2026 How to Pay for College If You Need Money Fast

Student Finance & Loan Expert

Facing unexpected tuition deadlines or rapid enrollment requirements can leave students scrambling for funds. Graduate students and professionals changing careers often encounter urgency when financial aid doesn't come through in time. Without quick access to money, opportunities may be lost or delayed, affecting academic and career progress. Navigating fast funding options while avoiding excessive debt is critical. This article explores practical strategies for securing money swiftly, focusing on student loans and alternative resources tailored to graduate-level needs to help readers manage urgent financial demands effectively.

- How can I get money fast for college without making expensive mistakes? Fast money

- What are the quickest federal aid options I can access right now? Fast federal aid

- How do emergency grants, advances, and payment plans work for urgent costs? Emergency help

- How does FAFSA work and when should I apply if I need money quickly? FAFSA timing

- What are the main differences between federal and private student loans? Federal vs private

- How much can I borrow in student loans and what interest rates should I expect? Limits & rates

- What fast private student loan options exist and how do I compare lenders? Fast private loans

- How do repayment plans, deferment, and forbearance affect my monthly budget? Repayment choices

- Which loan forgiveness and discharge programs could reduce what I ultimately repay? Forgiveness options

- How can parents and graduate students cover gaps when undergraduate aid isn't enough? Parent & grad loans

How can I get money fast for college without making expensive mistakes?

To secure quick college funds without expensive mistakes, start by prioritizing federal student aid. Completing the FAFSA unlocks access to Pell Grants and low-interest federal loans that offer borrower protections and flexible repayment plans. Avoid private loans initially since they typically carry higher interest rates and fewer benefits. If you are currently employed, explore employer tuition assistance programs as they provide direct funding without the obligation of repayment.

If you are seeking ways on how to get money fast for college without costly errors, consider scholarships and grants based on academic merit, field of study, or personal background, as these don't require repayment. Use scholarship search tools diligently and apply broadly; missing out on these opportunities narrows your funding options.

Part-time jobs or work-study programs can also help supplement your finances quickly without increasing debt. Some institutions offer emergency grants or short-term loans with low or no interest for immediate cash needs, but be sure to verify their terms carefully to avoid hidden fees or unfavorable conditions.

Be cautious about quick cash alternatives like payday loans or high-interest credit cards, which can lead to unmanageable debt. Instead, consult your school's financial aid office for personalized advice. For additional options, consider exploring urgent student loans for college, but always verify loan offers through official channels.

What are the quickest federal aid options I can access right now?

The fastest federal aid options available immediately include Direct Subsidized and Unsubsidized Loans and Federal Pell Grants. Completing the FAFSA (Free Application for Federal Student Aid) promptly is essential to unlock these resources without delay. Federal Direct Loans typically disburse within two to four weeks after schools process your aid application. Subsidized loans depend on financial need, while unsubsidized loans offer up to $5,500 to $7,500 per academic year for most undergraduates regardless of income. These are among the quickest federal student aid programs available.

Pell Grants offer immediate aid based on your Expected Family Contribution (EFC) and do not require repayment. These grants can reach up to $7,395 for the 2026 award year. According to the Education Data Initiative, scholarships and grants cover about 25% of students' annual education costs, averaging $7,500 per student, highlighting their importance in offsetting tuition expenses.

For urgent federal college funding, Federal Direct PLUS Loans serve graduate students and parents of undergraduates. They require a credit check but offer higher borrowing limits and quicker approval than private loans. Federal Work-Study is also available but depends on securing a campus job and may not provide funds quickly.

Some colleges provide emergency aid advances or short-term institutional loans in urgent situations. Additionally, students interested in alternative options can research ascent student loans for faster access to funds.

How do emergency grants, advances, and payment plans work for urgent costs?

Emergency grants provide quick, no-repay financial aid to cover urgent college costs such as housing, textbooks, or medical bills. These funds usually come from institutional or federal sources and require minimal application, making them a vital emergency grant option for college expenses. However, the amounts are often limited, ranging from a few hundred to several thousand dollars.

