2026 Best Student Loan Lenders for Graduate Students

Student Finance & Loan Expert

Securing funding for graduate studies often challenges those switching fields or returning to school after work experience. Traditional lenders may impose strict credit requirements or offer limited flexibility, complicating access to needed funds.

Additionally, navigating varying interest rates and repayment options can overwhelm prospective students. This situation demands clear, reliable guidance to identify lenders that accommodate diverse financial backgrounds while supporting advanced education.

This article examines top student loan lenders known for favorable terms, accessibility, and support for graduate students, helping readers make informed borrowing decisions that align with their academic and career goals.

- What are the best student loan lenders for graduate students? Best Lenders

- How do federal and private graduate student loans compare? Federal vs Private

- How do you qualify for graduate student loans? Eligibility

- How does FAFSA affect graduate student loan options? FAFSA

- What interest rates and borrowing limits apply to graduate loans? Rates and Limits

- Which repayment plans work best for graduate borrowers? Repayment Plans

- What forgiveness programs can graduate student borrowers use? Forgiveness

- When should you refinance or consolidate graduate student loans? Refinance or Consolidate

- What happens if you defer or forbear graduate student loans? Deferment Options

- How can you choose the right graduate student loan? Choose Loan

What are the best student loan lenders for graduate students?

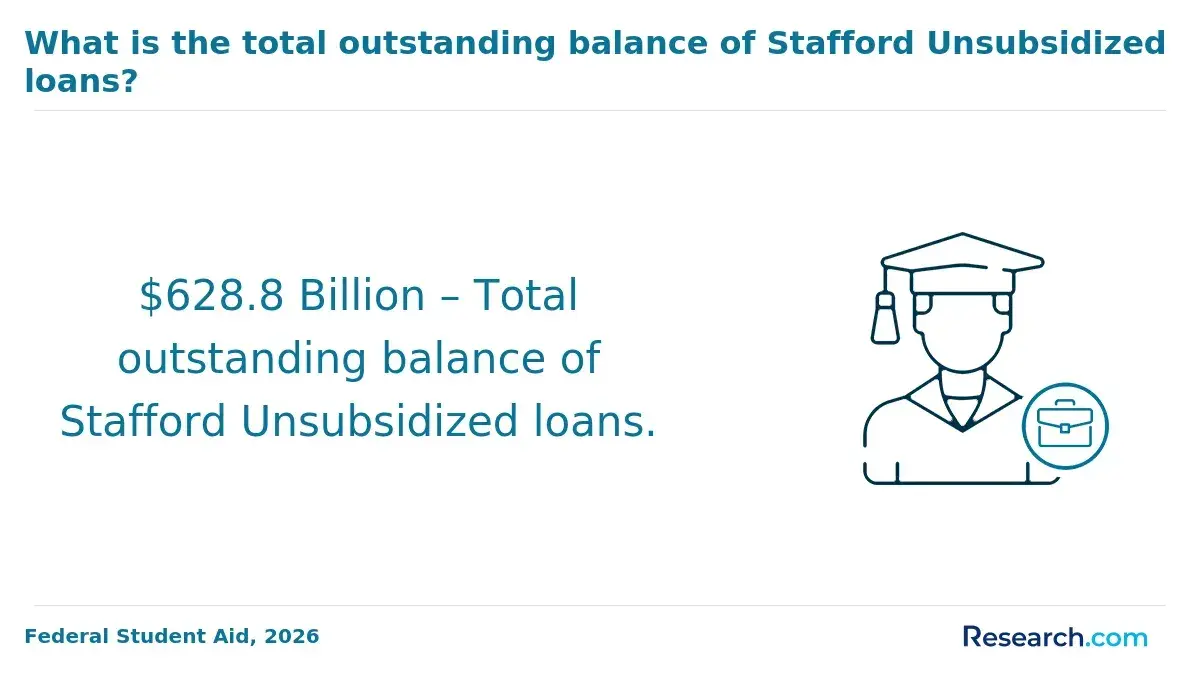

Federal Direct Unsubsidized Loans and Grad PLUS Loans are the leading options for graduate students, offering fixed interest rates and income-driven repayment plans with borrower protections such as Public Service Loan Forgiveness. These federal loans cover most graduate student needs and are crucial since graduate students hold a significant portion of federal student loan debt.

