2026 Best Parent Student Loans With Low Interest Rates

Student Finance & Loan Expert

Families facing the challenge of financing advanced education often struggle to find parent student loans with manageable interest rates. High interest can significantly increase the total repayment amount, creating financial strain long after graduation. Parents seeking to support their children's academic goals need options that balance affordability and repayment flexibility. Choosing the right loan is crucial to avoid excessive debt burdens while ensuring access to necessary funds. This article explores top parent student loan options featuring low interest rates, aiming to guide readers toward informed borrowing decisions that minimize financial risks and maximize educational opportunities.

- What are the best low-interest parent student loans? Parent Loans

- How do federal parent loans compare with private loans? Federal vs Private

- What credit requirements do parent loan lenders use? Credit Requirements

- How much can parents borrow for college? Borrowing Limits

- How do parent loan interest rates and fees work? Rates and Fees

- How do you apply for a parent student loan? Application Steps

- What repayment options do parent loans offer? Repayment Options

- Can parent loans be deferred or forborne? Deferment Options

- Can parent loans be refinanced or consolidated? Refinance or Consolidate

- What happens if a parent loan goes into default? Default Consequences

What are the best low-interest parent student loans?

The Federal Parent PLUS Loan remains a primary option for many families seeking affordable parent student loan options for US families, despite its fixed interest rate of 8.05% for current disbursements. Federal loans offer borrower protections like income-contingent repayment plans, but often come with higher rates compared to private loans.

Private parent student loans usually present competitive interest rates, ranging from around 4.5% to 10%, influenced by creditworthiness and lender terms. Credit unions and specialized lenders may offer fixed rates as low as 4.5%, which can substantially reduce the total interest paid. Parents with strong credit profiles may find private loans advantageous due to these lower rates and additional repayment flexibility not available in federal options.

When evaluating the best low interest parent student loans in the US, consider key factors:

- Interest rate type: fixed versus variable affects long-term payments and stability.

- Repayment flexibility: federal loans often allow deferment or income-driven plans, while private loan policies vary widely.

- Eligibility criteria and credit requirements: private loans generally need a strong credit history or cosigner guarantee.

Parents borrowed an estimated $11.7 billion through federal Parent PLUS loans in the 2023-24 academic year, highlighting the importance of informed choices.

Using online loan tools and prequalification offers can help uncover the lowest interest loans tailored to individual needs. For those figuring out how to pay for dental school or other educational expenses, resources like how to pay for dental school provide valuable guidance.

How do federal parent loans compare with private loans?

Federal Parent PLUS loans have a fixed interest rate of 8.94% for the 2025-26 academic year and include a 4.228% origination fee, according to Bankrate and NerdWallet. In contrast, private parent loans feature significantly lower fixed APRs starting around 2.59%, generally without any origination fees. This difference greatly impacts total borrowing costs, making a clear comparison of federal and private parent student loan options essential for families planning their finances.

Federal loans have notable benefits unavailable through most private lenders:

- Access without requiring strong credit history or cosigners

- Fixed interest rates that do not change during repayment

- Income-driven repayment plans and options for deferment or forbearance

- Eligibility for federal loan forgiveness programs

Private loans may appeal to borrowers with excellent credit as they can secure much lower interest rates. However, these loans tend to lack protections and flexible repayment options, sometimes requiring immediate payments or imposing penalties for early payoff. Borrowers should consider their credit profile and the federal parent loan interest rates versus private loans before deciding.

Parents with strong credit might reduce expenses by selecting private loans with rates near 2.59%. Others may prioritize federal loan stability despite higher costs. For those preparing to apply, checking the student loan deadline for fall semester is also crucial to meet all requirements in time.

What credit requirements do parent loan lenders use?

Parent loan lenders base credit requirements mainly on the borrower's credit history and financial situation. For federal Parent PLUS loans, the key criterion is the absence of an adverse credit history. This means no recent bankruptcies, defaults, foreclosures, significant delinquencies, or tax liens. Parents with an adverse credit history may still qualify by providing an endorser (cosigner) without adverse credit or by documenting extenuating circumstances.

Private parent loans generally enforce stricter credit criteria for parent student loans, requiring a strong credit score-often 650 or higher-stable income, and low debt-to-income ratios. Borrowers with weaker credit typically need a credit-worthy cosigner to secure favorable interest rates. Private lenders heavily weigh credit profiles to determine both loan approval and the terms offered, unlike federal loans.