Short-term advances, including cash advances on financial aid refunds or paycheck advances from campus jobs, offer immediate relief but must be repaid through future aid or earnings, influencing cash flow.

How payment plans help cover urgent college costs by allowing tuition or fees to be paid over several months, easing the financial pressure of lump-sum payments. Many schools offer low-interest or interest-free plans with an initial deposit and scheduled installments aligned with the academic calendar, reducing reliance on high-interest credit cards or loans.

Proactive communication with a school's financial aid or bursar's office is crucial to access these options. Sallie Mae's "How America Pays for College" report shows that 30% of families skipped the FAFSA, missing out on thousands in grants and subsidized aid, which are important for managing emergencies.

Students should file the FAFSA promptly, explore campus emergency funds, request payment plans, and learn about financial aid for adults returning to college to optimize support for unexpected college expenses.

How does FAFSA work and when should I apply if I need money quickly?

FAFSA determines eligibility for federal grants, work-study, and student loans by using financial information from two years prior, known as the "prior-prior year." For aid in 2026, applicants should use 2024 tax data, allowing for faster processing than current-year data. After submitting FAFSA, you'll receive a Student Aid Report (SAR) summarizing your expected aid based on your calculated Expected Family Contribution (EFC).

To get money fast, it's crucial to apply as soon as FAFSA opens on October 1 for the upcoming academic year. Schools usually award funds on a first-come, first-served basis, so prompt filing improves access to need-based aid. Students preparing to start college in fall 2026 should file in October 2025 and check specific school deadlines, as some states and institutions set earlier cutoff dates.

If urgent funds are needed for summer or short-term programs, consult your financial aid office to explore options like emergency grants or accelerated loan disbursements. Should any delays happen in processing, contact your school's financial aid office immediately; they may offer provisional aid or alternative resources such as short-term loans or private grants to bridge the gap.

Negotiated aid packages can dramatically lower tuition. According to College Board research, average net tuition and fees for full-time, in-state students at public four-year colleges have decreased significantly over recent years, illustrating how FAFSA-driven aid reduces sticker prices effectively.

Understanding how the FAFSA application process works can help you plan timely submissions and maximize aid opportunities. Also, if considering additional funding, it's wise to review options from the best banks that offer student loans.

What are the main differences between federal and private student loans?

Federal and private student loans differ mainly in their source, terms, and borrower protections. Federal loans come from the U.S. government and offer fixed interest rates set by law, usually lower than private loans. Private loans-which come from banks, credit unions, or other lenders-often have variable or higher fixed rates tied to creditworthiness.

Repayment plans also vary widely. Federal loans provide flexible options like income-driven repayment, deferment, and forbearance, helping those facing financial hardship. In contrast, private loans seldom offer such protections, making repayment potentially more difficult for borrowers with unstable incomes.

Eligibility requirements are another key distinction:

- Federal loans require completing the Free Application for Federal Student Aid (FAFSA) and generally have lenient credit standards.

- Private loans demand good credit or a co-signer, limiting access for many students.

Only federal loans typically include forgiveness options such as Public Service Loan Forgiveness, which can influence long-term financial planning. Private lenders do not provide loan forgiveness.

According to the College Board's financial aid trends, grants now make up 68% of undergraduate aid, with many schools expanding emergency and need-based grants. This growth lessens dependence on loans but increases the importance of carefully considering loan types.

How much can I borrow in student loans and what interest rates should I expect?

Federal student loan limits allow undergraduates to borrow up to $31,000 in Federal Direct Loans throughout their academic career. This amount combines both subsidized and unsubsidized loans. Annual limits vary by year: freshmen may borrow up to $5,500, sophomores $6,500, and juniors and seniors up to $7,500 each. Graduate and professional students have higher limits but under different terms.