For those who need additional funds or have reached federal loan limits, private lenders like Sallie Mae, Citizens Bank, and SoFi provide competitive fixed and variable rates.

These top private student loan providers for graduate programs often require good credit or a cosigner and may include benefits like interest rate reductions for autopay or career-related perks. However, private loans lack many federal borrower protections such as loan forgiveness or deferment.

When choosing the best student loan lenders for graduate students, consider:

- Interest Rates: Federal loans generally have lower rates that adjust annually; private rates vary with creditworthiness.

- Repayment Plans: Federal options include income-driven plans; private lenders usually do not.

- Loan Limits: Federal loans have annual and total borrowing caps; private loans can fill remaining costs without strict limits.

- Borrower Protections: Mostly available with federal loans.

- Application Requirements: Private lenders often require credit checks or cosigners.

Graduate students may also explore options to use student loans for off-campus rent when budgeting for living expenses. It is important to evaluate all factors carefully to make informed borrowing decisions.

How do federal and private graduate student loans compare?

Federal and private graduate student loans differ notably in interest rates, borrower protections, and eligibility requirements.

For graduate borrowers, the average interest rate for new federal Direct Unsubsidized Loans is 8.08%, while private student loans often offer fixed rates between 6% and 7%, depending on creditworthiness and lender criteria. These differences play a crucial role when comparing federal vs private graduate student loan options.

Federal loans come with fixed rates and flexible repayment plans, including income-driven options and loan forgiveness programs, which can be critical for those pursuing public service or facing unpredictable income. Private loans, on the other hand, typically lack these borrower protections and deferment options and often demand cosigners and stronger credit qualifications.

Graduate students exploring the differences between federal and private student loans for graduates should carefully assess credit profiles and career plans. Private lenders may provide lower rates or higher borrowing amounts, but the associated risks include variable or promotional rates that can increase with financial hardship.

Those with less-than-perfect credit seeking alternatives can review bad credit student loans for additional options. It is essential to compare multiple private lender offers alongside official federal loan terms to make an informed decision.

How do you qualify for graduate student loans?

Qualifying for graduate student loans in the United States requires meeting eligibility criteria established by federal and private lenders. Federal Graduate PLUS loans and Direct Unsubsidized Loans are available to students who maintain at least half-time enrollment in an eligible graduate program and have a valid FAFSA on file.

While a credit check is only required for Graduate PLUS loans, poor credit may lead to denial or the need for a cosigner.

Private lenders set varied credit standards, often requiring proof of enrollment, a strong credit score, steady income, and sometimes a cosigner. Terms and interest rates differ among private loans, making it important to compare offers carefully before deciding.

Recent financial data shows that from 2022 to 2024, average federal interest rates on new graduate loans increased by over 3 percentage points. This rise has led to an estimated 20-25% increase in total repayment costs over a typical 10-year term, according to Federal Student Aid and Congressional Research Service data. Students should consider this when evaluating loan options and repayment strategies.

Key steps to ensure approval include:

- Submitting the FAFSA annually to access federal loans.

- Maintaining half-time enrollment.

- Meeting credit requirements or securing a cosigner for private loans.

- Comparing loan terms and interest rates before accepting an offer.

Knowing how to qualify for graduate student loans in the United States and understanding the eligibility requirements for graduate student loan approval can improve chances of acceptance.

For those seeking guidance on selecting the best financing options, consulting resources about MBA student loans can be helpful in making informed decisions.

How does FAFSA affect graduate student loan options?

