2026 Best Emergency Student Loan Options

Student Finance & Loan Expert

Unexpected expenses or sudden changes in financial circumstances can leave prospective graduate students scrambling for immediate funding. Without access to emergency student loans, important academic opportunities may be delayed or lost. Navigating emergency loan options quickly and effectively is critical for those balancing work and study commitments. This article examines the best emergency student loan options available, focusing on eligibility, application speed, and repayment flexibility. It aims to equip readers with clear, actionable information to secure funds promptly and reduce the financial stress of advancing education under tight timelines.

- What is an emergency student loan and when should students consider using one? What is an emergency

- Which emergency student loan options are available from the federal government? Which emergency student loan

- How do campus-based emergency loans and institutional payment plans work? How do campus-based emergency

- What private emergency student loan and fast-funding options can borrowers access? What private emergency student

- How do interest rates, fees, and repayment terms compare across emergency loan choices? How do interest rates,

- What eligibility, credit, and enrollment requirements apply to emergency student loans? What eligibility, credit, and

- How can students apply quickly for emergency loans and document urgent financial need? How can students apply

- What alternatives to borrowing exist for urgent college expenses and tuition gaps? What alternatives to borrowing

- How do emergency student loans affect future financial aid, credit scores, and debt load? How do emergency student

- What strategies help prioritize repayment and avoid default on emergency student loans? What strategies help prioritize

What is an emergency student loan and when should students consider using one?

An emergency student loan is a short-term financial resource meant to cover unexpected education-related expenses like sudden tuition hikes, urgent textbook purchases, housing crises, or emergency travel. These loans are particularly useful when standard aid such as grants, scholarships, or work-study programs are insufficient or unavailable. Knowing when to apply for an emergency student loan ensures students can avoid disruptions like enrollment holds or late fees.

Emergency student loans often feature faster approval and smaller amounts than regular loans, sometimes with lower interest rates or flexible repayment terms. However, assessing the necessity is critical to prevent unnecessary debt accumulation. For those in need, exploring campus emergency funds or short-term assistance can be a valuable first step.

Students experiencing cash shortages for unplanned housing expenses may want to consider options like student loans for off-campus rent. These loans can bridge gaps while maintaining educational progress.

Key advice before seeking emergency loans includes:

- Confirming the emergency directly relates to education

- Reviewing all loan terms thoroughly to avoid high interest rates

- Planning repayment schedules aligned with expected income

- Exploring available campus-based emergency supports

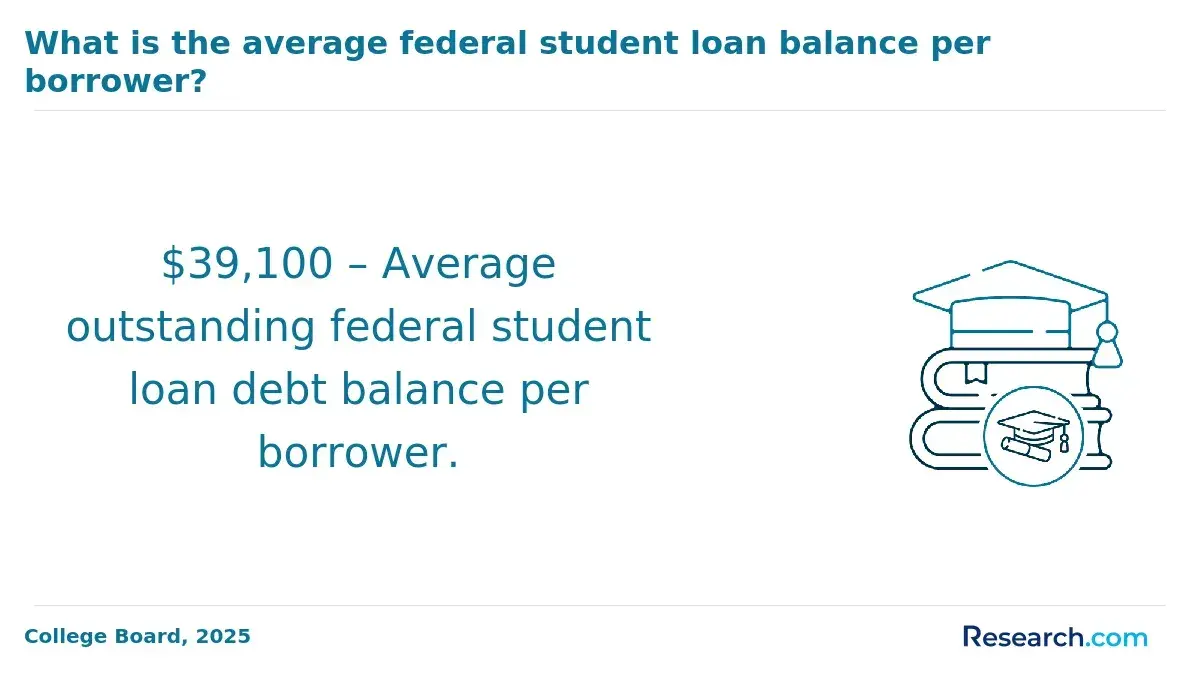

Understanding emergency student loan options in the United States is vital, especially since undergraduate and graduate aid totals billions annually. Emergency loans effectively supplement timely financial support when typical funding falls short.

Which emergency student loan options are available from the federal government?

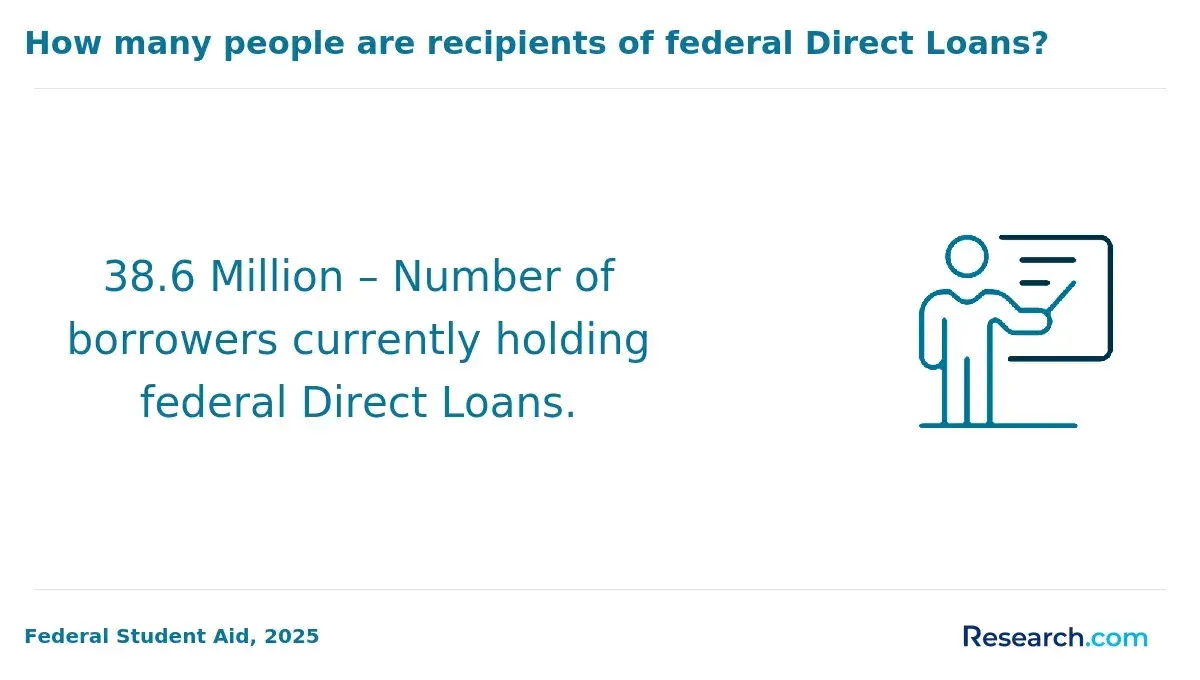

The federal government provides emergency student loan options to help borrowers facing urgent financial challenges. The primary choice is the Direct PLUS Loan for Graduate or Professional Students and Parents, which offers eligible borrowers additional funds beyond their original loan limits. This flexibility is crucial for covering sudden expenses during the academic year, such as medical bills or housing emergencies.

