2026 How to Help Your Child Pay for College Without Parent PLUS Loans

Student Finance & Loan Expert

Families often face rising college costs and hesitate to take out Parent PLUS loans due to high interest rates and strict borrowing limits. Parents may worry about the financial burden or their credit standing, while students look for alternative funding sources.

This situation leaves many seeking safer, more flexible ways to support college expenses without relying on Parent PLUS loans. Understanding these alternatives is crucial for managing education costs effectively and minimizing debt. This article examines practical strategies and financial options to help families finance college while avoiding Parent PLUS loans, offering clear guidance for informed decisions.

- How can we estimate our child's college costs and fill the gap without Parent PLUS loans? Estimating costs

- What federal student loan options can students use instead of Parent PLUS borrowing? Federal options

- How much can my child borrow in Direct Subsidized and Unsubsidized Loans each year? Student limits

- How do scholarships, grants, and work-study reduce the need for parent borrowing? Free aid & work

- When are private student loans a better choice than Parent PLUS loans for families? Private vs PLUS

- How can income-driven repayment and forgiveness make student loans more manageable for my child? IDR & forgiveness

- What role can 529 plans, savings, and payment plans play in avoiding Parent PLUS loans? Savings & plans

- How can we structure parent help through cosigning, shared payments, or family agreements? Structuring help

- What strategies help minimize interest costs and total debt for our child's education? Lowering costs

- How should families compare college offers to choose an affordable school without Parent PLUS loans? Comparing offers

How can we estimate our child's college costs and fill the gap without Parent PLUS loans?

Estimating total college costs involves accounting for more than just tuition. Include fees, room and board, textbooks, supplies, travel, and personal expenses. Public universities' average in-state tuition is around $10,000 annually, while private colleges average about $38,000. Living costs, which vary significantly by location, typically range from $8,000 to $15,000 per year.

To improve accuracy when estimating college costs without Parent PLUS loans, subtract known financial aid and scholarships. Most college websites offer net price calculators that reflect specific grants and institutional aid, providing a clearer picture than sticker prices.

Strategies to cover college expenses without Parent PLUS loans include:

- Maximizing federal student aid like Direct Subsidized and Unsubsidized Loans.

- Applying for scholarships and grants from private foundations and state programs.

- Participating in work-study or part-time jobs to manage daily expenses.

- Using 529 college savings plans for tax-advantaged savings dedicated to education.

- Considering private student loans after carefully comparing terms, interest rates, and borrower protections.

Many families seek ways to cover costs beyond tuition, including understanding if can student loans cover off-campus housing. Parent PLUS loans average a $32,000 balance per borrower, with 3.7 million borrowers owing over $111 billion collectively. Prioritizing alternative funding reduces long-term parental debt while keeping education affordable.

What federal student loan options can students use instead of Parent PLUS borrowing?

Students seeking federal student loan alternatives to Parent PLUS loans should consider Direct Subsidized and Unsubsidized Loans. These loans, accessible through the FAFSA process, offer fixed interest rates and flexible repayment plans.

Direct Subsidized Loans benefit undergraduates with demonstrated financial need by having the government pay interest while the student is in school. Direct Unsubsidized Loans have no need requirement but accrue interest throughout all periods. For those researching undergraduate federal loan options without parent borrowing, maximizing these loans is essential.

Annual federal borrowing limits vary: undergraduates can borrow between $5,500 and $7,500 per year based on their academic year and dependency. Graduate students may borrow up to $20,500 annually in Unsubsidized Loans.

Federal Work-Study programs provide part-time campus or community jobs funded by the government, helping to reduce loan dependence, though availability differs by institution.

Starting with "free money" - grants and scholarships is key. Over $4.0 billion in Pell Grants went unclaimed due to incomplete FAFSAs. Pell Grants, Supplemental Educational Opportunity Grants (SEOG), and TEACH Grants require no repayment but have specific eligibility rules.

Federal loans also feature lower origination fees and better repayment options than Parent PLUS loans, such as income-driven plans and possible forgiveness for public service.

Timely FAFSA submission and financial planning can help avoid costly Parent PLUS borrowing. For further guidance, consider resources like the Ascent student loan application as part of your research process.

How much can my child borrow in Direct Subsidized and Unsubsidized Loans each year?

Undergraduate students may borrow up to $5,500 annually in Direct Subsidized Loans based on their year and dependency status. First-year dependent students qualify for a maximum of $3,500, sophomores up to $4,500, while juniors, seniors, and independent students can access the full $5,500.