Interest rates on federal student loans are fixed and set annually by the U.S. Department of Education. For loans disbursed in 2026, undergraduate Direct Subsidized and Unsubsidized Loans carry rates between 5.50% and 6.00%. Graduate Direct Unsubsidized Loans can have rates up to about 6.50%. By comparison, private student loans often have variable rates ranging from 4% to over 12%, depending on the borrower's credit and lender.

Private loans can supplement federal borrowing but usually require credit checks and lack protections like income-driven repayment plans or forgiveness options. It is advisable to maximize federal loan options first before considering private loans.

- Federal loan caps ensure predictable borrowing limits.

- Fixed interest rates provide stability over variable private rates.

- Private loans may fill gaps but involve more risk.

What fast private student loan options exist and how do I compare lenders?

Private student loans offer fast funding when federal aid is insufficient. Unlike federal loans, private lenders such as Sallie Mae, Discover Student Loans, and Wells Fargo approve loans quickly, often within days, helping students cover urgent tuition or living costs. These lenders provide online applications and streamlined approval processes to accelerate access to funds.

When comparing private student loans, evaluate interest rates, repayment terms, fees, and borrower protections. Rates typically range from 3% to 14% and can be fixed or variable. Students with limited credit history may need a co-signer to secure better rates. It is also important to confirm if interest accrues during school or if repayments can be deferred.

Coverage varies by lender; some may finance 100% of the cost of attendance, including tuition, housing, and related expenses. Although private loans account for only about 7.7% of all student loans according to Education Data Initiative, they fill crucial gaps when federal aid doesn't cover all expenses.

- Obtain personalized interest rate quotes based on your credit profile.

- Check for origination fees or prepayment penalties.

- Review lender reputations and customer service ratings.

- Verify availability of income-driven repayment plans or forbearance options.

Opting for lenders that emphasize flexibility and transparency can help protect your financial future. Preparing documents in advance and carefully reviewing loan terms ensures timely access to funds without unforeseen costs.

How do repayment plans, deferment, and forbearance affect my monthly budget?

Repayment plans adjust your monthly student loan payments by spreading debt over a set period. Income-driven plans, for example, limit payments to a portion of your discretionary income, helping ease tight budgets but often increasing total interest paid due to longer repayment terms.

Deferment temporarily pauses payments during circumstances like school enrollment or unemployment. While this reduces immediate expenses, interest typically continues on unsubsidized loans, causing the balance to grow and future payments to rise.

Forbearance also delays payments, usually for financial hardship, but interest accrues on all loan types and compounds over time. It's a useful option in difficult situations but can significantly increase the amount owed.

The Education Data Initiative estimates that student income and savings cover only about 8% of total education costs, so most rely on loans or other funding sources. Choosing the right repayment approach balances current affordability with long-term costs. For example:

- A borrower with part-time work might select an income-driven plan for lower monthly payments.

- Someone expecting higher future income may opt for a standard plan to pay off debt faster.

Evaluate your financial outlook carefully before opting for deferment or forbearance, as these options postpone payments but increase debt over time. Combining sensible repayment plans with temporary relief can maintain financial stability without threatening future budgets.

Which loan forgiveness and discharge programs could reduce what I ultimately repay?

Several loan forgiveness programs can significantly lower your student loan repayment amounts. Public Service Loan Forgiveness (PSLF) offers full forgiveness after 10 years of qualifying payments while working full-time for government or nonprofit employers. This program is particularly beneficial for graduates entering public sector careers.

Income-driven repayment (IDR) plan forgiveness cancels remaining debt after 20 or 25 years, depending on the plan chosen. Options like Income-Based Repayment (IBR) and Pay As You Earn (PAYE) adjust monthly payments according to income and family size, easing monthly financial burdens. Any remaining balance after the repayment period is forgiven.

Discharge programs may eliminate loans in cases such as total and permanent disability, school closure, or false certification by the institution. For example, borrowers affected by a college closure before program completion may qualify for a closed school discharge.