Another useful resource is the Federal Direct Unsubsidized Loan, available to both undergraduate and graduate students without requiring proof of financial need. While not specifically labeled as an emergency loan, it can be accessed to handle unforeseen expenses when other aid falls short.

Those struggling to repay existing debts can explore the Federal Student Loan Deferment and Forbearance programs. These programs do not provide new funds but allow temporary suspension or reduction of payments, easing immediate financial stress and freeing resources for emergency costs.

Emergency grant programs funded by the federal government may also provide support, although eligibility depends on the institution. As part of the broader picture of us government student loan relief programs, nearly 19% of undergraduates reported difficulty finding $500 for unexpected expenses in 2020, highlighting the importance of these options.

When applying for federal emergency student loan options, borrowers should:

- Review eligibility and borrowing limits of Direct PLUS and Unsubsidized Loans.

- Understand interest rates and repayment terms.

- Consult their school's financial aid office for personalized advice and potential emergency grants.

Students and graduates looking for alternative financing options might consider private student loans without parents, which can be found through resources like private student loans without parents.

How do campus-based emergency loans and institutional payment plans work?

Campus-based emergency loans in California provide short-term financial aid to students facing urgent expenses such as housing, tuition, or medical bills. These loans often feature low or zero interest rates with flexible repayment terms, making them more accessible compared to private alternatives. Students typically apply through their school's financial aid office, which assesses their immediate needs and enrollment status before approval. Repayment may begin after graduation or school departure, or be deferred while enrolled.

Institutional payment plan options for emergency aid allow students to split tuition and fees into smaller monthly installments without accruing interest or traditional borrowing costs. This approach prevents large lump-sum payments and limits dependence on emergency loans or credit cards.

Campus-based loans and institutional payment plans offer more controlled and lower-risk financial solutions compared to private emergency student loans. Private loans, which constitute about 8-9% of outstanding education debt according to the Education Data Initiative's 2026 "Student Loan Debt Statistics," often come with higher financial stress and repayment difficulties.

Some schools may waive fees or provide interest-free loans in emergencies, while others require prompt repayment. Students should act quickly and maintain communication with their financial aid offices to access assistance. For additional support, exploring resources like scholarships and grants for adults returning to education can supplement emergency aid.

What private emergency student loan and fast-funding options can borrowers access?

Private emergency student loan lenders with fast approval offer quick funding options designed to cover urgent expenses such as rent, utilities, and medical bills. These loans typically range from $500 to $5,000 depending on creditworthiness and lender policies. Borrowers can often receive approval and disbursement in under 72 hours through automated underwriting and electronic applications.

These loans tend to have higher interest rates and shorter repayment terms compared to federal emergency loans, making it important to review eligibility criteria carefully. Many lenders target students with good credit or those who have co-signers, while peer-to-peer emergency loans also provide alternatives for students without strong credit history.

Institutional aid programs commonly offer grants under $1,000 for short-term relief addressing housing, food, and transportation needs. These grants support rapid intervention but may not cover all costs, which private loans can supplement with larger amounts.

Borrowers should evaluate potential trade-offs, including origination fees and higher interest, and compare private offers thoroughly. For those seeking longer-term financial strategies, understanding student loan refinance requirements can provide additional options to manage debt effectively.

How do interest rates, fees, and repayment terms compare across emergency loan choices?

Emergency student loans offer much lower interest rates than credit cards, which often exceed 20% APR. Federal emergency student loans usually range from 3% to 7% interest, while private loans vary from 5% up to 15% or more, depending on creditworthiness. Fees also differ significantly: federal programs typically charge little to no origination fees, whereas private lenders may impose fees between 1% and 5% of the loan amount.