FAFSA directly influences eligibility for federal student loans, providing the most affordable and flexible borrowing options for graduate students. Completing the FAFSA is essential to access federal loans like Direct Unsubsidized Loans and Grad PLUS Loans.

Without submitting FAFSA, students miss out on these federal funds and face reliance on more costly private loans.

Federal loan borrowing limits for graduate students are higher than for undergraduates but are capped yearly. For example, Direct Unsubsidized Loans allow up to $20,500 per academic year, and Grad PLUS Loans can cover the remaining cost of attendance, pending credit approval.

This system relies on FAFSA data to verify financial need and loan eligibility, demonstrating how how fafsa eligibility impacts graduate student loans.

Federal loan repayment plans and forgiveness programs require federally sourced loans, which underscores FAFSA's significance. Students skipping FAFSA lose access to Income-Driven Repayment plans that adjust payments based on income, reducing financial strain.

Median federal debt among graduate degree completers reached approximately $71,000, with higher debt levels common. Additionally, FAFSA benefits for graduate loan options extend to eligibility for need-based aid or institutional grants that can lower overall borrowing.

Prospective borrowers should complete FAFSA early to maximize funding opportunities and understand federal loan options clearly before pursuing private financing, including from student loan banks.

What interest rates and borrowing limits apply to graduate loans?

Federal unsubsidized Direct Loans for graduate students generally have interest rates between 5% and 7%. Private lenders offer a wider range, typically from 4% up to 14%, based on creditworthiness and market conditions. Both fixed and variable rates are available-fixed rates offer stability, while variable rates might start lower but carry more risk.

Annual federal borrowing limits for graduate students cap at $20,500 for unsubsidized Direct Loans. The total federal loan limit, including undergraduate debt, reaches $138,500. Professional degree students may access Grad PLUS loans, which can cover the full cost of attendance minus other aid, subject to credit approval and without a fixed cap.