Direct Unsubsidized Loans provide higher limits, with dependent undergraduates able to borrow up to $7,500 annually, including the subsidized amount-and independent students or those with dependents eligible for up to $12,500. These student loan limits for direct subsidized and unsubsidized loans help manage borrowing responsibly.

Graduate and professional students, ineligible for subsidized loans, may borrow up to $20,500 per year in Direct Unsubsidized Loans. The total loan amount cannot surpass the cost of attendance minus other financial aid received, ensuring students do not exceed their financial needs.

Federal grants play an important role in reducing loan dependence. In 2024-25, students received $53.7 billion in federal grants, including $38.6 billion in Pell Grants, reflecting a 32% real increase since 2022-23, as reported by the College Board's Trends in Student Aid.

Submitting FAFSA applications promptly enhances access to these grants before exploring borrowing options.

Careful evaluation of borrowing limits, coupled with prioritizing subsidized loans that don't accrue interest while in school, safeguards long-term financial health. For those researching more advanced funding, exploring MBA loan options can be a valuable step.

How do scholarships, grants, and work-study reduce the need for parent borrowing?

Scholarships, grants, and work-study programs reduce the need for parents to borrow through Parent PLUS loans by providing free or earned financial aid that helps offset college costs. Scholarships and grants do not require repayment, making them among the most effective free financial aid options to minimize parent PLUS loan reliance.

Merit-based scholarships reward academic, athletic, or unique talents, while need-based grants, such as the Pell Grant, lower tuition and other expenses based on financial need.

Work-study programs let students earn money during college, helping cover living expenses with flexible, tax-free earnings from federally funded campus jobs aligned with academic schedules. These earnings reduce dependence on loans and ease financial burdens.

Choosing cost-effective colleges is key to limiting borrowing. Public community colleges charge about $3,990 annually for full-time in-district students, significantly less than the average in-state tuition at public four-year universities.

Starting at a community college or picking an in-state public university helps bridge financial aid gaps, thus reducing parent borrowing needs.

Combining scholarships, grants, work-study earnings, and strategic college choices creates a layered approach that lowers student expenses. Families should actively pursue scholarships, complete the FAFSA to access grants, and consider campus jobs early.

Those seeking more financial flexibility might explore banks with student loan refinance options to manage or reduce parent PLUS loan burdens.

When are private student loans a better choice than Parent PLUS loans for families?

Private student loans generally offer lower interest rates and more flexible repayment plans compared to Parent PLUS loans, making them a cost-effective option for borrowers with strong credit or a qualified cosigner. These loans often include repayment choices like interest-only or deferred plans, which are typically unavailable through Parent PLUS loans.

Families with variable income or those wishing to avoid strict federal Parent PLUS collection rules may prefer private loans due to their adaptable payment schedules.

Private loans are also suitable for non-traditional students or those enrolling in programs where federal aid limits borrowing. They can cover additional education expenses such as technology or living costs without increasing federal loan debt.

Loan fees differ significantly: Parent PLUS loans carry origination fees up to 4.228%, while some private lenders waive fees altogether. However, private loans usually lack federal protections like deferment, forbearance, and income-driven repayment options, which should be carefully considered.

Work-Study and part-time jobs remain effective ways to reduce education costs. Nearly half of full-time undergraduates worked an average of 22 hours weekly, helping cover about a quarter of college expenses. Leveraging earnings from such programs can minimize loan reliance, regardless of the loan type chosen.

How can income-driven repayment and forgiveness make student loans more manageable for my child?

Income-driven repayment (IDR) plans adjust monthly student loan payments based on income and family size, often lowering payments to 10%-15% of discretionary income.

This makes loans more manageable during early career stages or times of financial strain. IDR plans include a loan forgiveness option: after 20 to 25 years of qualifying payments, remaining balances may be forgiven. For those in public service or nonprofit roles, forgiveness can occur after just 10 years through Public Service Loan Forgiveness (PSLF).

For example, a graduate earning $40,000 annually might pay about $200 monthly under an IDR plan instead of $400 or more with standard plans. After consistent payments over 20 years, any leftover loan balance can be eliminated, allowing more financial freedom for savings or expenses.

However, enrolling in IDR requires annual income recertification and may extend repayment time, increasing total interest paid. Prospective borrowers should consider these trade-offs carefully and select a plan aligned with their financial situation.