Repayment terms span from 6 months to 10 years, offering more flexibility than credit cards. Federal loans may include a six-month grace period after graduation or loan disbursement, giving borrowers time to stabilize their finances. Private emergency loans tend to have shorter repayment windows and less flexibility.

Key factors to consider include:

- Interest rates: Federal loans offer the lowest fixed rates, reducing long-term costs.

- Fees: Low or no fees on federal loans keep upfront costs down; private loans often increase total repayment with fees.

- Repayment flexibility: Federal options often include deferment or income-driven plans that ease financial burdens.

According to the Federal Reserve's "Economic Well-Being of U.S. Households" report, 48% of adults with education debt also carry credit card debt. This highlights the risk of using high-interest credit cards during emergencies and the value of emergency student loans structured with lower rates and fairer terms.

What eligibility, credit, and enrollment requirements apply to emergency student loans?

Emergency student loans require applicants to meet specific eligibility standards tied to enrollment, credit, and financial need. Borrowers must be enrolled at least half-time in an accredited institution that participates in federal student aid programs, covering undergraduate, graduate, and professional fields. Some loan options also support recent graduates experiencing urgent financial hardship.

Credit checks vary by loan type. Federal emergency loans usually do not require credit verification, making them available to those with limited or poor credit history. Private lenders often require a good credit score (typically 650 or higher) or a creditworthy co-signer, which is important for students without established credit.

Income qualifications emphasize proof of urgent financial need caused by unexpected expenses like medical bills, income loss, or housing issues. Documentation validating the emergency is often necessary. Federal borrowers frequently qualify for Income-Driven Repayment (IDR) plans after receiving funds, allowing manageable repayments relative to income. According to the Federal Reserve's 2025 report, about 30% of federal loan borrowers actively use IDR plans, highlighting their value as a financial safety net.

Applicants should prepare to show proof of current enrollment, identification, and evidence of financial hardship. Many programs also require maintaining satisfactory academic progress to continue receiving assistance.

- Enrollment requirements include half-time status at an accredited institution.

- Federal loans often do not involve credit checks; private loans do.

- Emergency need must be documented, linked to unforeseen financial crises.

- IDR plans assist federal borrowers in managing repayment based on income.

- Proof of enrollment and academic progress is commonly required.

How can students apply quickly for emergency loans and document urgent financial need?

Students needing emergency loans can apply quickly through online platforms offered by federal and private lenders, often designed for urgent financial situations. Universities frequently provide bridge or short-term loans with fast approval, requiring a simple application along with proof of enrollment and documentation of financial need.

To document urgent financial need, students should prepare:

- Recent bank statements or pay stubs showing insufficient funds

- Invoices for emergency expenses like medical bills, rent, or tuition

- A letter from a school financial aid officer or employer verifying urgency

- Proof of enrollment or course registration

Electronic submission of these documents is accepted by some lenders, speeding up the process. Federal emergency options such as Direct PLUS loans or temporary emergency grants usually require less documentation, mainly proof of enrollment and a brief financial hardship statement.

The Institute for College Access & Success (TICAS) report highlights a 47% rise in private student borrowing between 2014-15 and 2022-23. This reflects increased reliance on private short-term loans when federal aid is inadequate or unavailable.

Loan disbursement times vary; some private lenders release funds within 24 to 48 hours if documentation is complete. It is important to verify lender reputation and loan terms, as emergency loans often have higher interest rates and fees.

Choosing lenders with streamlined online systems and being prepared with documentation can help expedite access to emergency funding under financial stress.

What alternatives to borrowing exist for urgent college expenses and tuition gaps?

For urgent college expenses and tuition shortfalls, there are several alternatives to borrowing, including emergency grants, scholarships, payment plans, and institutional aid. Emergency grants, often offered by colleges and nonprofit groups, do not require repayment and typically cover unexpected costs such as textbooks or housing. For instance, Georgia State University's Panther Retention Grant provides emergency funds under $1,500. Research indicates that more than 86% of students receiving such grants either graduated or stayed enrolled after one year, demonstrating their effectiveness.

Scholarships focused on immediate financial needs or targeted student groups can also provide quick, non-debt assistance. Students are encouraged to consult their financial aid offices for expedited applications to these emergency scholarships.

