2026 Can You Get Student Loans After the FAFSA Deadline?

Student Finance & Loan Expert

Many prospective graduate students discover the FAFSA deadline has passed after they planned to apply for financial aid. Missing this key date can create uncertainty about securing student loans needed to fund advanced degrees. Without timely FAFSA submission, some federal aid options become unavailable, complicating budget planning. However, alternative strategies may still provide access to necessary financing despite the missed deadline. This article explores available student loan options after the FAFSA deadline and guides readers on navigating financial pathways to support graduate studies effectively.

- Can you still get student loans if you miss the FAFSA deadline? Can you still get

- What are the differences between federal and private loans when applying late? What are the differences

- How do school, state, and federal FAFSA deadlines affect your loan options? How do school, state,

- What last-minute steps should you take if you missed your school's priority deadline? What last-minute steps should

- Can you apply for federal Direct Loans after the academic year begins? Can you apply for

- How do private student loans work if you need funding after FAFSA closes? How do private student

- Are there emergency, payment-plan, or short-term options if loans aren't available? Are there emergency, payment-plan,

- How do borrowing limits and cost of attendance rules apply to late loan requests? How do borrowing limits

- What are the risks of relying on private loans instead of late federal aid? What are the risks

- How can you plan ahead to avoid missing future FAFSA and aid deadlines? How can you plan

Can you still get student loans if you miss the FAFSA deadline?

You can still apply for student loans after FAFSA deadline, but your options are limited and timing is important. Many schools accept late FAFSA submissions for federal direct loans and some institution-specific aid, though this varies by school and state. Contacting your financial aid office promptly is crucial to understand your options. Missing the FAFSA deadline often means losing eligibility for federal grants like Pell Grants. For instance, over $4.0 billion in unclaimed federal Pell Grants was reported due to late FAFSA filing.

Direct federal loans, including subsidized and unsubsidized Stafford loans, may remain available if your FAFSA is processed before or shortly after the academic year begins. However, applying late might reduce your loan amount or delay disbursement. Options for student loans if you missed FAFSA deadline include private student loans, which don't require FAFSA but usually have higher interest rates and depend heavily on creditworthiness.

Consider these steps if you miss FAFSA deadlines:

- Check your school's financial aid deadline extensions.

- Submit FAFSA as soon as possible to maximize remaining aid.

- Talk to your financial aid office about emergency or institutional aid.

- Explore private loans only after using federal aid options.

Late FAFSA filing can reduce your aid but doesn't close all doors. For questions about funding specific needs, explore whether can you use student loans to pay for rent may apply in your situation.

What are the differences between federal and private loans when applying late?

Federal student loans have strict FAFSA deadlines tied to state and college requirements, and missing these deadlines often results in losing eligibility for specific federal grants and subsidized loans. Funding is limited and distributed on a first-come, first-served basis. Data from Trends in Student Aid and Bankrate FAFSA statistics 2025 show that undergraduate and graduate students received $256.7 billion in total student aid during 2023-24, highlighting the competitive nature of this limited pool. Once the FAFSA deadline passes, accessing these federal funds usually isn't possible until the next cycle.

Applying late for federal and private student loans reveals a key difference: private loans do not require FAFSA completion or federal deadline adherence. Lenders approve private loans year-round based on creditworthiness, income, and other financial factors. This flexibility benefits students who missed FAFSA deadlines by providing alternative funding, often with quicker processing.

However, private loans often carry higher interest rates and fewer borrower protections than federal loans. Federal loans include benefits like income-driven repayment plans, deferment options, and forgiveness programs-features rarely available with private loans. Therefore, federal student loans versus private loans after FAFSA deadline involves weighing need-based aid against loan terms and risks.

Students applying late should:

- Check state and school-specific FAFSA deadlines early to avoid lost federal aid.

- Use private loans as a backup if federal aid is inaccessible but compare costs carefully.

- Apply to multiple private lenders to find the best interest rates and terms.

- Fully understand private loan terms, including repayment obligations and protections.

For those seeking alternative options, exploring student loans for bad credit borrowers may provide solutions tailored to credit challenges.

How do school, state, and federal FAFSA deadlines affect your loan options?

