2026 How to Find a Student Loan Cosigner

Student Finance & Loan Expert

Many prospective graduate students struggle to secure loans without a strong credit history or sufficient income. Lenders often require a cosigner to reduce their risk, but finding someone to co-sign can be challenging, especially for those transitioning careers or pursuing advanced education later in life. This obstacle can delay or prevent access to necessary funding. Understanding how to identify, approach, and secure a reliable cosigner is crucial for overcoming this barrier. This article explores practical strategies for finding a student loan cosigner and offers guidance to help borrowers navigate this complex process with confidence.

- How does a cosigner work on a student loan and why might you need one? Cosigner basics

- Who can be a student loan cosigner and what are the eligibility requirements? Cosigner eligibility

- How can you ask someone to cosign your student loan without harming the relationship? Asking a cosigner

- What steps should you take before looking for a cosigner for private student loans? Before cosigner

- How do you evaluate if a potential cosigner's credit and income are strong enough? Evaluating cosigner

- What risks and responsibilities does a cosigner take on for your student loan? Cosigner risks

- How can a cosigner improve your approval odds, interest rate, and loan terms? Cosigner benefits

- What options do you have if you can't find a cosigner for a student loan? No cosigner options

- How do cosigner release and refinancing work if you want to remove a cosigner? Removing cosigner

- How should you compare lenders that require a cosigner versus those that don't? Comparing lenders

How does a cosigner work on a student loan and why might you need one?

A cosigner on a student loan agrees to share legal responsibility if the borrower cannot make payments. Their credit history and income are evaluated during loan approval, often helping the borrower qualify and secure better interest rates. This is particularly important for those who lack sufficient credit history or income to qualify independently. Having a cosigner can offer several benefits of having a cosigner for student loans, including access to lower rates and improved loan terms.

Nearly 40% of Americans would be denied a private student loan based solely on credit, and between 61% and 100% of loans from major private lenders require a cosigner, according to the National Association of Student Financial Aid Administrators. This illustrates how critical cosigners can be in gaining loan approval in the private market.

Reasons to seek a cosigner might include:

- Limited or no credit history, often common among recent high school graduates.

- Low or unstable income that does not meet lender standards.

- A high debt-to-income ratio causing concerns about repayment ability.

Students frequently ask a parent or guardian to cosign, especially if they have no credit record. Professionals returning to school may also need a cosigner if their income doesn't justify the loan amount. Cosigners must understand student loan cosigner responsibilities, as missed payments affect both parties' credit scores and expose them to financial risk. Choosing a reliable cosigner is crucial.

For those exploring options, including graduate loans for dental school, detailed information is available at graduate loans for dental school.

Who can be a student loan cosigner and what are the eligibility requirements?

A student loan cosigner must be a creditworthy individual willing to share responsibility for repaying the loan if the primary borrower fails to do so. Typically, cosigners are parents, relatives, or close friends who meet specific eligibility standards, including a strong credit history (usually a credit score above 650) and proof of stable income to cover loan payments if needed. Being a U.S. citizen or permanent resident and at least 18 years old are also common requirements.

The eligibility requirements for student loan cosigning in the US often include limits on the number of loans a person can cosign. For instance, parents cosigning PLUS loans must remain within federal lending limits. Private lenders tend to impose stricter credit standards, so cosigners play a key role in reducing lender risk and securing better interest rates for borrowers with limited credit history.

- A strong credit history and reliable debt repayment behavior

- Proof of stable income sufficient to cover payments

- Legal U.S. residency or citizenship

- Being at least 18 years old

Choosing a cosigner requires trust, as they are equally responsible for the total debt, which averages $43,333 per borrower including private loans. Missed payments negatively impact both borrower and cosigner credit scores, affecting future financial options. Those without eligible cosigners might explore credit unions or lenders offering no-cosigner loans, often with higher rates. For advice on alternatives, check how to pay for college without parents.

How can you ask someone to cosign your student loan without harming the relationship?

Approach requesting a student loan cosigner with transparency and respect to preserve the relationship. Clearly explain why you need a cosigner by detailing your credit situation and financial plans. Emphasize your commitment to timely payments and responsible borrowing, which helps reduce the cosigner's risk perception. This approach is essential when learning how to ask someone to cosign a student loan without damaging trust.

