2026 Student Loan Checklist Before You Apply

Student Finance & Loan Expert

Applying for student loans can overwhelm prospective graduate students, especially those transitioning from unrelated undergraduate fields. Confusing terms, varying interest rates, and differing repayment options often lead to uninformed decisions that may impact financial stability for years. Many face difficulties assessing eligibility or estimating long-term costs before committing to debt. This uncertainty can delay education plans or increase financial risk. This article outlines a clear checklist to navigate loan applications effectively, helping readers understand crucial factors, evaluate their options, and prepare for responsible borrowing to support their academic and career goals.

- What should you check about your college costs before deciding how much to borrow in student loans? College Costs

- How do federal and private student loans work, and which type should you consider first? Federal vs. Private

- What steps do you need to take to complete the FAFSA and apply for federal student aid? FAFSA Steps

- What are the key eligibility requirements for federal student loans for students and parents? Loan Eligibility

- How do student loan interest rates, fees, and borrowing limits affect your total cost? Rates & Limits

- How do undergraduate, graduate, and parent PLUS loans differ in terms, benefits, and risks? Loan Types

- How can you estimate your future monthly payments and choose a federal repayment plan? Monthly Payments

- What student loan forgiveness, cancellation, and discharge options might you qualify for? Forgiveness Options

- When does refinancing or consolidating student loans make sense, and what are the trade-offs? Refinance vs. Consolidate

- How do deferment, forbearance, delinquency, and default work, and how do they affect credit? Deferment & Default

What should you check about your college costs before deciding how much to borrow in student loans?

Before deciding how much to borrow, thoroughly review your total college costs, including tuition, mandatory fees, and room and board. These expenses vary between public, private, and for-profit institutions. Also factor in textbooks, supplies, transportation, and personal costs, which often add up annually. Verify these figures with your school's financial aid office or website for precise estimates. Understanding average college costs and financial aid impact can help make smarter borrowing decisions.

Consider any scholarships, grants, or work-study opportunities you have or expect to receive, as these reduce your need to borrow. Check if your financial aid package includes institutional or state aid, which could lower your out-of-pocket expenses.

Account for possible future cost changes, such as tuition increases or shifts in living expenses. Prepare for worst-case scenarios to avoid financial shortfalls, remembering that loan fees and interest rates affect the total repayment amount. Familiarize yourself with student loan borrowing limits in the United States to avoid over-borrowing.

Keep in mind the average federal loan for undergraduates was $7,230, a 14% drop since 2010-11, indicating many students borrow less than their maximum eligibility to limit debt. To understand what qualifies as covered expenses, see this guide on can you use student loans for living expenses.

Ask yourself:

- Have I included all direct and indirect educational costs?

- What non-loan financial aid can reduce my borrowing?

- Can I cover some expenses with savings or part-time work?

- How will borrowing more affect my future repayment and credit?

How do federal and private student loans work, and which type should you consider first?

Federal student loans, issued by the U.S. Department of Education, offer advantages such as lower interest rates and flexible repayment options compared to private loans. These include Direct Subsidized, Direct Unsubsidized, and PLUS loans. A key benefit of subsidized loans is that they do not accrue interest while you are in school, which reduces costs significantly. Understanding how federal student loans work and benefits can help you make informed borrowing decisions.

Federal loans comprised 90.9% of the nation's $1.833 trillion student loan portfolio, reflecting their affordability and borrower protections, while private loans made up only 9.1%. Private loans are provided by banks, credit unions, or online lenders and often require a credit check with interest rates varying according to creditworthiness and market conditions. These typically have fewer repayment flexibility options and are often best as a secondary choice after maximizing federal loan eligibility.

The differences between federal and private student loans include repayment plans; federal loans offer income-driven repayment that adjusts based on your earnings, whereas private loans usually have fixed or variable rates with limited flexibility. Private loans may assist in covering tuition gaps or additional expenses. Consider key questions such as:

- Can you obtain a federal loan without a credit check?

- Do you qualify for subsidized loans based on financial need?

- Does the private lender offer cosigner release after timely payments?

For students seeking more independence, exploring independent student loans can be a useful resource. Starting with federal options ensures more affordable terms and greater protections before considering private loan alternatives.

What steps do you need to take to complete the FAFSA and apply for federal student aid?

To complete the FAFSA application process for federal student aid eligibility steps, start by gathering essential documents such as your Social Security number, federal income tax returns, W-2s, and records of untaxed income. Dependent students will also need their parents' financial information. Creating an FSA ID online is required for electronically signing the FAFSA.