The impact of creditworthiness extends to interest rates and repayment costs. Borrowing $40,000 for 10 years at the Parent PLUS rate of 8.94% versus a lower 5% rate can increase total repayment by about $8,800, according to the Consumer Financial Protection Bureau. Parents with limited or poor credit should consider improving their credit before applying or explore federal options allowing endorsers or special circumstance documentation.

Evaluating all loan terms, including credit requirements and rates, is vital for manageable educational funding. For those looking for additional ideas on how to cover education expenses, resources on how to pay for college as an adult can be helpful.

How much can parents borrow for college?

Parents can borrow up to the total cost of attendance (COA) for their child's college, minus any financial aid received. This borrowing limit varies by institution but generally includes tuition, fees, room, board, and other education expenses. Unlike other federal student loans, Parent PLUS loans do not have a fixed maximum amount, meaning the limit aligns with the documented COA after subtracting aid.

Typical borrowing limits used by parents tend to be more conservative. For example, the median Parent PLUS loan debt per parent borrower was $29,000 among bachelor's degree recipients, according to The College Board's "Trends in Student Aid 2024." This reflects that many families do not borrow up to the maximum allowed but instead aim for manageable debt levels. This is important when considering how much can parents borrow for college in the US in a realistic and financially responsible way.

Repayment terms and interest rates are crucial factors. Parent PLUS loans often carry higher interest rates than undergraduate federal loans and require repayment to begin immediately after disbursement, which can create heavy payment obligations if borrowing near the full COA. Parents should carefully calculate their needs, factoring in scholarships, grants, and other student loans that do not require a parental guarantee.

- Calculate the total cost of attendance at the chosen college.

- Subtract financial aid and other non-parent-guaranteed loans.

- Borrow only what is necessary to cover the remaining expenses.

- Prepare for loan repayment starting shortly after receiving funds.

For families with more than one child in college simultaneously, each child's borrowing limit applies independently, increasing total borrowing capacity but also repayment obligations. Those exploring financing options should compare different lenders, including student loan banks known for favorable terms to find the best approach for borrowing and repayment.

How do parent loan interest rates and fees work?

Parent loan interest rates vary significantly based on lender policies and the credit profile of the parent borrower or cosigner. Federal Parent PLUS loans carry fixed interest rates set by the government, currently about 8.05% for loans disbursed between July 2024 and June 2025. In contrast, private parent loans offer rates typically ranging from 4% to 12%, influenced by factors like credit score, income, and debt-to-income ratio. Origination fees, usually between 1% and 4% of the loan amount, may be deducted upfront or added to the principal balance.

Interest on these loans accrues daily and will capitalize if unpaid during deferment or forbearance, increasing the total repayment cost. For instance, interest on a $20,000 loan at 6% accrues about $3.29 per day. Variable-rate loans add uncertainty as rates can rise or fall, impacting the overall cost over time.

Approval rates for private parent loans substantially improve with a creditworthy cosigner. The MeasureOne Private Student Loan Report 2024 found that 92% of undergraduate private loans were approved when a strong cosigner or parent was involved, versus only 10% without one. This underscores the importance of strong credit when seeking favorable terms.

Parents should compare fees, loan types, and repayment features carefully. Many private lenders provide interest rate discounts for autopay enrollment or loyalty, which can lower borrowing costs. Evaluating these elements helps optimize financing decisions to support students effectively.

How do you apply for a parent student loan?

To apply for a parent student loan, gather important documents such as credit history, income verification, and the student's financial aid offer. Federal Parent PLUS loans require parents to complete the Free Application for Federal Student Aid (FAFSA) under the student's name, followed by a separate Parent PLUS loan application on the Federal Student Aid website. Approval involves a credit check and depends on no adverse credit history. If denied, parents may need an endorser or consider alternative loans.

Private parent loans, offered by banks and credit unions, have interest rates ranging roughly from 2.59% to 17.99% fixed APR. These loans also require credit checks and income verification. When evaluating lenders, compare interest rates, loan terms, fees, and repayment options carefully. Federal Parent PLUS loans offer a fixed 8.94% interest rate but generally less repayment flexibility than some private options.

Key steps to apply include:

- Completing the FAFSA to determine federal aid eligibility.

- Submitting a Parent PLUS loan application online for federal loans.

