2026 Parent Student Loan Tax Benefits

Student Finance & Loan Expert

Many parents face confusion about managing student loan debt incurred for their children's education, especially when tax filings approach. Uncertainty about eligibility for deductions or credits can lead to missed opportunities for financial relief. Taxpayers may not realize which payments qualify or how income limits affect their benefits.

Navigating complex IRS rules adds to the challenge and can result in overpaying taxes. This article clarifies the key parent student loan tax benefits, explains eligibility criteria, and outlines actionable steps to optimize tax savings related to education debt.

- How do parent student loan tax benefits work for federal and private loans? Parent Borrower Taxes

- Which parent student loan interest is tax-deductible and how do you claim it? Tax-Deductible Interest

- Who qualifies to claim the student loan interest deduction on parent loans? Deduction Eligibility

- How do parent PLUS loans affect your overall tax situation and refund? Parent PLUS Taxes

- Can you get education tax credits if you also have parent student loans? Tax Credit Eligibility

- How do tax benefits differ between parent loans, student loans, and 529 plans? Tax Benefit Comparison

- What IRS forms and documentation are needed for parent student loan tax breaks? Tax Form Requirements

- How do loan refinancing and consolidation change parent loan tax advantages? Refinancing Tax Effects

- How should parents coordinate tax strategies with their student's filing status? Optimizing Tax Benefits

- What common mistakes cause parents to miss or lose student loan tax benefits? Common Filing Mistakes

How do parent student loan tax benefits work for federal and private loans?

Parent federal student loan tax benefits primarily focus on Parent PLUS loans, where borrowers can deduct up to $2,500 of interest paid annually as an adjustment to income. This deduction lowers taxable income and can decrease the overall tax burden. Eligibility phases out for single filers earning between $70,000 and $85,000, and joint filers with incomes from $145,000 to $175,000.

Private parent student loan tax deduction rules are more restrictive. Interest on private loans is only deductible if the loan meets IRS criteria as education debt, which is uncommon. Many private lenders do not report interest payments in a manner that supports tax deductions, limiting these benefits.

Parents and students together borrowed $102.6 billion in federal and private education loans during the academic year, with Parent PLUS loans representing 12% of the total. This highlights the importance of understanding Parent PLUS loan benefits and tax deductions.

For effective tax planning, consider the following:

- Keep detailed records of interest payments made on Parent PLUS loans.

- Check income limits yearly to maintain deduction eligibility.

- Consult a tax advisor regarding private loans, as deductions vary.

It's also useful to explore options for student loans for cost of living to better manage education expenses. Knowing which loans qualify for deductions can maximize tax savings amid rising education costs and loan burdens.

Which parent student loan interest is tax-deductible and how do you claim it?

Parent borrowers may qualify for a student loan interest tax deduction on interest paid for loans used solely to cover their child's higher education expenses. Eligible costs include tuition, fees, room and board, books, and other necessary supplies. This applies to federal Direct PLUS Loans and private parent loans that meet the IRS's definition of a qualified student loan.

The parent student loan interest tax deduction eligibility excludes loans taken out before the student's enrollment or those used for non-educational purposes. To claim this deduction, interest must have been paid during the tax year, and income limits must be met.

For example, the maximum deduction allowed for tax year 2025 is $2,500 and phases out for single filers with modified adjusted gross income (MAGI) above $70,000 and joint filers above $145,000.

Parents report the deductible interest on their federal income tax return using Form 1040 Schedule 1. Loan servicers typically provide Form 1098-E showing interest paid, but deduction is still possible without it if reliable payment records exist. Parents should keep in mind that refinancing student loans requires confirming that the new loan remains eligible for the deduction.

How to claim parent student loan interest on taxes involves ensuring the loan is not in default and that the parent is not claimed as a dependent on another's return. This above-the-line deduction reduces taxable income regardless of itemizing deductions. For those managing loan timelines, it's helpful to know about the student loan deadline for fall semester.

Who qualifies to claim the student loan interest deduction on parent loans?

Parents who have taken out Parent PLUS loans are eligible for the student loan interest deduction if they meet certain IRS requirements. This deduction applies only to interest paid on qualified student loans used to fund educational expenses for the parent's dependent child at a degree-granting institution.

Importantly, the taxpayer must be legally responsible for the loan; merely making payments on behalf of the child without co-signing or holding the loan does not qualify.

