Consult your financial aid office before buying costly equipment.

- Evaluate how critical the item is for completing assignments or clinical work.

Proper documentation and justification are vital to secure loan approval for major-specific gear. For additional financial strategies, students can explore options among the best banks for student loan refinancing.

What documentation do schools or lenders require to approve equipment paid with student loans?

To secure student loans for professional equipment, schools and lenders require detailed documentation. This typically includes an invoice or receipt that outlines the exact cost of the necessary tools or equipment connected to your educational program. For example, nursing students must provide lists from approved vendors showing items like stethoscopes or clinical uniforms.

Institutions often ask for a formal letter or purchase order from the relevant department or program coordinator. This document should verify that the equipment is mandatory for completing the program and is part of the total cost of attendance.

Lenders also need proof that the equipment costs fit within the approved educational budget. This might involve submitting budget sheets, cost breakdowns, or tuition and fees disclosures that include professional tools. For instance, Doctor of Physical Therapy programs have average costs between $108,212 and $126,034, which factor in these expenses.

Students may also need to provide course syllabi or program requirements that specify necessary equipment purchases. If financing multiple items, it helps to submit a comprehensive list and vendor quotes to ensure smoother loan approval and prevent delays.

How do borrowing limits and financial aid packaging affect funding for professional equipment?

Federal student loan limits directly impact how much funding is available for professional equipment through borrowing. Dependent undergraduates are capped at borrowing $5,500 in their first year, with this limit increasing gradually each year to a total maximum of $31,000. Graduate students have a higher annual limit of $20,500 for Direct Unsubsidized Loans. These caps restrict the ability to use loans for non-tuition expenses such as specialized tools or technology needed for career programs.

Financial aid packaging also influences funding since schools focus primarily on tuition, fees, room, and board in their calculations. Equipment and supplies are included but usually constitute a smaller share of the budget. For example, average debt for bachelor's degree earners is around $29,560, while annual tuition and fees average $14,300, indicating that loans also cover other necessary costs. Heavy tuition expenses can reduce how much loan money remains available for purchasing professional equipment.

Students requiring costly tools should examine their full cost of attendance and understand how aid is allocated. They might consider supplemental funding options or scholarships aimed specifically at equipment costs if loan limits and packaging fall short.

- Dependent undergraduate borrowing limits: $5,500 first year, up to $31,000 total

- Graduate annual Direct Unsubsidized Loan limit: $20,500

- Tuition and fees often consume a large portion of loan amounts

- Alternative financing may be needed for costly equipment

Can I use student loan refunds to buy equipment, and what are the risks?

Student loan refunds can be used to purchase professional equipment if these expenses are approved by your school's financial aid office and count toward your cost of attendance. Items such as computers, specialized software, tools, or lab equipment tied to your academic program generally qualify. However, spending loan refunds on unrelated or non-essential equipment may violate loan terms and cause issues.

Consider these risks before using loan funds for equipment:

- Increased debt burden requires careful budgeting, especially for costly items.

- Equipment bought personally may lack institutional warranty or insurance protection if lost or damaged.

- Misuse of funds might trigger financial aid suspension or accelerated loan repayment if discovered during audits.

For instance, an art student purchasing specialized design software aligns with approved expenses, while buying unrelated consumer electronics does not. Always consult your financial aid office to verify which purchases are allowed.

Financially, borrowing for equipment involves balancing immediate needs against future debt. Notably, total education borrowing in the U.S. declined significantly over the past decade, shifting more costs to grants, tax benefits, and out-of-pocket expenses. This trend highlights the importance of exploring alternative funding before increasing loan debt for equipment purchases.

Are professional licensing exam fees, software subscriptions, and online tools covered by loans?

Professional licensing exam fees, software subscriptions, and online tools can often be covered by student loans, but eligibility depends on the loan type and your educational institution's policies. Federal student loans generally allow coverage of expenses like CPA, bar, or medical licensing exams when these are required for coursework and billed through your school. Private loans may offer similar benefits but usually require additional borrower verification and are less uniform.

Software essential for your academic or professional development-such as design tools, statistical software, or coding platforms-may qualify if directly tied to your course requirements. Online tools for research or skill-building are also eligible with proper documentation indicating necessity. Keeping detailed proof that these expenses are mandatory can improve approval chances.

Loan funds typically do not cover licensing or renewal fees after graduation unless you are enrolled in an eligible continuing education program. Not all schools permit loan usage for optional software or tools, so confirm your institution's guidelines first.

Graduate and professional students often encounter these costs frequently. Research from SoFi and the Education Data Initiative shows individuals with nearly $280,000 in graduate debt can benefit from financing these expenses as investments given their high lifetime earning potential.

- Professional exam fees billed through your school

- Necessary software subscriptions and coding platforms

- Online tools tied to coursework or research

- Restrictions around postgraduation renewals and optional tools

How should I compare financing options for equipment: student loans vs. 0% cards or payment plans?

When choosing equipment financing, consider total cost, repayment terms, and how it affects your overall debt. Student loans often feature fixed interest rates, deferment options, and borrower protections not usually found in credit cards or vendor payment plans.

0% interest credit cards are useful for short-term financing if fully paid within the promotional period, but late payments can trigger high retroactive interest. Vendor payment plans break costs into installments but might include fees or higher effective rates compared to federal student loans.