Provide detailed information about loan terms, including interest rates, repayment schedules, and consequences of default. Since January 2025, 3.6 million federal student loan borrowers have entered default, contributing to 8.8 million defaults overall (ProtectBorrowers.org Default Crisis Fact Sheet, January 2026). Explaining safeguards you will use to avoid default can build reassurance.

Encourage open dialogue so the potential cosigner can ask questions and share concerns. Discuss various loan options or alternative support methods, such as smaller loans or partial cosigning, to offer flexibility. This is one of several valuable tips for maintaining a good relationship when requesting a student loan cosigner.

Show your repayment plan by sharing a budget or proof of income. For instance, mention if you have a part-time job or expect a scholarship to highlight financial preparedness. Be sure to explore options like best parent student loans as part of your research.

Respect their decision without applying pressure or guilt, and if they decline, thank them sincerely and explore other paths to protect trust. Maintaining honesty and ongoing communication, especially if financial difficulties arise, safeguards your relationship.

What steps should you take before looking for a cosigner for private student loans?

Before seeking a cosigner for private student loans, evaluate your credit and financial situation thoroughly. Lenders often require a cosigner because students typically lack sufficient credit history or steady income. Between 61% and 100% of private student loans reviewed in a 2026 study by the National Association of Student Financial Aid Administrators required a cosigner, underscoring its importance in loan approval.

Start by obtaining your credit report to check your credit score, especially since a score below 660 generally reduces your chances of qualifying independently for private loans. Also, identify any errors or negative marks. Assess your income, employment status, and existing debt to understand your repayment capability. This financial checkup is essential preparation before finding a cosigner.

Research individual lender requirements carefully, as some offer loans without a cosigner if you have substantial income or collateral. Prioritize federal student loans first since they do not require cosigners and provide stronger borrower protections. Only consider private loans after maximizing federal aid options.

Prepare a list of potential cosigners-typically parents, relatives, or close friends with strong credit (usually a FICO score above 700) and stable income. Clearly discuss the responsibilities, including potential risks if payments are missed, to ensure transparency and avoid misunderstandings.

Gather essential documents such as proof of income, tax returns, and identification to streamline the application process and reassure cosigners. This organized approach supports a smoother journey toward funding with an informed cosigner. After securing the loan, consider options on how to refinance student loans to improve terms in the future.

How do you evaluate if a potential cosigner's credit and income are strong enough?

Verifying a cosigner's credit and income is crucial for student loan approval. Lenders typically prefer a credit score above 700, but require at least 650. Pay close attention to repayment history, checking for late payments, defaults, or bankruptcies, as these issues reduce the likelihood of approval.

Assess the cosigner's debt-to-income (DTI) ratio by dividing their total monthly debt payments by gross monthly income. A DTI under 40% signals they can manage extra loan payments without excessive risk. For instance, a cosigner with $5,000 monthly income and $1,500 debt payments has a 30% DTI, which is favorable.

Stable income documentation such as pay stubs or tax returns over two years strengthens their profile. If self-employed or with irregular income, additional paperwork may be needed. Evaluating existing financial obligations is also important, including outstanding loans, credit card balances, savings, or assets that offer financial stability.

Private student lenders rarely approve cosigner release requests; about 90% are denied according to a Consumer Bureau review cited in 2026, underscoring the long-term nature of cosigning. It's important to have direct conversations about these responsibilities to ensure the cosigner is fully informed.

What risks and responsibilities does a cosigner take on for your student loan?

Cosigners on student loans take on a serious financial and legal commitment. They are responsible for repaying the loan if the primary borrower cannot, with their credit directly affected by the loan's payment history. Late or missed payments harm the cosigner's credit just as much as the borrower's, and default can lead to collections targeting the cosigner.

While the loan is solely for the student, cosigners share full responsibility for the debt, including principal and interest. Private undergraduate loan rates can vary widely, sometimes exceeding 17% APR, so a cosigner with strong credit can help secure lower rates and save on interest over time. On the other hand, any missed payments increase risk and financial strain for the cosigner.

Cosigners are often parents or relatives helping students with little credit history, but they can also be friends or partners. Important considerations include:

- Understanding that liability for the debt is equal.

