2026 Best Student Loans for Past-Due Tuition

Student Finance & Loan Expert

Falling behind on tuition payments can delay graduation and limit access to essential campus resources. Many students face financial setbacks due to unexpected expenses or reduced income. This challenge often complicates continuing education or pursuing advanced degrees. Finding reliable financial solutions is critical to overcoming these obstacles and maintaining academic progress. This article explores top student loan options specifically designed to address past-due tuition balances. It aims to guide readers toward informed borrowing choices that balance affordability and repayment flexibility, enabling a smoother path to degree completion.

- What are the best loan options to cover past-due college tuition balances? Best options

- Can you use new federal student loans to pay off an existing tuition balance? Federal use

- How do private student loans for past-due tuition work and who offers them? Private loans

- What eligibility requirements apply to loans that cover unpaid tuition and fees? Eligibility

- How do interest rates, fees, and borrowing limits differ for past-due tuition loans? Rates & limits

- How do you apply for federal and private loans when your account is on financial hold? Applying on hold

- Which repayment plans are best if you borrowed to clear an overdue tuition bill? Best repayment

- How do deferment, forbearance, and school payment plans compare for past-due balances? Deferment vs plans

- What credit score, co-signer, and documentation do lenders require for delinquent tuition loans? Credit & co-signer

- How do default, collections, and transcript holds affect options to finance past-due tuition? Default impact

What are the best loan options to cover past-due college tuition balances?

Federal Direct PLUS Loans for parents and graduate students are among the best student loans for past-due tuition balances. These loans offer fixed interest rates and permit borrowing up to the total cost of attendance, including overdue fees. Although they require a credit check, they often provide more flexible repayment options compared to private loans.

Private loans can cover gaps not addressed by federal aid, but they typically come with higher interest rates and stricter credit qualifications. It's wise to shop for lenders offering competitive rates, low fees, and borrower protections. Some lenders specifically market tuition consolidation loans designed to clear outstanding tuition balances.

Many colleges offer institutional payment plans or short-term emergency loans that break down past-due amounts into manageable monthly payments, helping students avoid disenrollment and maintain access to transcripts and credits.

When selecting low-interest loan options for overdue college fees, students should weigh key factors:

- Interest rates and fees

- Repayment terms and flexibility

- Credit qualification criteria

- Ability to discharge the loan if unable to complete the program

Addressing unpaid tuition promptly is vital, as it leads to 36% lower reenrollment rates and leaves 6.6 million Americans with stranded credits (Ithaka S+R). Students may also consider broader financial needs by exploring student loans for living expenses alongside tuition assistance to maintain academic progress.

Can you use new federal student loans to pay off an existing tuition balance?

Federal student loans generally cannot be used to pay past-due tuition beyond a very limited amount. They typically restrict funding to the current enrollment period and only allow up to $200 to cover prior-year tuition balances. This restriction, imposed by the U.S. Department of Education, ensures federal aid supports ongoing education rather than clearing existing debts. If you're wondering about federal loan options for covering existing tuition debt, the possibilities are quite limited.

Private student loans, however, may provide more flexibility. Many private lenders allow borrowing to pay off unpaid tuition up to 12 months old, covering the full cost of attendance, including fees and other expenses. For instance, if you owe $3,000 from last semester and missed federal loan eligibility to cover it, a private lender might permit financing this amount alongside your current charges. This can unblock registration or access to academic services when past balances are an obstacle.

Keep in mind private loans generally carry higher interest rates and fewer borrower protections compared to federal loans. It's essential to evaluate loan terms carefully and assess your repayment capacity before borrowing.

Key points to consider:

- Federal loans typically cover only up to $200 of prior-year balances.

- Private lenders may finance balances up to 12 months old and include the full cost of attendance.

- Using private loans for past-due tuition requires careful evaluation of loan terms and repayment ability.

For those exploring flexible borrowing options, reading reviews such as the ascent non cosigned student loans can provide valuable insight. Always check with your school's financial aid office to understand specific policies related to past tuition debts and how they coordinate with various loan options.

How do private student loans for past-due tuition work and who offers them?

Private student loans for past-due tuition explained are personal credit products designed to cover overdue balances owed to educational institutions. These loans, offered by banks, credit unions, or specialized lenders, usually require a credit check and may need a cosigner. Loan funds are paid directly to the school, clearing past-due tuition so students can continue their studies or re-enroll. Interest rates vary and tend to be higher than federal loans, reflecting the borrower's credit profile.