Those experiencing financial hardship should explore these programs early to avoid default and wage loss. Many borrowers miss out due to misinformation or errors in their application process. The U.S. Department of Education provides helpful resources to verify eligibility and guide applications.

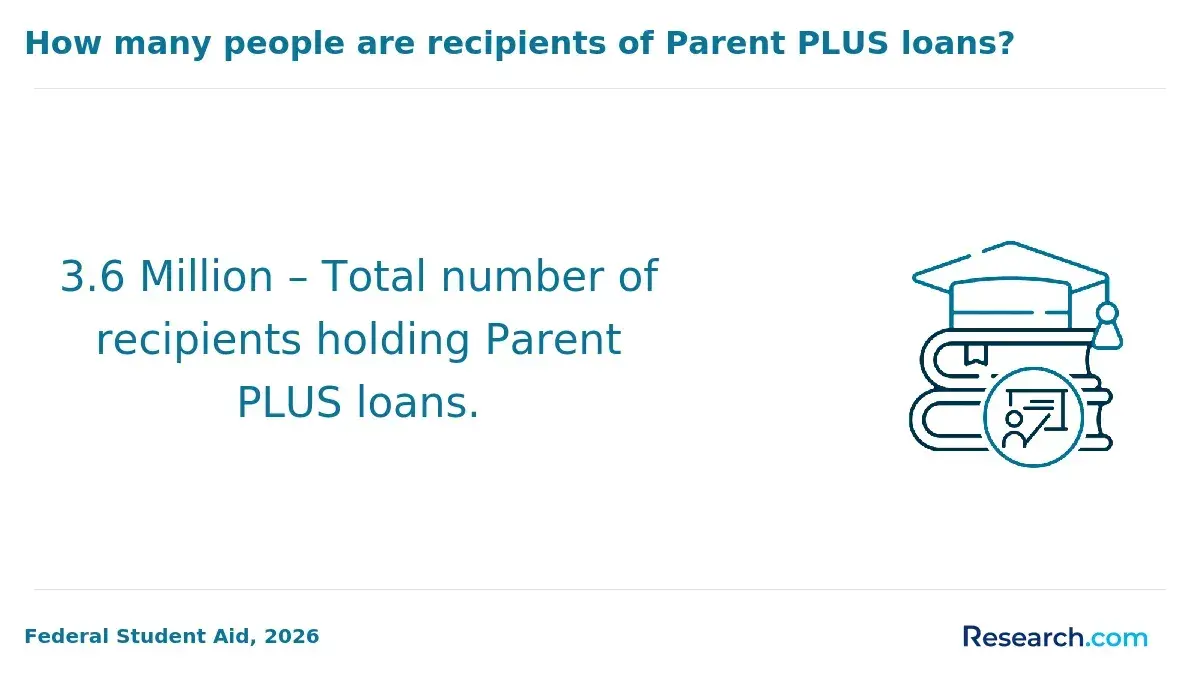

Parents who fund nearly half of college costs, as noted in Sallie Mae's 2025 study, should review Parent PLUS loan options. Strategies like consolidation or refinancing can impact forgiveness eligibility. Knowing which loans qualify for specific forgiveness programs is essential for maximizing debt relief.

How can parents and graduate students cover gaps when undergraduate aid isn't enough?

Parents typically cover a larger share of college expenses, paying about $34,461 annually, compared to $27,041 when students handle costs themselves, according to Education Data Initiative. To bridge these funding gaps when undergraduate aid is insufficient, targeted financial strategies are crucial.

Parent PLUS Loans allow parents to borrow up to the full cost of attendance minus other aid. These federal loans offer fixed interest rates and flexible repayment but require a credit check. Families with property may consider Home Equity Lines of Credit (HELOCs), which often have lower interest rates, though they carry the risk of foreclosure.