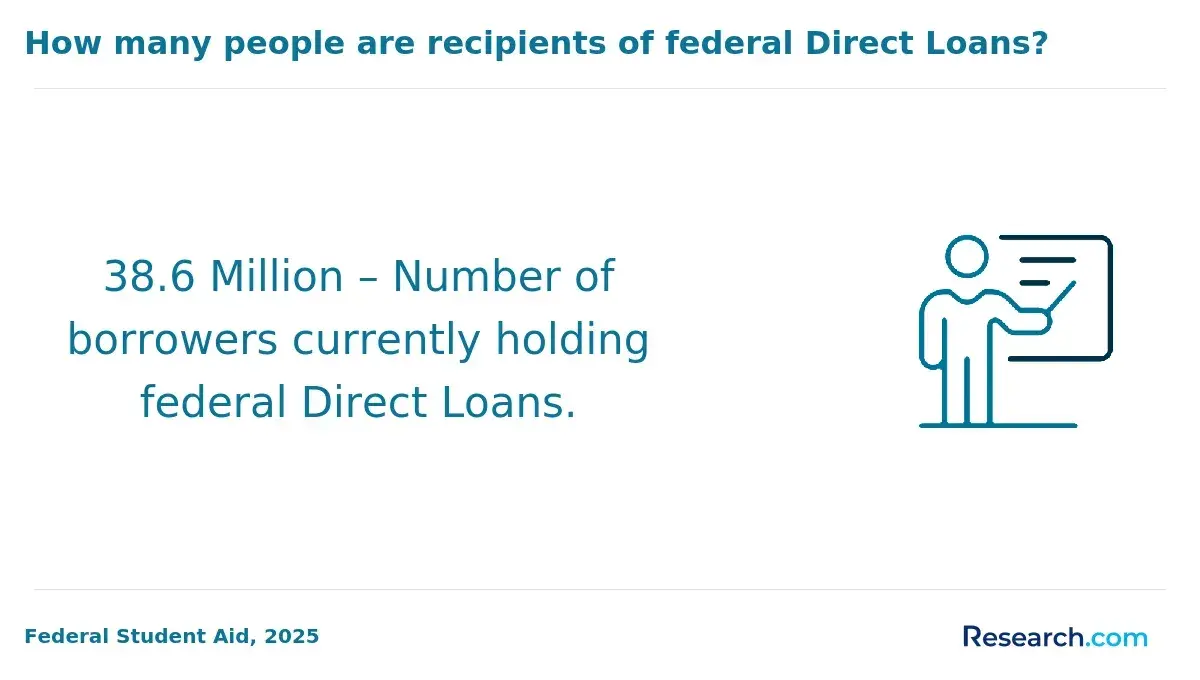

FAFSA deadlines at the federal, state, and school levels play a crucial role in determining eligibility for student loans and other aid. Missing the federal deadline generally results in losing access to federal Direct Loans, including subsidized and unsubsidized Stafford Loans for that academic year. According to Education Data Initiative, $93.1 billion in new federal Direct Loans will be disbursed in 2025, highlighting the importance of timely FAFSA submission.

The impact of school FAFSA deadlines on federal and state loan options can be significant. Many schools require FAFSA early to coordinate institutional aid with federal loans. Missing these deadlines can delay or reduce financial aid, even if the federal deadline is met. Meanwhile, state deadlines vary widely and affect eligibility for state-specific grants and loan programs, with some states setting deadlines as early as March and others using rolling deadlines throughout the year.

If all deadlines are missed, federal loan options disappear, but private loans remain available. These usually carry higher interest rates and fewer protections. Contact your school's financial aid office immediately to explore late FAFSA filing or emergency aid programs.

To maximize your aid opportunities, consider exploring scholarships for returning students, which often have different timelines and criteria. For more information, see scholarships for returning students.

Overall, understanding how federal and state FAFSA deadlines influence student loan eligibility can help you navigate the complex financial aid landscape effectively.

What last-minute steps should you take if you missed your school's priority deadline?

If you missed your school's priority FAFSA deadline, act quickly to maximize financial aid opportunities. Submit your FAFSA as soon as possible because while priority deadlines increase chances for aid, some schools accept late applications and award funds on a rolling basis. For students wondering how to apply for student aid late, contacting your financial aid office is essential. They can guide you on late FAFSA submissions, appeal processes, and alternative institutional aid options like grants or emergency loans.