- Researching private lenders, gathering documents, and applying through their sites.

- Reviewing loan terms closely, especially interest rates and repayment conditions.

Parents facing credit difficulties should address them early and consider loan consolidation or refinancing after disbursement to improve terms and payments.

What repayment options do parent loans offer?

Parent student loans come with several repayment options tailored to different financial situations. The standard repayment plan lasts 10 years with fixed monthly payments, resulting in higher monthly costs but less interest paid overall. Extended repayment plans can stretch up to 25 years, lowering monthly payments but increasing total interest. For instance, extending a $30,000 parent loan at 7% interest from 10 to 20 years cuts monthly payments by about 32% but raises total interest by roughly 70%, according to the Consumer Financial Protection Bureau's loan calculator.

Graduated repayment plans start with lower payments that increase every two years, ideal for parents expecting their income to grow. Income-driven repayment options are rare for parent PLUS loans but can apply if the loans are consolidated; these adjust payments based on discretionary income and family size. Deferment or forbearance allows temporary suspension or reduction of payments during financial hardship, though interest continues accruing.

Choosing a repayment plan depends on cash flow needs and long-term cost. Parents with steady incomes who want to minimize interest typically choose the 10-year standard plan. Those needing smaller monthly payments might opt for extended or graduated plans but should expect higher total interest. Deferment and forbearance offer short-term relief but increase overall loan costs.

- Standard plan: fixed payments over 10 years

- Extended plan: up to 25 years with lower payments

- Graduated plan: increasing payments every two years

- Income-driven plan: adjusted by income if consolidated

- Deferment/forbearance: temporary payment relief with accruing interest

These options help parents manage debt effectively while supporting their student's education goals.

Can parent loans be deferred or forborne?

Parent PLUS loans can be deferred or placed in forbearance, but these options differ from typical student loans. Direct PLUS loans allow deferment for specific situations such as returning to school at least half-time, unemployment, or economic hardship. Unlike subsidized loans, Parent PLUS loans are unsubsidized, so interest continues to accrue during deferment, increasing the overall cost.

Forbearance is available for temporary financial difficulties that don't qualify for deferment. It allows payment pauses or reductions, but interest still accrues and adds to the principal balance, potentially increasing the total repayment amount significantly.

Borrowers over 55 years old make up a large portion of Parent PLUS loan holders. Around 3.5 million in this age group carry an average balance of $38,000, many still paying as they approach or enter retirement. This makes understanding repayment options crucial for managing long-term debt.

Effective repayment management includes:

- Contacting the loan servicer to explore specific deferment and forbearance options based on personal circumstances.

- Considering income-driven repayment plans, available after consolidation of Parent PLUS loans.

- Evaluating the impact of accruing interest during non-payment periods to prevent ballooning loan balances.

Can parent loans be refinanced or consolidated?

Parent PLUS loans can be consolidated or refinanced, but the options differ significantly. Federal Parent PLUS loans qualify for federal Direct Consolidation Loans, which combine multiple federal loans into one with a fixed interest rate based on the weighted average of the original loans. While consolidation simplifies repayment, it does not reduce interest rates.

Refinancing, on the other hand, allows borrowers to transfer federal Parent PLUS loans into private loans, often securing lower interest rates if they have good credit. According to Credible's Student Loan Refinancing Report, those who refinanced private loans saved an average of 2.15 percentage points on their interest rate and about $250 monthly on payments.

Refinancing offers potential savings but comes with trade-offs:

- Federal protections like income-driven repayment plans and loan forgiveness programs are lost upon refinancing into private loans.

- Private lenders require credit approval, which may be difficult for some parents to obtain.

- Loan terms vary widely: shorter terms decrease total interest but raise monthly payments; longer terms do the opposite.

Weighing the benefits of lower rates against losing federal borrower protections is essential. Reviewing private refinancing offers carefully and using reliable calculators or consulting a financial advisor can help determine whether refinancing or consolidation aligns best with one's financial goals.

What happens if a parent loan goes into default?

Default on federal Parent PLUS loans typically occurs after 270 days of missed payments, triggering serious consequences. At this point, the full loan balance becomes immediately payable, and the government may pursue aggressive collections without additional warning.

Consequences of default include wage garnishment of up to 15% of disposable income, tax refund offsets, and even Social Security benefit seizure. These measures can destabilize a family's finances. Additionally, a defaulted loan damages the parent's credit score, limiting access to new credit, housing, or employment opportunities.