Top lenders offering student loans for overdue tuition include Sallie Mae, Citizens Bank, and SoFi. Each lender provides different terms, repayment options, and benefits, such as deferred payments until after graduation or income-driven repayment plans that can ease monthly expenses.

Credit unions and community banks sometimes offer more flexible criteria, making them viable options for students with urgent past-due balances. Some private lenders market loans specifically as "tuition loans" or "educational loans" targeting arrears resolution.

About 30% of undergraduates at public institutions accumulate institutional debt during college, with nearly half leaving without a degree (Student Borrower Protection Center). Private loans can prevent enrollment holds or collections but have higher costs and fewer protections than federal aid.

Before choosing a private loan for overdue tuition, students should compare lender offers, understand repayment responsibilities, and explore alternatives such as institutional payment plans or emergency grants. It's also valuable to review student loan refinance deals to potentially reduce overall costs.

What eligibility requirements apply to loans that cover unpaid tuition and fees?

Loans that cover unpaid tuition and fees require specific eligibility requirements, which depend on the loan type but typically focus on enrollment status, program type, and creditworthiness. Federal Direct Loans permit borrowing only if students are enrolled at least half-time in a qualifying degree or certificate program. These loans generally do not fund past-due balances unless the school verifies enrollment and eligibility for further aid. Private lenders and institutional loans usually require proof of current enrollment and satisfactory academic progress, though some specialize in refinancing past balances regardless of enrollment, provided borrowers have steady income or co-signers.

Key eligibility criteria for student loans covering unpaid tuition include:

- Enrollment Status: Federal loans require at least half-time enrollment; some private lenders have more flexible conditions or allow refinancing of unpaid tuition for graduates.

- Academic Standing: Maintaining satisfactory progress is essential; students with academic holds might face restrictions.

- Income and Credit History: Federal loans are generally credit-independent except for PLUS loans, which require credit checks; private lenders typically assess creditworthiness closely, sometimes needing co-signers.

- Institution Eligibility: The school must participate in federal student aid programs to enable federal loans to cover past-due tuition.

Requirements to qualify for loans on past-due tuition and fees are vital to address promptly, as adults aged 25-34 with bachelor's degrees earn significantly more than those with only a high school diploma. Loans that allow re-enrollment and degree completion represent crucial investments in career prospects and earnings. For those seeking student loans for RN programs, understanding these criteria can help secure needed funding.

How do interest rates, fees, and borrowing limits differ for past-due tuition loans?

Interest rates on past-due tuition loans vary significantly based on the lender, credit profile, and whether the loan is federal or private. Private undergraduate loans typically have fixed rates ranging from about 4.5% to over 16% APR. Borrowers with strong credit or cosigners often secure rates near 4.5%, while those with weaker credit face higher rates. Fees also differ: federal loans usually avoid origination and late fees but may charge penalties for missed payments. Private lenders frequently include origination fees between 1% and 6%, plus late payment fees that can increase costs.

Borrowing limits depend on the loan type, institution, and student status. Federal loans limit annual borrowing to roughly $5,500-$12,500 for undergraduates. Private loans may allow higher amounts, sometimes covering the full past-due balance, although total debt generally cannot exceed the cost of attendance minus other aid.

When considering options, it helps to compare factors such as interest rates, fees, borrowing limits, and borrower protections. For instance, a borrower with good credit might obtain a private past-due loan near 5% APR with lower fees but face stricter repayment terms. Federal loans offer more protections but lower amounts. These distinctions impact affordability and long-term financial health.

How do you apply for federal and private loans when your account is on financial hold?

When your student account is on financial hold, obtaining federal or private student loans involves specific steps to address outstanding balances. For federal loans, start by contacting your school's financial aid office to discuss the hold. You might need to submit a payment plan or pay part of the past-due tuition before new federal loan disbursements can be approved. Some institutions lift holds temporarily once you provide proof of a loan application.

Private lenders vary in their approach to past-due tuition. For instance, Earnest permits borrowers to use private loans to cover institutional balances up to 365 days past due and up to the full certified cost of attendance under their lending guidelines. This can be essential if your hold is due to overdue charges from the last year.

Effective steps to apply include:

- Confirm your school's policies on financial holds and overdue balances.

- Collect your tuition balance statements and hold details from the bursar or student accounts office.