For example, a parent who holds a Parent PLUS loan in their name and pays the interest can claim the deduction. However, if a student takes out their own loan and the parent repays it, the parent cannot claim the deduction.

Income limits affect who qualifies for student loan interest tax deduction benefits. The phase-out starts at a modified adjusted gross income (MAGI) of $75,000 for single filers and $155,000 for married filing jointly, with no deduction allowed beyond $90,000 (single) and $185,000 (joint). The maximum deductible amount is $2,500 of interest paid annually.

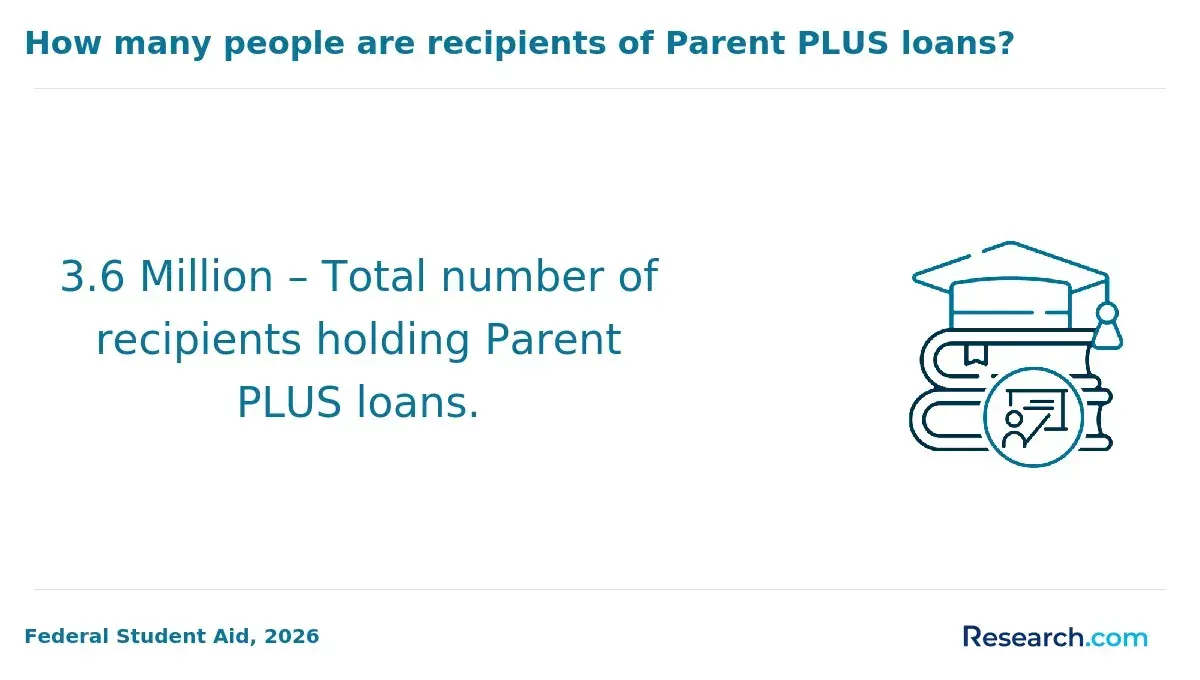

Parent PLUS loans account for a large share of federal student loan debt-about $112.2 billion held by 3.8 million borrowers compared to $104.0 billion in Grad PLUS loans by 1.8 million borrowers. For families exploring financing options or refinancing, it's useful to check student loan refinance deals that may offer better terms or savings.

How do parent PLUS loans affect your overall tax situation and refund? - PLUS tax impact

Parent PLUS loans impact your taxable income through the student loan interest deduction, but only the parent borrower can claim this benefit. You may deduct up to $2,500 of interest paid annually, which reduces your taxable income and can lower your federal tax bill depending on your tax bracket. This deduction is an adjustment to income, not a direct credit, so it decreases taxable income rather than the tax owed.

The effect on your tax refund varies based on the interest paid and overall income. For example, paying $1,500 in interest might reduce your taxable income by that amount, potentially increasing your refund. However, if your Modified Adjusted Gross Income exceeds $85,000 individually or $170,000 jointly, the deduction phases out, limiting its usefulness at higher income levels.