The FAFSA application becomes available after October 1, 2025, at studentaid.gov for the 2026-2027 academic year. Enter accurate personal and financial information to avoid delays or reduced aid eligibility. Using the IRS Data Retrieval Tool helps automatically transfer tax information securely.

Review each section carefully, including questions on dependency status, scholarships, and prior college attendance. Submit the FAFSA before your college's priority deadline since many institutions award federal aid on a first-come, first-served basis. Always save a copy of your confirmation page for your records.

After submission, you will receive a Student Aid Report (SAR) summarizing your details. Verify the accuracy and respond promptly to any requests from your financial aid office. Completing FAFSA accurately can significantly affect your financial planning, especially as students graduating in 2025 had average loan debts of $39,550, an increase of 117% since 2007.

For borrowers, exploring options like the best MBA student loans can provide more manageable financing solutions as you plan your educational investment.

What are the key eligibility requirements for federal student loans for students and parents?

To qualify for federal student loans in 2026, students and parents must meet specific eligibility requirements set by the U.S. Department of Education. Applicants must be U.S. citizens or eligible non-citizens, such as permanent residents. Enrollment has to be at least half-time in an accredited degree, certificate, or eligible program at a participating institution. Maintaining satisfactory academic progress, as defined by the school, is essential to remain eligible. These federal student loan eligibility criteria for US students and parents also include the completion of the Free Application for Federal Student Aid (FAFSA), which assesses financial need and qualification.

For Direct PLUS Loans, available to parents and graduate students, a credit check is required. Those with adverse credit must either provide an endorser or document extenuating circumstances. Students cannot have outstanding defaulted federal student loans or owe refunds on federal grants; these issues disqualify them until resolved. Male students aged 18-25 must comply with Selective Service registration. Parental eligibility differs mainly regarding the Direct PLUS Loan, where parents borrow for dependent undergraduates and must meet separate credit standards, especially if the student drops below half-time enrollment.

The National Center for Education Statistics noted that in 2020-21, only 38% of first-time, full-time undergraduates took federal loans, down from 50% in 2010-11. This trend reflects more cautious borrowing behaviors and possible changes in financial strategy or eligibility even before recent loan repayment pauses. Prospective borrowers may also consider exploring student loan refinance lenders to manage debt effectively.

Requirements for federal student aid qualification in the United States continue to evolve alongside these trends, influencing how students and families plan for college financing.

How do student loan interest rates, fees, and borrowing limits affect your total cost?

Interest rates, fees, and borrowing limits greatly influence the total repayment amount and financial strain after graduation. For instance, a 5% fixed interest on a $20,000 loan results in $1,000 additional interest yearly if unpaid. Variable rates may start low but can increase, making costs unpredictable. Fixed rates provide steadiness though they may initially be higher.

Loan fees, such as origination fees typically between 1% and 4%, are deducted upfront from the disbursed amount. These fees lower the funds you receive but do not reduce the principal, increasing the overall cost. Additional fees, including late charges and prepayment penalties, can add to expenses, so it's important to know all fee structures before borrowing.

Borrowing limits set the maximum amount you can borrow annually and in total. Federal undergraduate limits usually range from $5,500 to $12,500 per year, with higher limits for graduate programs. Exceeding these limits often means turning to private loans, which usually have higher interest rates and less favorable terms.

Missed payments quickly increase financial pressure; in Q4 2025, 10.0% of federal student loan dollars were delinquent (Education Data Initiative, "Student Loan Debt Statistics 2026"). To manage costs effectively:

- Compare fixed versus variable interest rates carefully.

- Consider all fees, not just interest rates.

- Plan repayments based on realistic income.

- Stay within federal borrowing limits to avoid expensive private loans.

How do undergraduate, graduate, and parent PLUS loans differ in terms, benefits, and risks?

Undergraduate, graduate, and parent PLUS loans each carry different terms and risks that influence borrowing and repayment strategies. Undergraduate federal loans generally offer lower interest rates and more forgiving repayment options. For instance, Direct Subsidized Loans for undergraduates provide interest subsidies while students remain enrolled, reducing the overall cost.