- Being prepared to cover payments if the student cannot pay.

- Regularly monitoring loan status.

- Knowing how the loan impacts their credit and borrowing power.

Cosigning impacts the cosigner's ability to acquire new credit, as lenders view the cosigned loan as their obligation. Potential cosigners should carefully assess their financial situation and risks before committing.

How can a cosigner improve your approval odds, interest rate, and loan terms?

A cosigner can greatly enhance your chances of getting approved for a student loan by offering their stronger credit history and income as a guarantee. This reduces the lender's risk and is particularly crucial for private student loans, where cosigners are often essential. While federal student loans rarely require cosigners, private loans-totaling about $150 to $200 billion-commonly rely on them to help borrowers qualify.

Interest rates on student loans usually depend on the borrower's creditworthiness. By adding a cosigner with excellent credit, borrowers may secure interest rates several points lower, sometimes dropping a 7% rate below 5%. This can lead to significant savings over time and lower monthly payments, making the loan more affordable.

Additionally, cosigners can influence loan terms positively, allowing access to higher loan amounts, extended repayment periods, and more flexible options. They can also help borrowers without steady income or sufficient credit qualify for loans that might otherwise be denied.

It's important to remember that cosigners share full responsibility for repayment. Missed payments can harm the cosigner's credit score and borrowing ability, so choosing a reliable cosigner is vital.

What options do you have if you can't find a cosigner for a student loan?

Federal student loans are a primary option if a cosigner is unavailable, offering Direct Subsidized and Unsubsidized Loans to many undergraduates and graduate students based on financial need or enrollment. These loans generally provide more favorable terms without needing a cosigner.

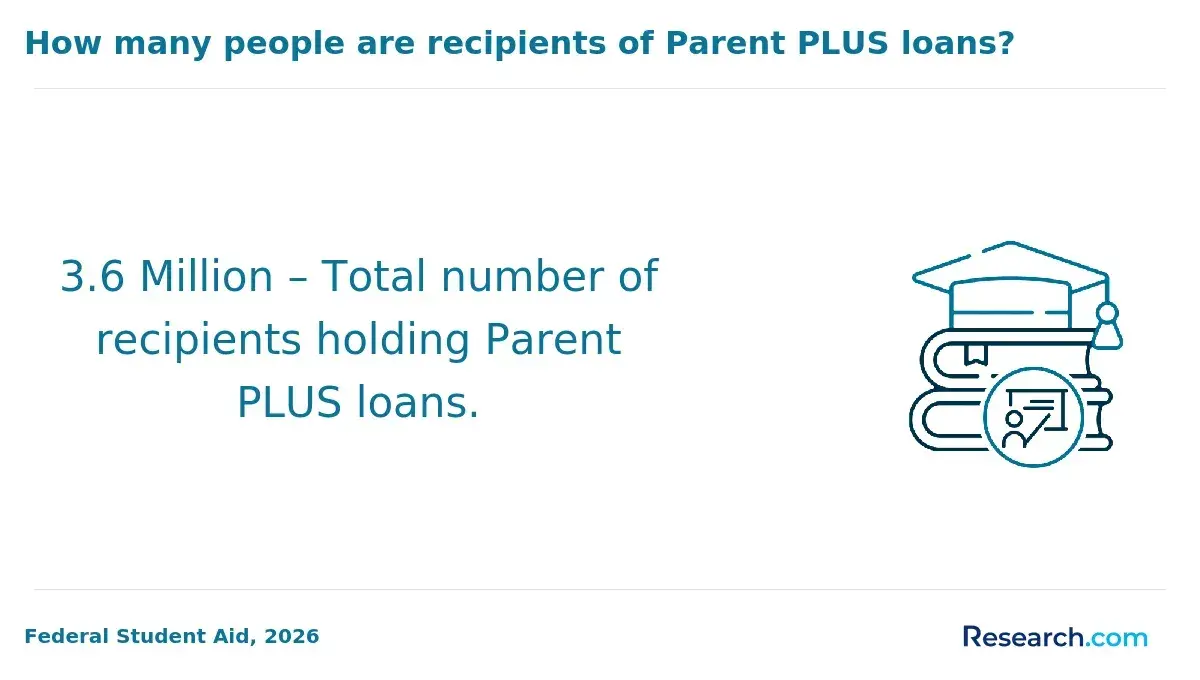

Parent PLUS Loans allow parents to borrow on behalf of their children, covering gaps left by federal loans. Though these loans carry higher borrowing limits, parents undertake the legal responsibility. Currently, Parent PLUS federal loans amount to approximately $116.0 billion held by 3.6 million borrowers, highlighting the significant role parents play in financing education alongside private loans.