According to the U.S. Bureau of Labor Statistics, individuals with a bachelor's degree earn a median income of $61,600, 57% higher than those with only a high school diploma. This income advantage highlights the importance of strategically managing student loan payments to enhance returns on educational investment.

What role can 529 plans, savings, and payment plans play in avoiding Parent PLUS loans?

529 plans provide a tax-advantaged way to save for qualified education expenses, reducing the need for Parent PLUS loans. Contributions grow tax-free, and withdrawals for tuition, room, and board are federally tax-exempt. Starting early with these plans allows families to accumulate significant funds before college.

While regular savings or custodial accounts offer flexibility, they lack the tax benefits of 529 plans. These accounts can cover non-qualified costs like books or transportation, making them useful supplements. A combined approach with both savings vehicles helps minimize student debt.

Many colleges offer payment plans that break tuition into monthly installments without added interest. These plans improve affordability by avoiding large lump-sum payments and reducing reliance on costly loans. Prospective students should explore these institutional payment options during the enrollment process.

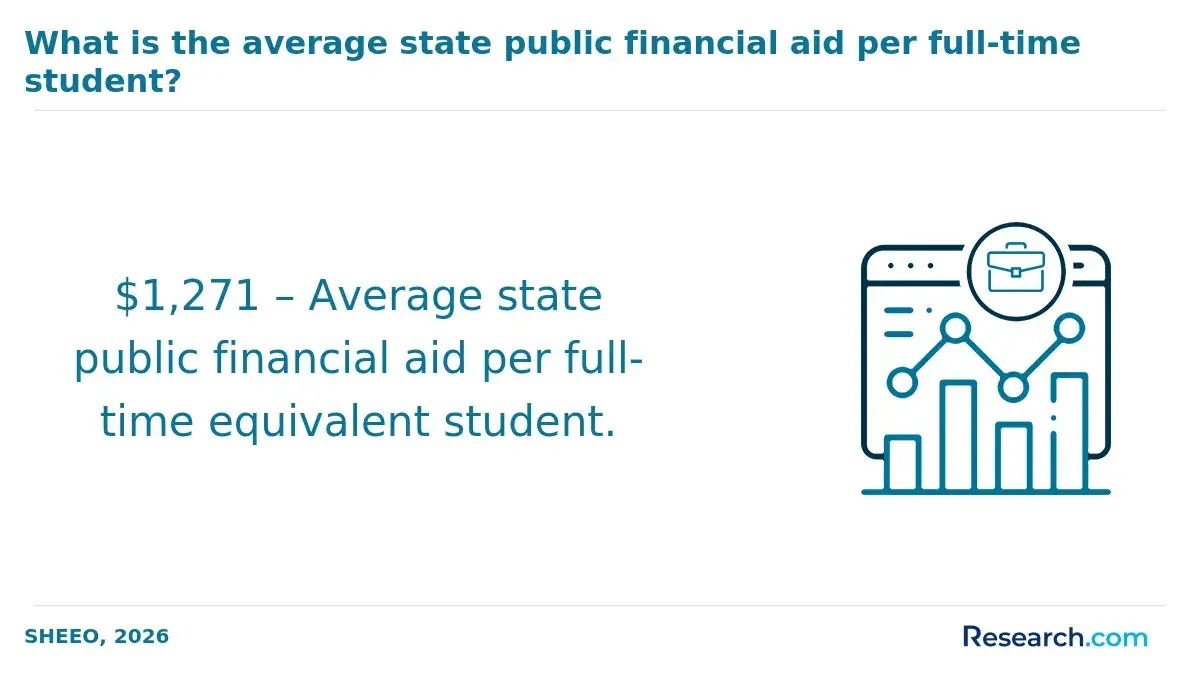

State grants and institutional aid also play a critical role in offsetting college expenses. The State Higher Education Finance Report 2025 notes a 5.1% rise in state public financial aid, reaching $1,271 per full-time equivalent student, even amid a slight decline in overall state funding. Applying through FAFSA and other channels can significantly lower borrowing needs.

A strategic mix of 529 plans, savings, payment plans, and maximizing grants and aid can effectively reduce or eliminate the necessity for Parent PLUS loans. Early preparation and exploring all financial options are key to successful college funding.

How can we structure parent help through cosigning, shared payments, or family agreements?

Parents have several options to help finance college without relying on Parent PLUS Loans. Cosigning private student loans or lines of credit can improve loan eligibility and interest rates by using the parent's credit. However, cosigners assume full repayment responsibility if the student defaults, which can negatively affect their credit and finances.