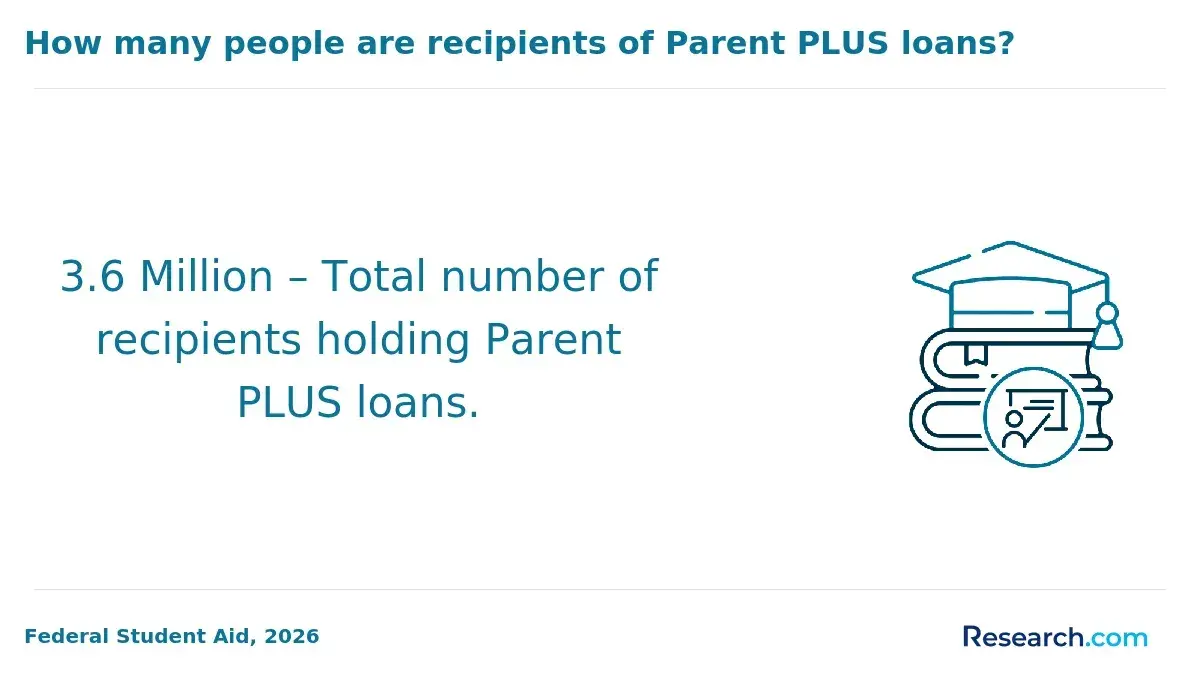

Graduate loans, such as Direct Unsubsidized Loans, begin accruing interest immediately with no subsidy, increasing the total debt. Although graduate and professional students make up only about 21% of federal borrowers, they hold approximately 56% of the outstanding federal student loan debt, reflecting larger borrowing needs. Parent PLUS loans enable parents to borrow for their dependent undergraduate students but come with higher interest rates and fees, no borrowing caps except the cost of attendance, and immediate repayment requirements, potentially affecting cash flow.

Key distinctions include:

- Eligibility: Undergraduates qualify for subsidized and unsubsidized loans; graduates only for unsubsidized; parents for PLUS loans exclusively.

- Interest rates: Graduate and PLUS loans tend to have higher fixed rates than undergraduate loans.

- Repayment: Parent PLUS loans require repayment during school unless deferment is approved; graduate loans accumulate interest without subsidy.

- Loan limits: Undergraduates have annual limits; graduates and parents can borrow larger sums, increasing debt burden.

Borrowers should carefully weigh these factors. Graduate students often face heavier long-term debt, while parent borrowers must assess repayment capacity to avoid default. Selecting the right loan mix depends on understanding each loan's protections and repayment options based on borrower status and educational level.

How can you estimate your future monthly payments and choose a federal repayment plan?

Use the Department of Education's Loan Simulator to estimate future federal student loan payments. This tool calculates your projected monthly payments based on your loan balance, interest rates, and income across all federal repayment plans, including Standard 10-year, Graduated, Extended, and Income-Driven Repayment (IDR) plans.

Carefully assess your income prospects. If you expect lower earnings initially or income fluctuations, IDR plans such as Revised Pay As You Earn (REPAYE), Income-Based Repayment (IBR), or the SAVE plan can significantly reduce payments by capping them as a percentage of discretionary income.

The SAVE plan is particularly impactful. About 8 million borrowers benefit from monthly payments cut by over 50% compared to the standard plan. For example, a typical $400 monthly payment might drop to around $180 under SAVE, helping low- and moderate-income borrowers.

When deciding on a plan, consider:

- Your current and future income and family size

- The expected repayment duration

- Eligibility for Public Service Loan Forgiveness (PSLF) or other forgiveness program

It's important to reassess your repayment strategy regularly, as income changes affect payments and forgiveness timelines. Annual use of the Loan Simulator helps ensure you select the most cost-effective option and avoid default.