Institutions sometimes offer tuition payment plans that break down the total cost over several months, usually with minimal or no interest, easing the burden of lump-sum payments. Work-study and campus employment programs allow students to earn money for urgent needs without increasing debt.

Community organizations, including local nonprofits and religious groups, might offer financial aid or goods that help alleviate immediate budget pressures. Additionally, students may negotiate with college billing or financial aid offices for short-term deferrals or reduced payments to avoid borrowing.

- Emergency grants under $1,500 correlate with 86% retention or graduation rates

- Emergency scholarships provide fast, non-loan aid for specific needs

- Tuition payment plans reduce upfront costs without interest

- Work-study and campus jobs generate earned income for urgent expenses

- Community aid and payment negotiations help bridge short-term financial gaps

How do emergency student loans affect future financial aid, credit scores, and debt load?

Emergency student loans increase your debt load immediately and can limit eligibility for future financial aid. Many aid programs assess total student debt before approval, so taking out emergency loans may reduce your chances of qualifying for grants or subsidized loans. This can create a cycle where additional debt leads to more borrowing, complicating long-term financial management.

How you handle emergency loans affects your credit score. Making timely payments can help build credit, but late or missed payments damage your credit profile and raise future borrowing costs. Unlike federal student loans, some emergency loans have higher interest rates and fewer flexible repayment options, increasing risks to your credit health.

Growing debt from emergency loans often results in longer repayment periods and more interest paid overall. According to Federal Reserve 2025 data, 29% of adults with education loans feel their debt is "not at all" worth it, especially those who didn't finish their degree. This highlights the financial burden of relying on loans for emergencies without completing education to boost earning potential and repayment ability.

Before opting for emergency student loans, consider alternatives such as:

- Emergency grants

- Family support

- Low-interest personal loans

If borrowing is necessary, choose loans with borrower protections like income-driven repayment or deferment options to maintain financial stability during and after your education.

What strategies help prioritize repayment and avoid default on emergency student loans?

Managing repayment of emergency student loans effectively requires clear budgeting and proactive strategies to minimize financial strain. Start by distinguishing essential living costs from discretionary spending to prioritize loan payments without sacrificing basic needs. Setting up automatic payments can prevent missed due dates and reduce the risk of default.

Utilize loan grace periods or deferment options when possible, but keep in mind that interest often continues to accrue, increasing total repayment. Focus on paying off loans with the highest interest rates first-for example, targeting a 10% interest loan before one at 5% helps lower your overall cost.

Consider employer assistance or income-driven repayment plans if available, as these can reduce monthly payments during financial hardship. Early communication with lenders about any repayment difficulties can open opportunities for flexible arrangements or negotiated terms.

The Federal Reserve's "Economic Well-Being of U.S. Households" report indicates 35% of adults may need to borrow for urgent expenses, underscoring the importance of managing emergency loans wisely. Supplementing income through part-time or freelance work can help maintain steady progress toward repayment.

Regularly review your repayment plan to adjust for income changes or unexpected costs. Staying informed about your loan terms and adopting structured repayment approaches greatly lowers the risk of default and long-term financial challenges.

Other Things You Should Know About

Yes, emergency student loans can typically be used to cover a range of urgent expenses, including living costs such as rent, utilities, and groceries. However, the exact allowable uses depend on the lender's terms, so students should verify what expenses are covered before borrowing.

Emergency student loans from federal sources are not usually reported to credit bureaus unless the borrower defaults. Private emergency loans, on the other hand, are often reported to credit agencies, which can impact your credit score positively or negatively depending on repayment behavior.

Some private emergency student loans may require a co-signer, especially if the borrower has limited or no credit history. Federal emergency assistance or campus-based loans often do not require co-signers, making them accessible for students without established credit.

Failing to repay an emergency student loan can lead to late fees, increased interest rates, and damage to your credit score. Federal emergency loans may offer deferment or forbearance options in hardship cases, but private lenders generally have fewer protections, so it's important to communicate proactively with the lender if repayment difficulties arise.