2026 Best Student Loan Refinance for Medical School Debt

Student Finance & Loan Expert

Medical school graduates often face overwhelming debt with high-interest rates on multiple federal and private loans. Managing these debts while balancing residency and early career expenses can hinder financial stability and delay long-term goals like buying a home or saving for retirement.

Refinancing student loans can reduce monthly payments and cut interest costs, but choosing the right lender and plan is complex. This article examines top refinance options tailored for medical school debt, highlighting key features, eligibility criteria, and potential savings to help borrowers make informed decisions and improve their financial health efficiently.

- What is student loan refinancing for medical school debt and how does it work? Student Loan Refinancing for Med School Debt

- When does it make sense to refinance medical school loans instead of using federal plans? Refinancing vs. Federal Plans for Med School Loans

- How can you compare medical school refinance lenders, rates, and terms to find the best deal? Comparing Refinancing Lenders

- What credit score, income, and debt-to-income ratio do you need to refinance med school loans? Eligibility Requirements for Med School Debt Refinancing

- How does refinancing affect federal protections like IDR, forbearance, and loan forgiveness? The Impact of Refinancing on IDR, Forbearance, & Forgiveness

- Should doctors refinance during residency or wait until after training to get better terms? Should Residents Refinance or Wait?

- How do refinancing options differ for federal Direct, Grad PLUS, and private medical loans? Refinancing Options by Medical Loan Type

- What refinance strategies work best for physicians pursuing PSLF or other forgiveness programs? Refinancing vs. PSLF for Doctors

- How can co-signers, spouse income, and practice ownership impact medical loan refinancing? Co-Signers, Spouses, and Practice Equity in Refinancing

- What steps should you take to apply for refinancing and avoid common medical borrower mistakes? Refinancing Application Steps

What is student loan refinancing for medical school debt and how does it work?

Student loan refinancing options for medical school debt in the US allow borrowers to replace multiple existing loans with a single private loan, often at a lower interest rate. This simplifies repayment with one monthly payment and can reduce the overall interest paid. Refinancing works by applying to a lender who reviews your credit, income, and financial history to offer terms tailored to your situation.

How medical school loan refinancing works for US graduates is especially beneficial for those with high or variable interest rates or loans from different servicers. For example, refinancing an average debt of $206,924 from an 8% APR to a 5% APR could save around $316 per month and over $37,000 in total interest across 10 years.

Medical professionals face unique challenges such as long residencies and unstable income. Refinancing can help by offering flexible repayment schedules or switching from variable to fixed rates. However, refinancing federal loans means losing federal protections like income-driven repayment plans and Public Service Loan Forgiveness.

Success depends on good credit and steady income; applying with a cosigner often improves approval chances and lowers rates. When comparing lenders, consider interest rates, fees, repayment options, and benefits tailored to medical professionals such as deferment during residency or bonus programs. For some borrowers wondering if they can student loans pay rent, refinancing may indirectly ease overall financial burdens.

Refinancing is a strategic choice requiring careful evaluation of your financial situation, loan types, and career plans to maximize savings and loan manageability.

When does it make sense to refinance medical school loans instead of using federal plans?

Refinancing medical school loans offers potential savings when borrowers secure significantly lower interest rates than federal loans provide. With the average medical school debt around $223,130 and a median of $200,000 for the Class of 2025 (Credible, citing AAMC data), even a 1% interest reduction can save thousands over time. This strategy benefits those with strong credit, steady income, and less reliance on federal protections.

Consider refinancing medical school loans instead of federal plans if:

- You have a solid credit score and stable employment that qualifies you for private lenders with lower rates than federal fixed loans.

- You don't need Income-Driven Repayment (IDR) plans or Public Service Loan Forgiveness (PSLF), since refinancing federal loans removes access to these programs.

- You want a shorter repayment term to pay off loans faster, accepting potentially higher monthly payments for overall interest savings.

- You prefer consolidating multiple federal and private loans into one private loan with simplified payments and better terms.

Refinancing may not be ideal if you anticipate variable income early in your career or need federal forgiveness options. For example, residents with lower salaries might benefit more from federal Income-Contingent Repayment plans.

Knowing when to refinance medical school loans instead of federal plans is key to maximizing benefits and minimizing risks. Also, borrowers with less-than-perfect credit might explore student loans with bad credit and no cosigner as an alternative option.

Incorporating the benefits of refinancing medical school debt for U.S. students depends on creditworthiness and future earnings stability, making careful evaluation essential.

How can you compare medical school refinance lenders, rates, and terms to find the best deal?