What student loan forgiveness, cancellation, and discharge options might you qualify for?

Student loan forgiveness and discharge options depend on your loan type, employment, and personal situation. Federal programs include Public Service Loan Forgiveness (PSLF), which requires 10 years of qualifying payments while working full-time for a government or nonprofit employer. Teachers may qualify for Teacher Loan Forgiveness by working five consecutive years at low-income schools, receiving up to $17,500 in loan cancellation.

Income-driven repayment (IDR) plans forgive the remaining balance after 20 or 25 years of qualifying payments, varying by plan. Certain professions, such as healthcare and social work, may benefit from state-specific forgiveness programs that complement federal options.

Discharge options cancel loans under specific conditions like Total and Permanent Disability Discharge, available through Social Security Administration or physician certification. Closed School Discharge applies if your school closes during or shortly after your enrollment. Borrowers misled by their school may seek Borrower Defense to Repayment if legal violations occurred.

Data from the Urban Institute's Federal Student Aid Portfolio Chartbook shows that only 45% of federal loan borrowers from 2010 to 2012 had reduced their principal by the time of this report, with many facing increased balances due to accrued interest. This highlights why evaluating your eligibility for forgiveness programs and understanding your school's outcomes is vital before borrowing.

When does refinancing or consolidating student loans make sense, and what are the trade-offs?

Refinancing or consolidating student loans can be a strategic move to lower interest rates, reduce monthly payments, or simplify loan management. Borrowers with strong credit scores and high federal loan rates may save significantly by refinancing through a private lender. This option often offers access to lower rates and the ability to switch from variable to fixed interest rates for more predictable payments.

Consider refinancing if:

- You have stable income and a solid credit history

- You prefer fixed interest rates over variable

- You don't rely on federal protections like income-driven repayment or loan forgiveness

Consolidation combines multiple federal loans into one payment, which can make managing debt easier. It may lower monthly payments by extending the repayment term and provide access to alternative repayment plans or deferment options.

Consolidation benefits include:

- Simplified payments for multiple loans

- Restored eligibility for deferment or forbearance

- Potentially new repayment options

However, refinancing with private lenders means losing federal benefits such as income-driven repayment and public service loan forgiveness. Consolidation might reset the clock on forgiveness eligibility. Weigh the short-term savings against the possible increase in total interest and loss of protections before deciding.

With many adults delaying financial goals due to student loan payments, choosing the right option can improve financial stability and reduce budget stress.

How do deferment, forbearance, delinquency, and default work, and how do they affect credit?

Deferment and forbearance temporarily suspend or reduce student loan payments but impact credit in different ways. Deferment lets you pause payments without accruing interest on subsidized loans, keeping your account current and protecting your credit score. This option is useful if you return to school or face unemployment.

Forbearance also postpones payments, but interest continues to accumulate on all loan types, increasing your balance over time. While this means your account stays current with minimal immediate credit impact, long-term use may signal financial trouble to lenders.

Delinquency occurs when payments are late by 30 days or more, damaging your credit score and making future borrowing more difficult or expensive. If payments remain unpaid for 270 days, your loan enters default, severely damaging your credit for seven years and possibly leading to wage garnishment or tax refund seizure.

With the average debt-to-income ratio at 58% for many borrowers, proactively contacting your loan servicer about deferment or forbearance can help avoid these pitfalls.

Other Things You Should Know About

Yes, federal student loans do not require a cosigner because they are based on financial need and eligibility rather than credit history. However, many private student loans often require a cosigner, especially for borrowers with limited or poor credit. Some private lenders offer loans without a cosigner, but these typically have higher credit standards and interest rates.

Failing to pay student loans can lead to serious consequences, including late fees, damage to your credit score, and loan default. Defaulting on federal loans typically occurs after 270 days of missed payments and can result in wage garnishment, tax refund withholding, and loss of eligibility for additional federal aid. Private lenders may pursue collections or legal action depending on your agreement.

Yes, student loans can cover a variety of education-related expenses beyond tuition. These include room and board, textbooks and supplies, transportation, and sometimes even computer equipment required for coursework. It's important to borrow only what you need for legitimate education costs to avoid excessive debt.

It might be possible to adjust your loan amount after applying, but policies vary by loan type and lender. For federal loans, you can usually request an increase or decrease through your school's financial aid office before the loan is disbursed. Private lenders may allow modifications but often require a new application or approval process.