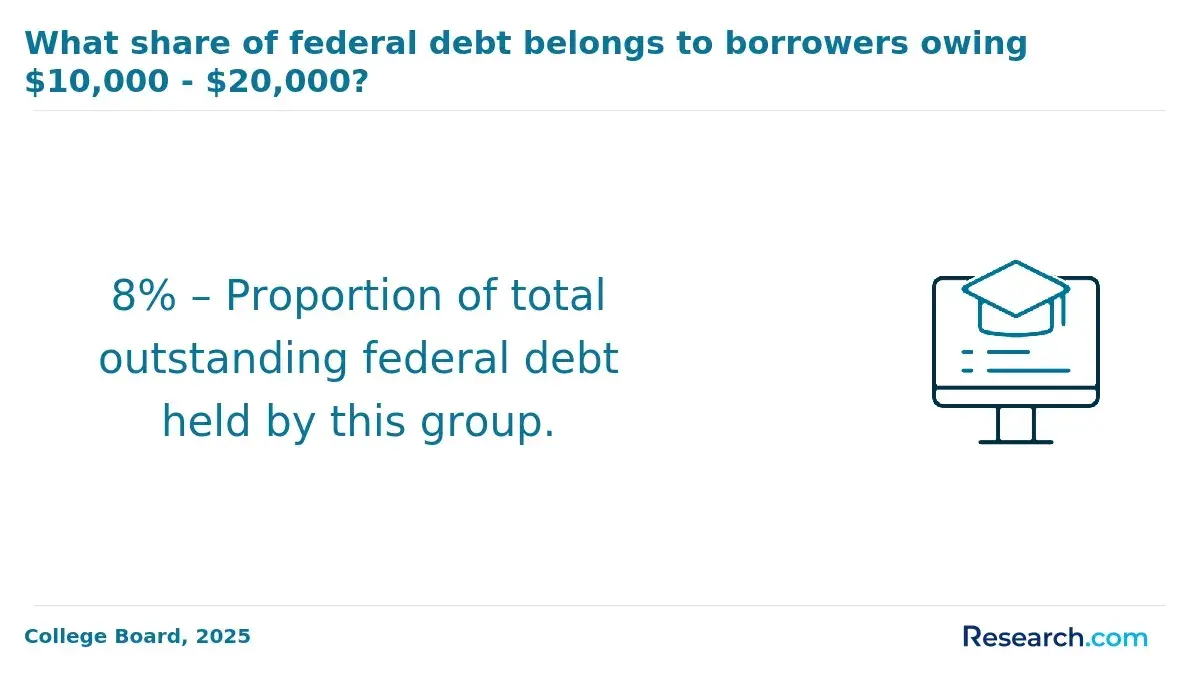

Most federal student loans for equipment fall under modest amounts; 32% of borrowers owed less than $10,000 and 21% owed $10,000-$20,000, though these groups held only 12% of total federal debt (College Board Research). This suggests loans for tools and supplies tend to be smaller, fitting professional equipment needs within these ranges.

- Cost over time: Factor in all fees and interest for each financing method.

- Repayment flexibility: Federal loans may offer income-driven plans and deferment in hardship.

- Credit impact: Credit cards affect credit scores differently than student loans.

- Loan purpose restrictions: Confirm equipment qualifies under your loan's educational expense criteria.

Match your repayment timeline and financial capacity with the option chosen. While 0% cards minimize short-term costs, student loans typically provide lower interest and borrower safeguards for longer repayment periods.

How does borrowing for equipment impact repayment, forgiveness eligibility, and long-term costs?

Borrowing student loans to cover the cost of professional equipment increases your total loan amount, which directly affects repayment terms and forgiveness eligibility. Equipment expenses are included in your cost of attendance, meaning your principal balance rises, leading to higher monthly payments and potentially more interest accrued over the life of the loan. For instance, adding $5,000 for specialized tools or technology often extends your repayment period or increases monthly installments.

Forgiveness programs typically require that loan funds pay for qualified educational expenses. However, federal guidelines are tightening definitions of allowable costs, and not all equipment purchases automatically qualify. This uncertainty can risk forgiveness if the equipment is deemed nonessential later on. It's important to confirm with your financial aid office whether your specific equipment costs qualify.

Rising borrowing for equipment adds to overall student debt levels, contributing to about $87.2 billion lent annually to postsecondary students, with a 10.0% delinquency rate reported by the Education Data Initiative. Policymakers are considering stricter rules about allowable equipment expenses, which could impact borrowing limits and future loan forgiveness programs.

To manage these challenges, consider the following:

- Request detailed cost breakdowns to ensure equipment costs fall under the cost of attendance.

- Consult loan servicers and school advisors about how equipment loans affect forgiveness eligibility.

- Plan for higher repayments by including equipment costs in your loan calculations.

Other Things You Should Know About

Federal student loans generally require you to be enrolled at least half-time to remain eligible. If you are enrolled less than half-time, you may lose access to federal loans, which can limit your ability to use those funds for professional equipment. Private loans may have different requirements, so reviewing the lender's terms is important.

Using student loan money to buy professional equipment does not change the length or start of your federal loan grace period. The grace period begins after you drop below half-time enrollment or graduate, not based on how you spend the loan funds. It remains important to keep track of your enrollment status.

Student loan proceeds are not considered taxable income regardless of how they are used, including for professional equipment. You do not have to report loan disbursements as income on your tax returns. However, loans must be repaid according to the terms, independent of tax implications.

It may be possible to increase your loan amount through a process called loan adjustment or by applying for an additional loan, but this depends on your school's policies and lender approval. You will need to demonstrate that the extra funds are necessary and fit within your cost of attendance. Always consult your financial aid office before borrowing more.