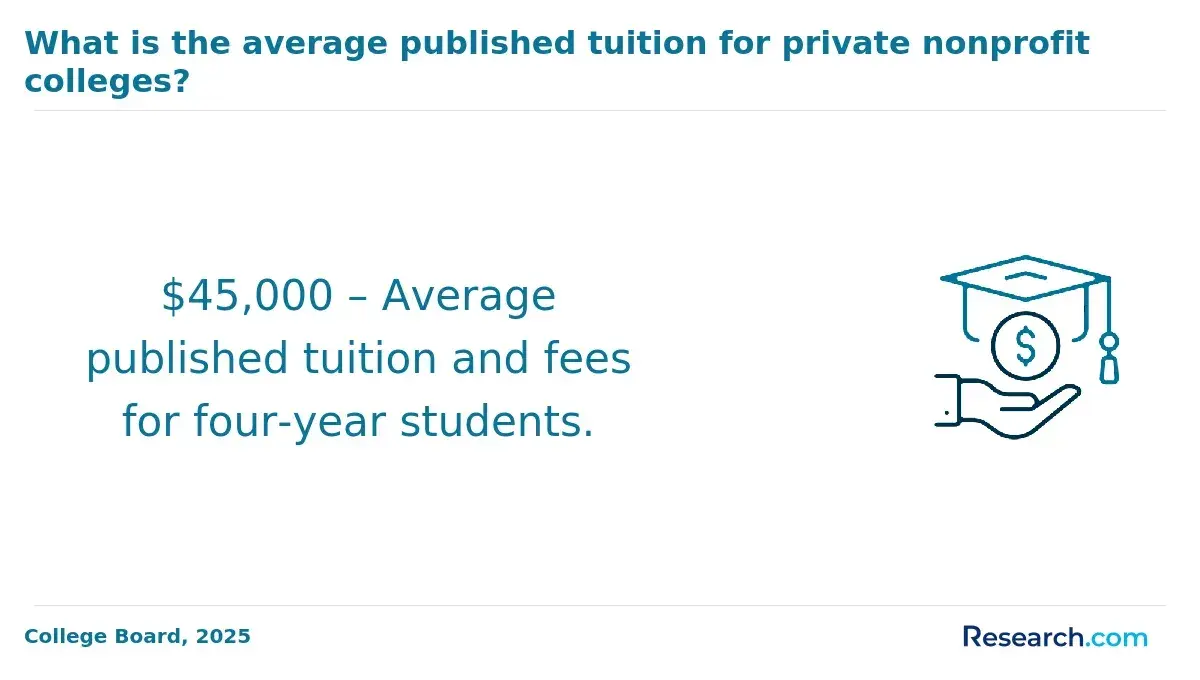

Private loans do not have standardized limits and often cover the entire cost of attendance, which varies widely. Private nonprofit graduate tuition averaged $32,170 per year, more than double the $13,790 charged by public institutions. This substantial gap often increases loan reliance despite grants or savings.

Key considerations for graduate borrowers:

- Federal loans usually offer lower interest rates and flexible repayment options.

- Private loans require careful review of rates, fees, and protections.

- Loan consolidation might simplify payments but won't reduce interest rates.

Which repayment plans work best for graduate borrowers?

Income-Driven Repayment (IDR) plans offer significant benefits for graduate borrowers managing substantial student debt while expecting increased earnings. Options like Revised Pay As You Earn (REPAYE) limit monthly payments to 10-15% of discretionary income, providing early-career flexibility and supporting financial stability.

For graduates with professional degrees and median salaries near $127,000, standard or graduated repayment plans may be preferable. These plans allow faster loan payoff over 10 years with lower total interest, pairing well with steady, higher incomes.

Refinancing private loans is another option for those with strong credit and reliable income but may result in losing federal loan protections, so this choice requires careful consideration.

Key factors in choosing a repayment plan include:

- Monthly payments relative to discretionary income.

- Eligibility for loan forgiveness through public service or other programs.

- The balance between loan term length and total interest costs.

- Alignment of payment schedules with expected income growth.

Workers with master's degrees earn roughly 21% more than those with just a bachelor's, making manageable monthly payments vital. REPAYE and similar IDR plans help maintain financial balance without excessive payment burdens early in a graduate's career.

What forgiveness programs can graduate student borrowers use?

Graduate student borrowers have access to several federal loan forgiveness programs aimed at reducing debt after years of qualifying service or employment in certain fields.

The Public Service Loan Forgiveness (PSLF) program stands out by forgiving remaining balances after 120 qualifying payments while employed full-time by government or nonprofit organizations. Income-Driven Repayment (IDR) plans such as REPAYE, PAYE, and IBR offer forgiveness on leftover debt following 20 to 25 years of qualifying payments.

Teacher Loan Forgiveness benefits graduates who teach full-time in low-income schools for five consecutive years, potentially forgiving up to $17,500. Other professions, including nurses and physicians working in underserved areas, may qualify for state-specific or occupation-based forgiveness programs.

Private student loans typically do not provide forgiveness options. Nearly 90% of approved private undergraduate and graduate loans in 2025 required a creditworthy cosigner, and applicants with FICO scores below 700 faced higher rejection or APR rates, according to Sallie Mae's How America Pays for College 2025. Therefore, federal and public loans remain the main pathways for forgiveness benefits.

Borrowers should carefully track qualifying payments and verify employment eligibility under each program, as using incorrect repayment plans or employer types can delay or disqualify forgiveness. Exploring state or employer-based options is also important, since criteria and availability vary significantly.

When should you refinance or consolidate graduate student loans?

Refinancing or consolidating graduate student loans can be a strategic move to lower interest rates or combine multiple payments into a single loan. Borrowers with high-interest private loans often reduce their overall costs and monthly bills through refinancing.

Consolidation suits those holding several federal loans with varying terms who prefer one payment without altering original interest rates. Note that federal consolidation might eliminate certain borrower protections, so weigh the pros and cons carefully.