Many states offer separate aid programs and scholarships that do not rely strictly on FAFSA deadlines, providing additional financial support. Consider federal student loans independently from FAFSA deadlines since Direct Loan applications can sometimes be processed after priority dates if loan counseling and master promissory notes are completed promptly.

Private student loans remain an option but require thorough comparison due to different terms and interest rates. Use them cautiously to fill remaining gaps after exhausting federal aid. For insights into managing those loans, explore how does student loan refinancing work.

Keep documentation ready to support appeals or late applications, including missed deadline explanations and updated financial details. Persistence and prompt communication improve chances of securing aid despite delays.

Federal Student Aid data show 17.045 million FAFSA applications were submitted in 2022-23, covering only 61.10% of fall enrollees (Education Data Initiative, Financial Aid Statistics 2025). This demonstrates opportunities remain for those who file late or seek alternative aid sources, emphasizing the importance of exploring all options for student loans after FAFSA deadline.

Can you apply for federal Direct Loans after the academic year begins?

Federal Direct Loans can still be applied for after the academic year starts, provided you have submitted a FAFSA for that year. Without a completed FAFSA, you won't be eligible for federal student loans during the academic period.

Once your FAFSA is on file, your school may offer Direct Loans at any point throughout the year. Keep in mind that disbursement schedules differ by institution and loan type, and some schools may restrict late loans due to budgeting or enrollment verification deadlines.

Applying late often means missing out on earlier financial aid offers, which can increase personal expenses. According to Bankrate, undergraduates received an average of $16,360 in total financial aid, including $11,610 in grant money. Missing FAFSA deadlines can force students to replace free grant aid with higher-cost loans or personal funds.

Students who file FAFSA late may only qualify for unsubsidized loans or limited aid, while programs like Direct PLUS Loans typically require earlier FAFSA approval and credit checks.

- Submit your FAFSA as soon as possible, even if overdue.

- Contact your financial aid office promptly about loan application steps.

- Know your school's policies on late loan disbursements.

- Explore alternative funding if federal loans are restricted.

How do private student loans work if you need funding after FAFSA closes?

Private student loans remain an option after the FAFSA deadline closes, offering funding when federal aid is no longer accessible. These loans are provided by banks, credit unions, and online lenders, with approval based mainly on creditworthiness, income, and sometimes requiring a co-signer. Since applications can be submitted year-round, students who miss FAFSA deadlines still have the chance to secure money for upcoming terms.

Compared to federal loans, private loans often carry higher interest rates and less flexible repayment options. Borrowers should carefully review loan terms, including whether rates are fixed or variable, repayment timeframes, and any borrower protections. Some lenders allow deferring payments until after graduation, but these options differ greatly. Consulting your school's financial aid office can help identify preferred private lenders with competitive terms.

Over $4 billion in federal grants went unclaimed, according to the Education Data Initiative, mainly due to missed priority deadlines. This highlights why applying for federal aid early is critical to maximize affordable funding.

If federal aid is unavailable post-FAFSA, consider the following:

- Research private lenders thoroughly for interest rates, fees, and repayment flexibility.

- Prepare documentation of income, credit history, and enrollment status before applying.

- Consider co-signers to improve approval chances and terms.

- Explore institutional aid or scholarships still available after FAFSA deadlines.

- Contact your financial aid office for guidance on supplemental private funding.

Are there emergency, payment-plan, or short-term options if loans aren't available?

Students who miss the FAFSA deadline still have options to manage college expenses through emergency grants, short-term loans, and payment plans. Many colleges offer interest-free emergency funds to cover immediate costs such as tuition deposits or housing fees, typically requiring repayment within one semester.

Paying tuition in installments is another viable approach. Schools often provide monthly or quarterly payment plans that help spread out the balance into smaller amounts. Early enrollment in these plans prevents late fees and issues like registration or transcript holds.

Private student loans become a fallback when federal aid isn't accessible. Data from College Board shows a rise in private borrowing alongside federal and nonfederal loans, highlighting families turning to private lenders after FAFSA deadlines. These loans usually need credit approval and may have higher interest rates.