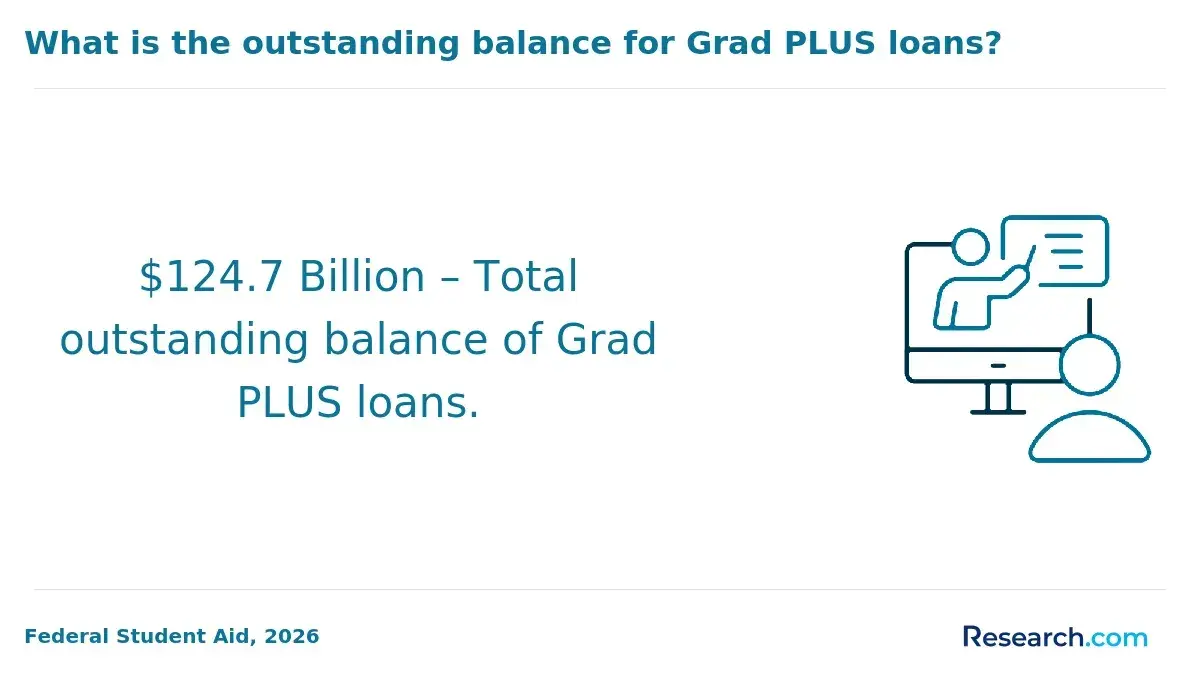

Graduate students can utilize Grad PLUS Loans to borrow up to the total cost of attendance with fixed rates. If federal options fall short, private graduate student loans are available but usually have higher interest rates and stricter credit requirements.

Additional strategies for both groups include:

- Part-time employment

- Employer tuition reimbursement programs

- Scholarships or grants targeted at graduate students or parents

- Budget adjustments and financial counseling to optimize available aid

Combining several of these methods proactively can lower reliance on high-interest debt and help cover remaining college costs beyond undergraduate aid.

Other Things You Should Know About

Yes, student loans typically cover more than just tuition fees. You can use loan funds for related educational expenses such as room and board, textbooks, supplies, transportation, and personal costs. Be sure to budget carefully, as borrowing beyond necessary costs increases debt without added benefits.

Federal student loans generally do not require a credit check for most borrowers, making them accessible regardless of credit history. However, some private student loans and PLUS loans do require a credit check, which can affect approval and interest rates. Exploring federal options first is advisable if you need money quickly.

If you miss payments, your loan can go into default, damaging your credit and increasing costs with fees and interest. Federal loans offer options like deferment, forbearance, and income-driven repayment plans to help manage payments and avoid default. Contact your loan servicer promptly to discuss your situation.

If you withdraw from school, you may need to return some or all of your student loan funds depending on when you leave. Loan eligibility is tied to your enrollment status, so withdrawing early can affect how much aid you keep or must repay. It's important to understand your school's refund and loan return policies before making decisions.