Some private lenders offer loans without requiring a cosigner, but these generally demand strong credit and come with higher interest rates. Building credit over time can improve chances of qualifying for these loans.

Other cost-reduction strategies include scholarships, grants, work-study programs, and employer tuition assistance plans, all of which don't require repayment or cosigners.

Community lending programs or credit unions may provide flexible loan conditions and lower rates without cosigners. Additionally, some schools offer institutional loans or payment plans for students without cosigners, albeit with limited availability.

How do cosigner release and refinancing work if you want to remove a cosigner?

Cosigner release permits borrowers to remove a cosigner from a private student loan after meeting specific lender requirements. Typically, these include on-time payments for 12 to 24 months and demonstrating improved creditworthiness. Note that federal loans do not allow cosigner releases, as cosigners cannot be removed from these loans. Another route to remove a cosigner is through refinancing, which replaces the original loan with a new one solely in the borrower's name. Refinancing depends on the borrower's credit score, income, and debt-to-income ratio, and can offer better interest rates or terms if qualified.

Refinancing eligibility varies, and failing to meet these financial criteria means cosigner removal won't be possible via this option. Borrowers must balance the risks, since cosigners remain fully liable if a borrower defaults. This was highlighted by the Trump administration's 2026 move to restart wage garnishment for defaulted federal borrowers, showing how quickly serious collection actions can impact any legally responsible party.

Key points to consider include:

- Checking lender criteria for cosigner release

- Maintaining a strong credit profile to qualify for refinancing

- Remembering that federal loans do not allow cosigner removal

- Understanding cosigner removal is permanent and transfers full debt responsibility to the borrower

Consult directly with lenders and use refinancing calculators or credit counseling services to assess eligibility and timing for safely removing a cosigner.

How should you compare lenders that require a cosigner versus those that don't?

Lenders requiring a cosigner generally offer lower interest rates because the cosigner reduces the lender's risk. For instance, private loans with a cosigner may start around 4%, while loans without one often begin near 7%. However, loans without cosigners target borrowers with strong credit or stable income, making approval more challenging for those with limited or poor credit.

A cosigner takes on legal responsibility and affects their credit score if payments are missed. This adds risk for both the borrower and the cosigner. Federal student loans, which do not require cosigners, will introduce a new income-driven repayment plan starting July 2026. This plan could benefit approximately 42.8 million borrowers by capping payments relative to income, reducing the risk of default, according to GetOutOfDebt.org. Private loans backed by cosigners tend to lack such flexible repayment options.

- Compare total borrowing costs including fees to see the true price difference between loan types.

- Ensure the cosigner understands their financial commitment since missed payments affect both parties.

- Consider the long-term impact; federal loans with income-driven plans may offer greater repayment flexibility without needing a cosigner.

Balancing affordability, ease of approval, repayment options, and cosigner risks helps in choosing the best loan type for individual financial situations.

Other Things You Should Know About

Yes, a cosigner's credit can be affected if the student misses payments or defaults on the loan. Late payments or defaults will appear on both the student's and cosigner's credit reports, potentially lowering their credit scores and making it harder for either to obtain credit in the future.

Most private student loans only allow one cosigner. However, some lenders may permit multiple cosigners, but this is uncommon. It is important to check the specific lender's policies before applying.

If a cosigner dies or can no longer make payments, the borrower remains responsible for the full loan amount. The lender will typically seek repayment from the borrower, and the loan will not be automatically discharged due to the cosigner's death or incapacity.

Generally, loan terms are set at approval and cannot be changed by adding a cosigner afterward. To benefit from a cosigner's credit after approval, borrowers may need to refinance the loan with the cosigner included to potentially secure better interest rates or terms.