Parents should keep detailed records, as only interest payments qualify for the deduction, not principal repayments. Refinancing a parent PLUS loan into a private loan usually disqualifies you from claiming this federal tax benefit. Understanding the impact of parent PLUS loans on tax refund helps in planning your finances.

For borrowers exploring alternatives, consider looking into student loans from banks as another option for funding education.

In essence, parent PLUS loan tax deductions can reduce your federal tax burden if properly managed, with the parent borrower exclusively receiving the advantage.

Can you get education tax credits if you also have parent student loans?

You can claim education tax credits even if you have parent student loans, but the benefits differ from loan repayment rules. Credits like the American Opportunity Credit and Lifetime Learning Credit depend on qualified education expenses paid for an eligible student, not on who holds or repays the loan. Parent loans do not disqualify you from these credits; the essential factor is who actually pays tuition and fees during the tax year.

Education tax credits lower the amount of tax owed by up to $2,500 per student annually with the American Opportunity Credit. These credits relate to expenses paid, not to loan balances or payments.

In contrast, interest on parent student loans may be deductible up to $2,500 annually if you meet income limits and are legally responsible for the debt. This deduction reduces taxable income but does not affect education credits.

Employer-paid student loan repayment assistance is an increasingly common benefit. This assistance is tax-free up to $5,250 per year through 2025. Employer contributions toward your parent student loans within this limit are not taxable.

Key distinctions:

- Education tax credits require qualifying education expenses, not loan payments.

- Loan interest deductions apply if you're legally responsible for the debt and meet income requirements.

- Employer assistance can reduce loan burdens without tax penalties up to a set limit.

These differences can help you strategically optimize tax savings whether managing parent loans, paying tuition directly, or benefiting from employer support.

How do tax benefits differ between parent loans, student loans, and 529 plans?

Tax benefits differ notably among parent loans, student loans, and 529 plans, each offering unique advantages. Parent PLUS loans, unlike federal student loans taken by the student, do not qualify for the student loan interest deduction. Therefore, parents cannot deduct interest paid on these loans from their taxable income, which limits potential tax savings.

Student loans taken out by borrowers provide up to $2,500 of interest paid annually as a deduction, subject to income limits. This deduction reduces taxable income directly and offers a financial benefit during repayment.

529 plans stand out by focusing on tax-advantaged saving rather than borrowing. Contributions grow tax-free, and distributions used for qualified education expenses avoid federal income tax.

Under the SECURE Act, a 529 plan also allows up to $10,000 in student loan repayments per borrower, including siblings or parents after a beneficiary change-expanding flexibility and easing debt burdens without federal tax consequences.

- Parent loans lack interest deduction, increasing overall costs.

- Borrower-held student loans offer interest deductions up to $2,500 annually with income restrictions.

- 529 plans provide tax-free growth, withdrawals for education, and a $10,000 lifetime student loan repayment benefit per individual.

For families managing education finances, 529 plans are often the most tax-efficient tool to save or reduce debt, making them a key consideration alongside student and parent loans.

What IRS forms and documentation are needed for parent student loan tax breaks?

To claim parent student loan tax benefits, obtaining Form 1098-E, Student Loan Interest Statement, from your loan servicer is essential. This form reports the amount of interest paid on qualifying student loans during the tax year and is necessary to claim the student loan interest deduction accurately.

Parents usually report this deduction on IRS Form 1040, using Schedule 1, Additional Income and Adjustments to Income. Enter the deductible interest on line 20 of Schedule 1, which then transfers to the main form. If filing jointly, combine both spouses' loan interest statements without exceeding the $2,500 maximum deduction.

Documentation for loan discharge such as death or disability, if it occurred in 2025, remains tax-free. For discharges in 2026, federal law requires reviewing Form 1099-C, Cancellation of Debt, since taxable income might apply.

Other key documents that support your claim include loan origination statements and payment history records, crucial during an IRS audit. Ensure loans fit the IRS definition of student loans; private loans for non-educational purposes usually do not qualify. Verification from educational institutions, such as enrollment confirmation, can help validate qualification.

Parents must confirm the student hasn't claimed the deduction on the same interest, as multiple claims are disallowed by the IRS. Keeping thorough documentation is vital to secure and substantiate these tax benefits.

How do loan refinancing and consolidation change parent loan tax advantages?