Compare medical school loan refinance lenders by focusing on interest rates, loan terms, and borrower benefits. Personalized rate quotes based on credit score, income, and loan balance help in finding the best deal. Lower interest rates significantly cut repayment costs; for example, dropping from 8% to 5% on $250,000 in debt can save tens of thousands over the life of a loan. Since many graduates carry substantial debt, examining these rates closely is essential.

Evaluate terms and conditions for best medical school refinancing deals, especially repayment length and the choice between fixed or variable rates. Shorter terms often increase monthly payments but reduce total interest. Flexibility in payment schedules or temporary forbearance options can help manage financial strain during hardship.

Check borrower benefits such as autopay discounts, cosigner release options, and career-based repayment assistance. These perks provide added value beyond just rates and terms.

Be aware that refinancing federal loans with private lenders eliminates federal protections and forgiveness eligibility. Private refinancing is advisable only when interest rates are significantly lower and forgiveness is unlikely.

Use online comparison tools to streamline evaluations by creating side-by-side charts comparing interest rates, terms, fees, and benefits. Confirm no hidden fees like origination or prepayment penalties apply. For additional financial aid options related to education, consider looking into adult student scholarships.

What credit score, income, and debt-to-income ratio do you need to refinance med school loans?

Refinancing medical school loans generally requires a credit score of at least 670, with the best interest rates often reserved for those above 700. Credit scores reflect your creditworthiness, and scores over 700 can lead to significant savings over the loan term. Scores between 670 and 700 may still qualify but typically come with slightly higher rates.

Income requirements vary, but lenders usually look for stable earnings that comfortably cover your monthly debt. This typically means a gross annual income between $45,000 and $60,000. Income verification is essential-while a resident physician earning about $60,000 may qualify, a medical student without an income usually does not meet refinancing criteria.

Debt-to-income ratio qualifications for refinancing student loans in the US are also critical. A DTI ratio below 40% is preferred, indicating manageable debt relative to income. Some lenders allow up to 45% if other factors are strong, but a higher ratio often reduces approval chances.

Refinancing can provide tangible benefits. For example, lowering a $250,000 medical school loan from 8% to 5% APR over 10 years could reduce monthly payments by approximately $380 and save around $45,000 in total interest.

For those exploring related aid options, private nursing school loans may also be worth considering as part of your broader financial planning for healthcare education. More details can be found at private nursing school loans.

How does refinancing affect federal protections like IDR, forbearance, and loan forgiveness?

Refinancing federal student loans into private loans eliminates all federal protections such as Income-Driven Repayment (IDR) plans, forbearance options, and loan forgiveness programs. Federal IDR plans adjust monthly payments based on income and family size, offering flexibility private lenders do not match. Once you refinance, these benefits end immediately, and payments become fixed or variable according to the private lender's terms.

Forbearance and deferment options available with federal loans do not apply after refinancing. This means financial hardships cannot pause or reduce payments under federal safeguards. While some private lenders may offer hardship programs, they vary widely and often lack the reliability found in federal protections.

Loan forgiveness programs such as Public Service Loan Forgiveness (PSLF) and Teacher Loan Forgiveness are unavailable once you refinance. These programs require maintaining eligible federal loans. For instance, refinancing medical school loans with Panacea Financial offers fixed rates from 5.74% to 9.50% APR and terms ranging from 5 to 20 years, but it sacrifices federal benefits.

- Lower interest rates may reduce overall costs

- Federal protections offer payment flexibility and forgiveness opportunities

- Refinancing suits those less dependent on federal benefits

- Retaining federal loans benefits borrowers pursuing PSLF or anticipating financial instability

Should doctors refinance during residency or wait until after training to get better terms?

Doctors typically achieve better refinancing terms on medical school loans after completing residency due to more stable incomes and employment histories. During residency, salaries are lower and contracts often temporary, limiting eligibility for competitive refinancing offers. Attempting to refinance while still in training often leads to higher interest rates than those available afterward.

Refinancing soon after residency can lower an average medical school debt of around $206,924 from approximately 8% APR to about 5%. This reduction may save between $10,000 and $15,000 in interest over a decade, based on analyses by NerdWallet for loan refinancing scenarios projected in 2026. Delaying refinancing by two years risks losing these savings, especially if interest rates increase.

Residents may find income-driven repayment plans or federal programs more beneficial while in training, as these options provide payment flexibility without sacrificing eligibility for deferment or loan forgiveness programs such as Public Service Loan Forgiveness.