- Complete the FAFSA and meet any specific school requirements for federal loan disbursement while on hold.

- For private loans, focus on lenders like Earnest who support loans for past-due amounts and provide necessary documentation.

- Submit loan applications with accurate cost of attendance figures to cover current and overdue tuition.

Maintaining open communication with your financial aid office throughout is crucial to avoid delays or denial of funds. Knowing each lender's criteria helps streamline approvals and lift holds faster.

Which repayment plans are best if you borrowed to clear an overdue tuition bill?

Income-driven repayment plans adjust monthly payments according to your income and family size, making them suitable if you borrowed to clear overdue tuition. The Revised Pay As You Earn plan, for example, caps payments at 10% of discretionary income, reducing financial pressure early in your career.

Federal consolidation loans allow combining multiple federal loans into one, extending the repayment period to lower monthly payments. This helps improve cash flow but may increase total interest paid.

Private loan borrowers often benefit from fixed repayment plans that offer predictable monthly payments, aiding budgeting. Since over 90% of new private undergraduate loans require a cosigner (MeasureOne Private Student Loan Report, 2024), borrowers with cosigners typically receive better rates and repayment terms. For those without a cosigner, flexible plans with deferment or forbearance options are important.

Graduated repayment plans start with lower payments that increase every two years, fitting borrowers expecting income growth through raises or promotions. However, they carry risks if income stagnates.

Selecting the right plan depends on your financial situation, credit status, and expected income growth. Carefully weigh plans that balance affordability now with minimizing long-term debt impact to best manage your student loans.

How do deferment, forbearance, and school payment plans compare for past-due balances?

Deferment, forbearance, and school payment plans provide different ways to handle overdue tuition balances, each affecting student finances uniquely. Deferment pauses loan payments temporarily and often stops interest accumulation on federally subsidized loans. Examples include unemployment or economic hardship deferments, which give students relief without increasing debt. However, unsubsidized loans generally continue to accrue interest during deferment, raising the total owed.

Forbearance also suspends or lowers payments but usually results in interest compounding on all loan types, including federal and private loans. It tends to be more expensive over time and is best used for short-term financial issues when deferment is unavailable, like a brief job loss.

School payment plans let students split past-due tuition into manageable monthly payments directly with their school. These plans typically avoid credit checks and interest but may include administrative fees. They help maintain enrollment and prevent loan default but require careful budgeting to avoid extra penalties.

Non-loan alternatives like grants and emergency aid are vital. The National Association of Student Financial Aid Administrators reports that 71% of public four-year schools offer emergency or completion grants for unforeseen or overdue expenses. Utilizing these funds can reduce reliance on additional loan debt.

Students should first assess their eligibility for deferment, then consider forbearance if needed, while also exploring school payment plans and emergency aid as supplementary options to lessen financial strain.

What credit score, co-signer, and documentation do lenders require for delinquent tuition loans?

Lenders typically require a minimum credit score of around 620 to approve loans for delinquent tuition, though applicants with lower scores may succeed if supported by a co-signer. Co-signers usually need credit scores above 700 and stable income to improve loan approval odds, helping to offset the lender's risk.

Essential documentation includes proof of outstanding tuition-like billing statements or collection notices-and income verification through recent pay stubs or tax returns. Some lenders also request enrollment verification from the school to confirm the student's status. Providing complete documentation is crucial for accurate underwriting, especially when dealing with past-due balances.

Co-signers must often submit identification, proof of residence, and credit authorization. Borrowers with poor credit or prior collections may face requirements for higher down payments or additional collateral. These measures protect lenders and may increase loan approval chances.

Failing to resolve past-due tuition debts can lead to serious consequences. Roughly one-third of institutional debts are sent to collections, remaining on credit reports for up to seven years and significantly harming credit scores. Meeting lender documentation requirements and using co-signers when needed can improve terms and approval rates.

How do default, collections, and transcript holds affect options to finance past-due tuition?

Defaulted student loans, collections, and transcript holds create significant obstacles when trying to finance past-due tuition. Students with previous loan defaults often become ineligible for federal aid programs such as Direct Loans or PLUS Loans. Private lenders typically view defaulted borrowers as high risk, which can lead to higher interest rates or outright loan denials.

Collections on credit reports further damage borrowing prospects by signaling missed payments that can linger for up to seven years. This reduces creditworthiness and increases loan costs. Transcript holds add another layer of difficulty by blocking class registration and withholding official transcripts until balances are cleared, forcing many students to rely on private loans or alternative payment arrangements.