Additional support can come from some states and private organizations offering emergency loan programs or bridge funding to help students caught between financial aid cycles. To find the best solution, contacting your school's financial aid office promptly is essential-they can guide you through available grants, loans, and payment options to avoid financial penalties and ensure continued enrollment.

How do borrowing limits and cost of attendance rules apply to late loan requests?

Federal student loan borrowing limits depend on your cost of attendance (COA) and enrollment status. Even if you apply after the FAFSA deadline, you cannot borrow more than the COA minus any other financial aid you receive. For example, with a COA of $25,000 and $15,000 in other aid, your maximum loan eligibility is $10,000.

Late loan applicants often receive less aid because many programs give priority to on-time FAFSA submissions. The Department of Education also caps annual loan amounts as follows:

- $5,500 for first-year undergraduates

- $6,500 for second-year undergraduates

- $7,500 for third-year and beyond undergraduates

- $20,500 for graduate students for unsubsidized loans

Submitting all required documents quickly after the deadline improves your chances of securing any leftover loan funds, which schools distribute on a first-come, first-served basis.

Federal Work-Study and tax benefits contributed to the $256.7 billion in student aid awarded, but these programs usually require timely FAFSA filing, limiting late applicants' access to full aid packages.

If federal loan limits and deadlines restrict your funding options, consider alternatives such as institutional payment plans or private loans. Contact your financial aid office to explore all available possibilities.

What are the risks of relying on private loans instead of late federal aid? - Private Loan Risks

Private loans pose significant financial risks compared to federal aid, often carrying higher interest rates that increase the total borrowing cost. Unlike federal loans, private lenders rarely provide income-driven repayment plans or forgiveness programs, limiting your ability to manage repayment difficulties. Additionally, private loans usually require credit checks and a co-signer, which can be a barrier for many students.

Federal aid typically offers lower, fixed interest rates and flexible repayment options designed to support borrowers facing financial challenges. These include deferment and forbearance options, which help avoid default during hardship periods. Private loans tend to lack such protections, raising the chance of long-term financial damage.

The impact is notable: data from NCES and Fast Facts: Student Debt shows that bachelor's degree recipients with federal loans had average debts around $45,300 by 2020. Delaying or missing federal aid may force students to rely more heavily on private funding, increasing overall debt and monthly payments.

Students should compare private loan terms carefully with federal aid, focusing on interest rates, repayment flexibility, and borrower protections. If federal aid isn't available, exploring scholarships, grants, or school payment plans can reduce dependence on expensive private loans.

How can you plan ahead to avoid missing future FAFSA and aid deadlines?

Mark all FAFSA and aid deadlines on a digital calendar as soon as each cycle opens, setting multiple reminders-one well ahead and another the day before submission. Federal Student Aid advises applying early starting October 1 for the upcoming academic year. Keep track of deadlines from states, colleges, and private sources, which often differ from the federal deadline. Many schools provide financial aid portals to send personalized alerts.

Prepare a checklist with essential documents like tax returns, Social Security numbers, and income details before you begin. Applying early increases chances of qualifying for limited funds. Trusted advisors or high school counselors can offer valuable guidance, especially for first-generation college students, who make up 47% of FAFSA filers and face higher risks of missing deadlines (Bankrate, FAFSA Statistics 2025).

Staying organized and proactive helps maintain eligibility for student loans and grants without last-minute stress or missed opportunities.

Other Things You Should Know About

Applying for most federal student loans requires submitting a FAFSA form, as it determines eligibility and loan amounts. However, some private lenders offer educational loans without FAFSA, but these typically depend on creditworthiness and a cosigner. Without FAFSA, access to federal aid programs is generally unavailable.

If you submit the FAFSA after your school's final deadline, you may miss out on some institutional or state aid that has limited funding. Federal aid applications remain accepted, but your school's authority to distribute financial aid funds based on your FAFSA may be restricted. Always confirm deadlines with your financial aid office.

Applying late for student loans can reduce the total aid you receive because some grants and scholarships have limited funds and are awarded early. Additionally, late applications may delay disbursement of loan funds, potentially affecting your ability to pay tuition on time. Planning ahead ensures full access to available aid.

Loan terms for federal student loans are standard and do not change based on application timing, so there is no negotiation involved. For private loans, the terms depend on the lender and your credit profile; applying late may limit your options or lead to less favorable terms. It is important to compare lenders carefully in either case.