- Creditworthiness: Post-residency incomes and credit profiles improve, enabling better rates.

- Cash flow: Residents often prioritize manageable monthly payments over aggressive refinancing.

- Loan forgiveness eligibility: Refinancing federal loans during residency may disqualify borrowers from forgiveness programs.

Balancing short-term affordability and long-term financial benefits is critical. Refinancing after residency generally offers the most favorable rates and terms, optimizing savings and preserving loan forgiveness options.

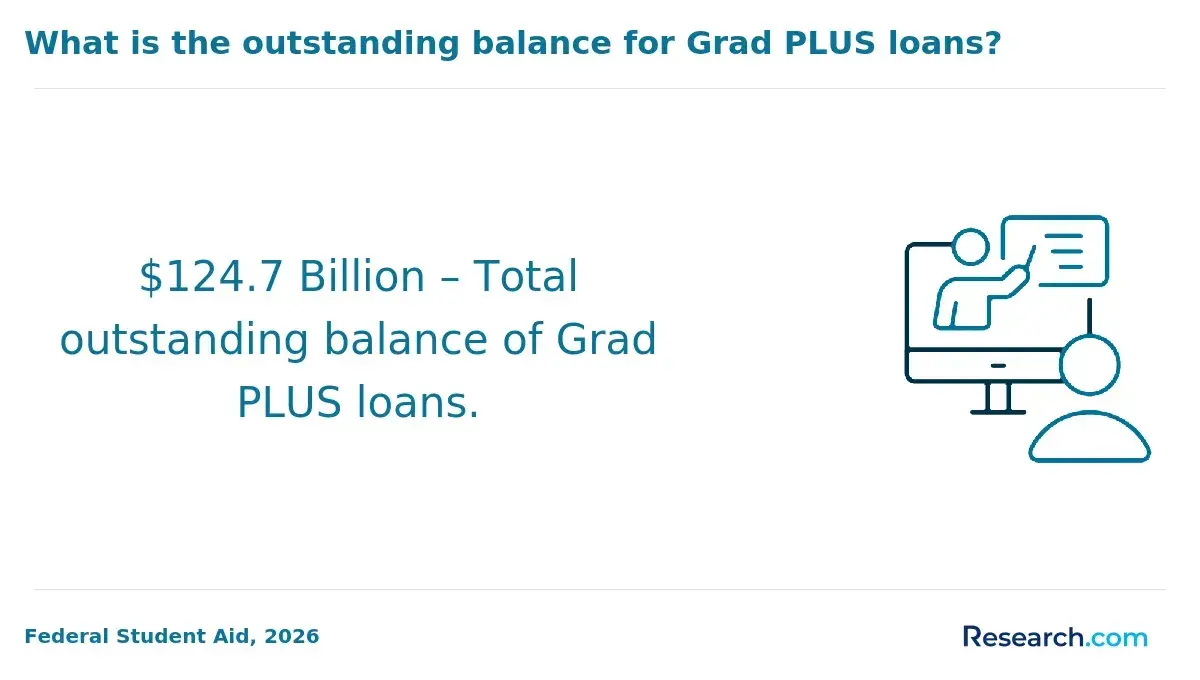

How do refinancing options differ for federal Direct, Grad PLUS, and private medical loans?

Refinancing options for federal Direct, Grad PLUS, and private medical loans vary widely in eligibility, benefits, and interest rates. Federal Direct loans have borrower protections such as income-driven repayment plans and Public Service Loan Forgiveness but tend to have higher fixed interest rates-8.05% for Grad PLUS loans. Refinancing these into private loans removes those federal benefits but can lower interest rates significantly for well-qualified borrowers.

Top medical-focused refinance lenders advertise fixed APRs starting around 4.1%-4.3%, creating nearly a 4 percentage point difference compared to federal Grad PLUS rates.

Grad PLUS loans have higher rates and fewer flexible repayment options than Direct loans. Borrowers should consider refinancing to lower long-term costs, but refinancing federal loans eliminates eligibility for forgiveness programs. Private medical loans, including refinanced ones, rarely offer such options. Factors like credit score, income stability, and career plans should guide decisions.

- Refinancing can simplify repayment by consolidating multiple loans.

- Borrowers pursuing Public Service Loan Forgiveness may prefer keeping federal loans.

- A resident with stable employment and strong credit might benefit from refinancing to a 4.2% fixed rate.

What refinance strategies work best for physicians pursuing PSLF or other forgiveness programs?