Shared payment strategies divide expenses between parent and student, such as parents covering tuition while students pay for room, board, and personal costs funded through part-time earnings or scholarships. This reduces loan dependence and encourages financial responsibility for students.

Family agreements formalize these arrangements by setting clear payment plans, roles, and consequences for missed payments. Written contracts help prevent misunderstandings and can include other relatives' contributions or future income-based repayment terms.

Additional credit-earning opportunities like dual enrollment, Advanced Placement (AP) courses, and CLEP exams can save significant tuition costs.

According to the U.S. Department of Education, Institute of Education Sciences, high school students in dual enrollment programs save an average of $12,600 on future college tuition. These options lower the loan amount needed by shortening time-to-degree and reducing upfront costs.

Combining cosigning, shared payments, and family agreements promotes transparency and lessens debt burdens without defaulting to Parent PLUS Loans, allowing families to tailor solutions according to credit profiles and long-term financial goals.

What strategies help minimize interest costs and total debt for our child's education?

Have your child pursue federal student loans before considering Parent PLUS loans. Students received significantly more federal loans than parents did in Parent PLUS loans, showing generally lower costs when students borrow first. Federal student loans typically offer lower interest rates and more flexible repayment options, which can reduce total debt over time.

Opt for schools with lower tuition or those offering merit scholarships. Starting at a community college for two years before transferring to a four-year university can cut expenses significantly. Choosing in-state public universities also tends to save thousands compared to private or out-of-state schools.

Encourage part-time work or paid internships to help cover costs and build professional experience. Applying for grants and scholarships based on the student's field, background, or achievements is another effective way to lower loan reliance.

Consider a lighter course load during some semesters to lessen borrowing needs by balancing work and study. Refinancing federal loans post-graduation into lower-interest private loans is possible but removes federal protections, so weigh that decision carefully.

Maintain a strict budget for living expenses to avoid excessive borrowing. Since Parent PLUS loans carry higher interest and fees than federal loans, they should be a last option. Prioritizing student federal loans and minimizing costs can significantly reduce long-term debt and interest paid.

How should families compare college offers to choose an affordable school without Parent PLUS loans?

Families should focus on the net cost after grants, scholarships, and federal student loans, excluding Parent PLUS loans, when comparing college financial aid offers.

Begin by collecting all award letters aligned to the same academic year and distinguish between gift aid (grants and scholarships) and self-help aid (loans and work-study). Prioritize offers with higher grant aid and lower loan amounts, especially federal loans that typically offer better interest rates and repayment terms.

Consider the total cost of attendance (COA), including tuition, fees, room, board, and living expenses. Keep in mind that COA varies between institutions, and the average total aid per full-time undergraduate highlights the importance of coordinating multiple funding sources over several years rather than focusing solely on the first year's price.

Develop a multi-year plan to anticipate changes in aid and costs, reviewing renewal policies, scholarship eligibility, and possible tuition increases. Check each school's flexibility regarding work-study or part-time jobs to help manage expenses.

Request detailed loan term breakdowns if federal student loans are part of the package, and avoid private loans or credit cards due to high costs. Families should compare total COA minus grants and scholarships to reveal the true net price and weigh federal loans carefully before dismissing any offers.

- Compare total COA minus grants and scholarships for true net cost.

- Consider federal student loans with favorable terms before excluding offers.

- Review aid renewal policies and multi-year sustainability.

- Include work-study or employment income in budget planning.

- Avoid offers requiring expensive private loans by assessing self-help aid.

Other Things You Should Know About

Yes, your child can consolidate federal student loans through the Direct Consolidation Loan program. This combines multiple federal loans into one loan with a single monthly payment, which can simplify repayment. However, consolidating may extend the repayment term and increase total interest paid, so it's important to weigh the pros and cons before proceeding.

If your child faces difficulty repaying their student loans, they can consider options such as deferment, forbearance, or enrolling in an income-driven repayment plan. These options can temporarily reduce or pause payments but may increase total interest costs. It's crucial to communicate with the loan servicer promptly to explore available solutions and avoid default.

No, Parent PLUS loans are taken out by the parent borrower and appear on the parent's credit report, not the student's. This means the loan will not affect your child's credit history directly, but the parent's creditworthiness is critical to obtaining the loan and influences the loan's terms.

Private student loans generally lack many borrower protections that federal loans provide, such as income-driven repayment plans and loan forgiveness programs. Some private lenders may offer limited forbearance or deferment options, but terms vary significantly. It is essential to review the specific lender's policies carefully before borrowing.