Default also means losing access to deferment, forbearance, and income-driven repayment options, which help manage payments during financial hardship. Rehabilitation is possible by making nine consecutive on-time payments within ten months, restoring the loan to good standing.

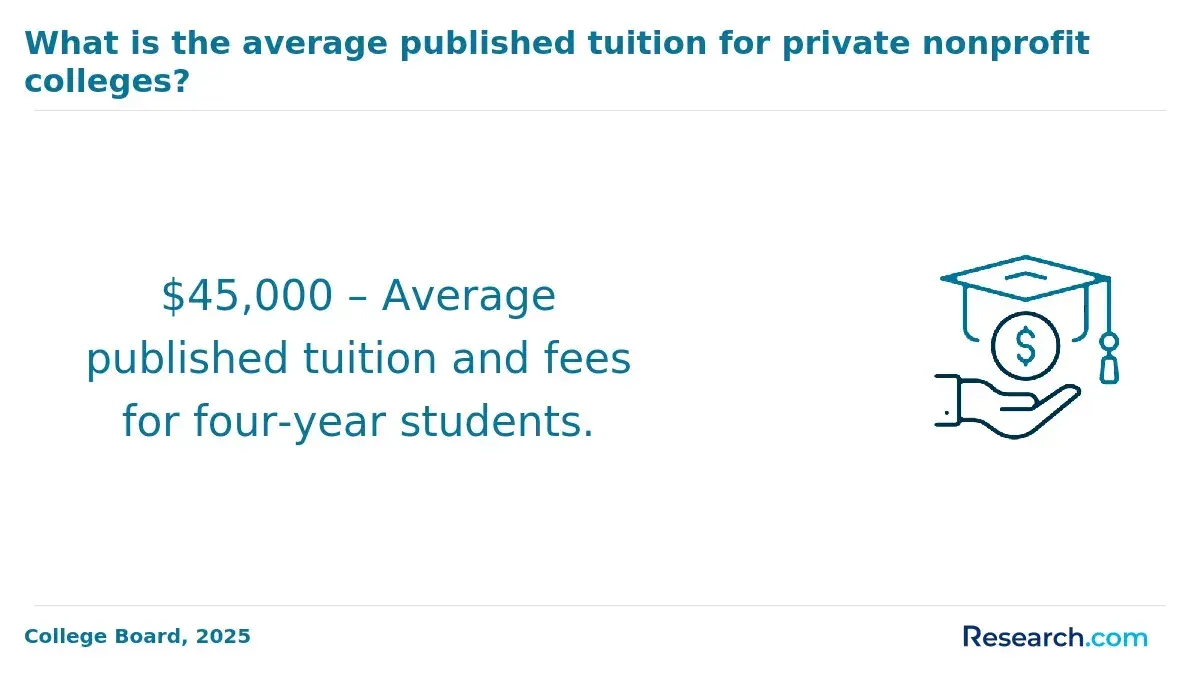

Parents should explore alternative strategies to minimize borrowing. For instance, average in-state public college costs after grants were about $3,900, while private nonprofit colleges averaged $33,200-nearly a $30,000 difference. Choosing more affordable schools or maximizing scholarships can reduce reliance on Parent PLUS loans.

Parents facing repayment difficulties are advised to contact their loan servicer promptly to discuss options. Ignoring payments accelerates default and intensifies long-term financial harm.

Other Things You Should Know About

Yes, parent student loans can impact a parent's credit score. Payments reported on time can help build credit, while missed or late payments can cause significant damage. Lenders also consider credit history when approving parent loans, so managing these loans responsibly is important for maintaining good credit.

Parents may be eligible to deduct interest paid on student loans, including some parent student loans, up to certain limits on their tax returns. However, the deduction phases out at higher income levels. It's important to consult IRS guidelines or a tax professional to understand eligibility and maximize tax benefits.

If the student withdraws or does not finish college, the parent is still responsible for repaying the loan in full. Parent loans are legally the borrower's obligation, regardless of the student's enrollment status or graduation. Parents should be prepared for repayment even if the student's education plans change.

Generally, cosigners are not required for parent student loans because the parent borrower is the primary applicant. However, private lenders might request a cosigner or additional credit support if the parent's credit does not meet their standards. Federal parent loans do not allow cosigners since they rely on the parent's credit standing alone.