Physicians pursuing Public Service Loan Forgiveness (PSLF) or federal forgiveness programs should avoid refinancing federal loans into private loans, as this removes eligibility for PSLF, Income-Driven Repayment (IDR) plans, and other federal benefits. Roughly 25% of physicians planned to use these forgiveness programs, risking the loss of five- or six-figure forgiveness opportunities.

To optimize loan forgiveness, physicians should enroll in qualifying repayment plans like Income-Based Repayment (IBR) or Pay As You Earn (PAYE). These plans reduce monthly payments and apply toward forgiveness.

Refinancing typically makes sense only after completing or exiting forgiveness programs, such as when employment status changes disqualify one from PSLF or the forgiveness period ends. Federal consolidation can be an alternative to refinancing, as it combines loans and preserves forgiveness eligibility while potentially lowering rates.

For those with private loans or ineligible Parent PLUS loans, refinancing earlier may reduce interest and payment burdens. In such cases, it is crucial to select lenders offering flexible terms and no prepayment penalties.

- Avoid refinancing federal loans before exhausting PSLF or IDR benefits

- Maximize forgiveness eligibility through qualifying repayment plans

- Consider federal consolidation to maintain federal protections

- Evaluate refinancing only after losing forgiveness eligibility or with private loans

How can co-signers, spouse income, and practice ownership impact medical loan refinancing?

Co-signers can improve refinancing approval and secure better interest rates by adding credit reliability. Lenders view a skilled co-signer as a way to reduce risk, especially when the borrower's credit history is limited. However, both the borrower and co-signer share legal responsibility for repayment, so trust and communication are crucial.

Including a spouse's income often increases total qualifying income, potentially improving loan terms. When spouses file taxes jointly, combined income may be considered by lenders, enabling higher borrowing capacity or lower interest rates. It is important to confirm whether a lender accepts spouse income before applying to avoid unexpected issues.

Practice ownership significantly impacts refinancing capacity by providing income stability and growth potential. Medical practice owners usually report higher earnings and have more leverage with lenders. Specialists, for example, have a median income of around $429,500 versus $273,000 for primary care physicians.

This income difference means specialists might refinance $250,000 and pay it off in under seven years with payments near 15% of gross income, whereas primary care physicians may take closer to ten years at the same payment ratio.

- A co-signer can reduce interest rates but adds shared responsibility.

- Spouse income can boost qualifying income but varies by lender policy.

- Practice ownership usually increases income verification strength and repayment capacity.

What steps should you take to apply for refinancing and avoid common medical borrower mistakes?

Gather all current loan documents-including balances, interest rates, and repayment terms-to enable precise comparisons between refinancing offers. Check your credit score and report to spot errors and improve your creditworthiness, as lenders heavily weigh credit history for better rates.

Compare offers from at least three lenders. Research.com data shows that borrowers who shop around save an average of 1.70 percentage points on interest rates, which can amount to significant savings on large medical school debts. Use online calculators to estimate monthly payments and total interest costs for each option.

Look for lenders offering flexible repayment options like deferment or forbearance, important during income-variable phases such as residencies. Avoid fixed terms without fully understanding prepayment penalties or mandatory auto-debit discounts.

When applying, provide accurate financial information to avoid delays or denials. Common errors include underestimating expenses or overstating income. Be aware that refinancing federal loans into private loans eliminates federal protections such as income-driven repayment plans and Public Service Loan Forgiveness eligibility.

Clarify all fees, including origination or application fees, before committing. Refinancing is a significant financial decision; review all contracts thoroughly to prevent surprises.

Other Things You Should Know About

Medical school loans are considered federal student loans, which are generally not dischargeable through bankruptcy. To have these loans discharged, you must prove "undue hardship" in bankruptcy court, a challenging and rare standard to meet. Private medical school loans also rarely qualify for discharge, but exceptions depend on specific lender terms.

Federal loans offer several borrower protections including income-driven repayment plans, deferment, forbearance, and loan forgiveness programs such as Public Service Loan Forgiveness (PSLF). Refinancing with a private lender eliminates eligibility for these federal benefits, which can be critical if you face financial hardship or pursue certain employment paths.

Yes, refinancing federal medical school loans with a private lender results in losing eligibility for federal forgiveness programs like PSLF. These programs require borrowers to maintain federal loan status and meet specific employment and payment criteria, which refinancing permanently changes.

Many lenders allow borrowers to consolidate loans from different medical schools into a single refinance loan, simplifying management and potentially lowering monthly payments. However, refinancing consolidates your debts privately and does not qualify as federal consolidation, so federal protections and benefits do not transfer to the new loan.