To manage these barriers, consider:

- Negotiating loan rehabilitation or consolidation with servicers to regain federal loan eligibility.

- Requesting payment plans from your institution to remove transcript holds without adding new debt.

- Exploring private loans with a cosigner to improve approval chances and terms.

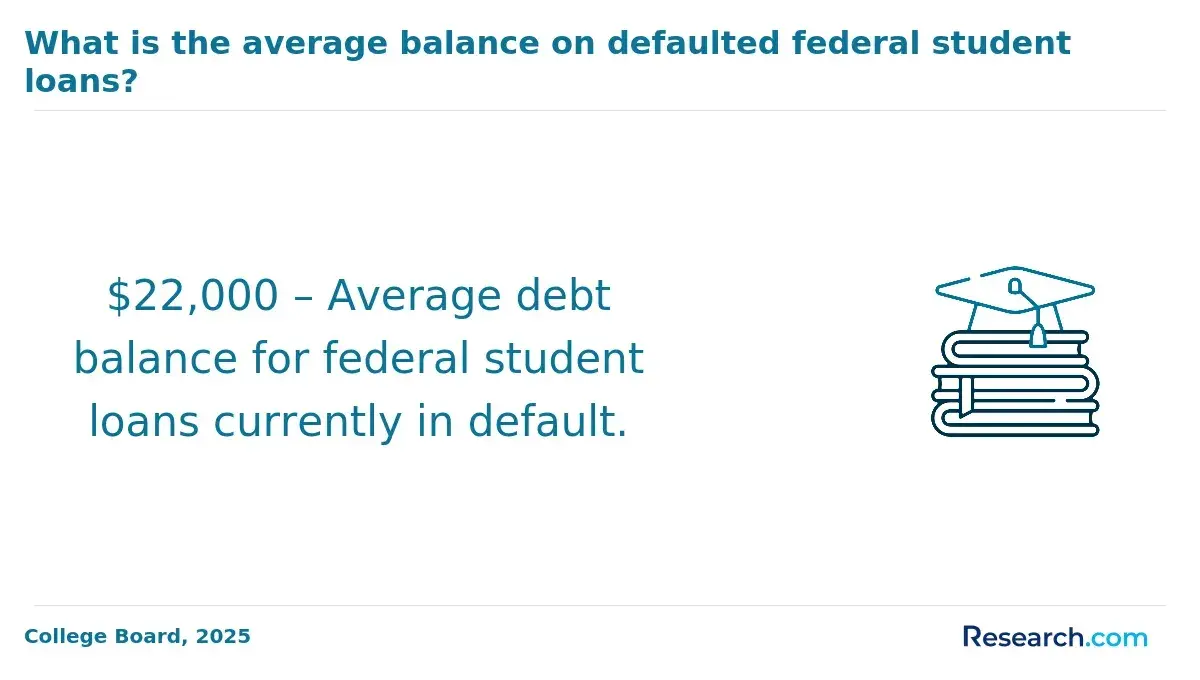

Among borrowers aged 25-34, the average outstanding student loan debt is around $33,200, with 16% experiencing delinquency or default (Federal Reserve). Developing a clear repayment strategy is essential before seeking new loans for overdue tuition, as unresolved defaults or collections will worsen financial challenges and limit access to affordable federal funding.

Other Things You Should Know About

Yes, unpaid tuition balances that go into collections can negatively impact your credit score. Once a school or collection agency reports the delinquency to credit bureaus, it may remain on your credit report for up to seven years, making it harder to secure loans or favorable interest rates in the future.

Generally, student loans used to cover past-due tuition are not considered taxable income and do not create immediate tax liabilities. However, it is important to note that any loan forgiveness or cancellation in the future could potentially have tax consequences depending on current tax laws.

Many schools offer payment plans or financial counseling that may help reduce or delay the amount owed on past-due tuition. Negotiating directly with your school before securing a loan can sometimes result in lower fees, waived penalties, or extended deadlines, making loans less necessary or smaller in amount.

Failing to repay a loan used for past-due tuition can lead to default, which severely impacts your credit score and may result in wage garnishment or tax refund withholding. It can also limit your ability to borrow money in the future, so it is crucial to explore repayment options and communicate with lenders early if you encounter difficulties.