Graduate borrowers with stable incomes may choose refinancing to shorten repayment terms, thereby decreasing total interest costs. Meanwhile, those experiencing financial difficulties might consolidate into an income-driven repayment plan, which can lower monthly payments based on income, a benefit federal consolidation provides.

Data shows graduate borrowers have a relatively low default rate-about 7% within three years of repayment-compared to nearly 22% for certificate or associate degree holders. Despite this, managing multiple loans or facing high rates calls for evaluating refinancing or consolidating options promptly to improve financial health.

Key considerations when deciding include:

- Comparing interest rates and fees to ensure refinancing or consolidation leads to real savings.

- Considering the potential loss of federal benefits like loan forgiveness or flexible repayment options.

- Assessing your current and future income to select the best repayment approach.

What happens if you defer or forbear graduate student loans?

Deferment or forbearance temporarily pauses or reduces your graduate student loan payments but does not stop interest from accumulating. Some federal loans, like Direct Subsidized Loans, may have subsidized interest during deferment, but most graduate loans, including unsubsidized federal and private loans, continue to accrue interest, which capitalizes when you resume payments.

This capitalization raises your total debt and can increase monthly payments later. For example, deferring a $50,000 unsubsidized loan at 6% interest for one year could add about $3,000 in interest to your principal once repayment restarts.

Forbearance functions similarly but is often granted during temporary financial hardship without strict eligibility requirements, though interest still accumulates and capitalizes on all loans during this time.

Use deferment or forbearance cautiously, as prolonged periods can significantly increase your debt over time. Consider refinancing options to manage payments more effectively.

Borrowers with excellent credit can reduce interest rates from approximately 7.9% to 5.1%, potentially saving $10,000-$15,000 in interest over 10 years on a $100,000 balance, according to a credible refinancing marketplace report.

When choosing deferment or forbearance, confirm the interest impact and terms with your lender. Federal income-driven repayment plans may be better alternatives, lowering payments without interest capitalization, helping control long-term costs more effectively.

How can you choose the right graduate student loan?

Federal borrowing limits for graduate student loans will change starting July 1, 2026. Most graduate borrowers will be capped at $20,500 per year, with a lifetime Direct Unsubsidized Loan limit of $100,000. This adjustment reduces available federal amounts by up to $65,500 compared to previous Grad PLUS loan limits, based on data from Finaid.org and the U.S. Department of Education.

Interest rates vary between federal and private loans. Federal options generally offer fixed, often lower rates, and include flexible repayment plans like income-driven repayment or deferment. These options can support borrowers during early career stages or periods of unemployment.

Loan fees and penalties also differ. Federal loans typically have no prepayment penalties, while private lenders may charge origination fees or penalties that impact total loan cost.

Credit requirements are a key distinction. Federal student loans do not require a credit check, whereas private loans often do, possibly requiring a co-signer which may affect eligibility.

Students should assess their actual borrowing needs carefully within the $20,500 annual federal limit. Many graduate programs exceed this amount, making private loans a necessary supplement. Borrow only what is needed to cover education and living costs to avoid excessive debt.

Other Things You Should Know About

Yes, graduate student loans can cover living expenses such as rent, food, and transportation. Both federal and private loans allow you to borrow funds beyond tuition costs to help manage your overall budget while in school. It is important to borrow only what you need to avoid excessive debt.

Graduate student loan interest may be tax-deductible up to $2,500 annually, depending on your income level and filing status. This deduction can reduce your taxable income but does not require you to itemize deductions. Check the latest IRS rules to confirm your eligibility.

If a graduate student loan goes into default, the borrower faces severe consequences including damage to credit scores, wage garnishment, and loss of eligibility for additional federal aid. Defaulted loans may also incur additional fees and legal action, making it crucial to stay current on payments or seek alternative arrangements.

Graduate students may qualify for deferment or forbearance under certain conditions such as ongoing enrollment, economic hardship, or unemployment. These options temporarily pause or reduce loan payments but may result in accrued interest, increasing the total repayment amount over time.