Refinancing a parent student loan with a private lender often removes federal benefits, including the student loan interest deduction that lets borrowers reduce taxable income by up to $2,500 annually. This is because the loan is no longer classified as federal or parent PLUS, disqualifying it from the deduction and many federal protections.

Consolidation into a federal Direct Consolidation Loan may maintain tax advantages if the loan remains a federal parent PLUS loan. However, private refinancing usually results in losing these federal tax benefits. For example, lowering your interest rate through refinancing might save money but could reduce overall tax savings if the $2,500 deduction is lost.

Parents should also consider education tax credits when refinancing, as these credits are not directly affected by refinancing but impact overall tax planning:

- The American Opportunity Tax Credit can reduce a parent's tax bill by up to $2,500 per eligible student annually.

- The Lifetime Learning Credit offers up to $2,000 for 20% of the first $10,000 in qualified education expenses.

Practical steps include evaluating if refinancing savings outweigh lost deductions, confirming whether federal protections are forfeited, and coordinating loan interest deductions with education tax credits. Consulting tax professionals is advisable, given the complexity of loan types, lender policies, and eligibility rules.

How should parents coordinate tax strategies with their student's filing status?

Parents and students must carefully coordinate tax strategies when dealing with student loans and education-related tax benefits. When parents file separately from their student, they can retain control over student loan interest deductions and claim credits like the American Opportunity Credit if they support the student financially. If the student files independently as an adult, parents may lose eligibility for many education tax benefits.

Tax planning should focus on who claims education credits or deductions to maximize family savings. Students filing independently can claim up to $2,500 annually in student loan interest deductions, but parents should consider their own loan interest payments and tax brackets to avoid wasting deductions.

Proposed legislation under S.1298 aims to introduce a parent-specific allowance against income in the Student Aid Index. This could reduce assessed parental financial ability on federal aid applications and improve grant eligibility-adding a new dimension to tax and financial aid planning.

- The dependent status determines eligibility for various credits and deductions.

- Income levels impact phase-outs of education benefits, so parents in higher tax brackets may benefit if the student claims deductions.

- Loan interest deduction limits are $2,500 per filer, requiring coordination.

- Anticipating new Student Aid Index allowances can influence loan repayment and tax filing strategies.

Effective planning requires reviewing incomes, tax brackets, and financial aid implications together to optimize the family's overall benefit.

What common mistakes cause parents to miss or lose student loan tax benefits?

Many parents miss out on student loan tax benefits due to misunderstandings about eligibility and qualified expenses. Only interest on qualified loans up to $2,500 annually is deductible, and income limits may reduce or eliminate this benefit. A common error is assuming all student loan interest is deductible, which is not the case.

Parents often confuse who qualifies for the deduction. Only those legally obligated on the loan can claim the deduction, so parents who borrow for their children must meet this requirement. Incorrectly claiming dependents or misfiling can lead to IRS disallowance of benefits.

Maintaining accurate documentation is crucial. Records should clearly link loan payments to qualified education expenses. Payments made toward refinancing or private loans not used for education purposes are non-deductible.

Future policy changes may affect these benefits. Provisions like the tax-free status of death and disability discharges and the CARES Act employer student loan repayment exclusion sunset after 2025. This creates a possible "tax cliff" in 2026, making it essential to stay updated on legislation.

To avoid mistakes, verify loan types, track payments carefully, confirm taxpayer eligibility yearly, and monitor changes in laws impacting education-related tax benefits.

Other Things You Should Know About

Yes, unpaid parent student loans can negatively impact your credit score. Missed or late payments are reported to credit bureaus, which lowers your score and can make it harder to secure other types of credit in the future. Keeping up with payments and communicating with your lender if you face difficulties is crucial to protecting your credit.

Generally, only the borrower who is legally responsible for the loan can claim student loan interest deductions. If the student holds the loan, parents assisting with payments typically cannot claim those payments on their taxes. However, paying the loan can still indirectly benefit the family's overall financial health.

If a parent student loan is discharged or forgiven, the amount forgiven may be considered taxable income by the IRS, which could affect your tax bill. Recent changes and exceptions exist for certain forgiveness programs, so it's important to check current IRS rules or consult a tax professional regarding your specific situation.

Yes, your filing status can influence eligibility for student loan tax benefits. For example, married filing separately taxpayers often face restrictions that reduce or eliminate deductions. Most benefits phase out for higher-income taxpayers, so choosing the appropriate filing status is an important consideration.