2026 Best Student Loans for Returning to College

Student Finance & Loan Expert

Many returning students face challenges financing their education after time away from school. Budget constraints, changing life circumstances, and unfamiliarity with current loan options create barriers to enrolling or continuing studies. Traditional student loans may no longer fit their unique financial needs or goals.

Navigating interest rates, repayment plans, and eligibility criteria adds complexity to deciding which loan best supports academic and career advancement. This article examines the top student loan options tailored for returning college students and working professionals seeking further education, providing clear, reliable guidance to help secure the most suitable financial aid.

- What are the best student loan options for adults returning to college? Best loans

- How do federal and private student loans compare for returning students? Federal vs private

- How can returning students qualify and apply for federal student loans? Federal eligibility

- What borrowing limits and interest rates apply when you go back to school? Limits & rates

- Which federal loan programs work best for part-time, online, or career-changer students? Best federal options

- How do income-driven repayment plans work when you return to college later in life? IDR plans

- What loan forgiveness and discharge options can returning students realistically use? Forgiveness options

- How do parent, PLUS, and graduate loans fit into funding a return to college? Parent & grad loans

- When should returning borrowers use refinancing or consolidation to manage old and new loans? Refinance vs consolidate

- How do deferment, forbearance, and default impact returning students' credit and future aid? Hardship & default

What are the best student loan options for adults returning to college?

Federal student loans are often the best student loan options for adults returning to college, offering fixed interest rates around 5.5% for undergraduates through Direct Subsidized and Unsubsidized Loans.

These loans provide key benefits such as deferred payments while enrolled at least half-time and income-driven repayment plans like REPAYE or PAYE, which cap monthly payments based on discretionary income to ease financial pressure.

Private student loans may supplement federal aid but tend to have higher interest rates from 7% to 13% and fewer borrower protections. Adults with strong credit or a creditworthy co-signer might secure better terms.

Credit unions and banks that offer specialized loans targeted at non-traditional students can also provide more tailored repayment schedules, enhancing access to affordable student loans for adult learners.

Employer tuition assistance programs can work alongside federal loans to significantly reduce overall debt. Refinancing options after completing a degree may lower interest costs if the borrower's financial situation improves. For tailored guidance on specific fields, consider exploring resources like the best loans for dental students.

This approach is particularly valuable since adults earning a bachelor's degree after age 25 typically experience median annual earnings 54% higher than those with only a high school diploma, highlighting the importance of affordable and manageable loan options for adult learners returning to college.

How do federal and private student loans compare for returning students?

Federal and private student loans differ significantly in cost, borrower protections, and qualification criteria, especially for returning students. For example, federal Direct Loans feature fixed interest rates of 6.39% for undergraduates and 7.94% for graduate borrowers.

In contrast, private loans offer a broader range from 4.42% up to 15.90%, based on data from Federal Student Aid and Credible. This variability means private loans can sometimes be cheaper but may also carry higher maximum rates.

Borrowers seeking the best student loan options for returning adult learners should consider that federal loans include benefits like income-driven repayment plans, deferment, and loan forgiveness programs. Private lenders often require strong credit or a co-signer and provide less flexible repayment options, making federal loans safer for those with uncertain incomes.

Returning students with strong credit profiles may find private loans appealing due to potentially lower rates near 4.42%. However, without good credit, interest rates can surpass federal loans. Federal loans generally do not require credit checks for most undergraduates, offering greater accessibility.

Private loans might be suitable for students who have reached federal loan limits or need additional funding. However, they lack federal borrower protections, increasing risks during financial difficulties. Students should weigh interest rates, borrowing limits, repayment flexibility, and eligibility criteria carefully.

Those interested in student loans with low credit score should evaluate all options before borrowing.

How can returning students qualify and apply for federal student loans?

Returning students seeking federal student loans can qualify by completing the Free Application for Federal Student Aid (FAFSA). This essential form evaluates financial need to determine eligibility for Direct Subsidized and Unsubsidized Loans. For returning undergraduates who qualify as independent students, total Direct Loans can reach up to $57,500, with a maximum of $23,000 being subsidized, according to federal loan limits.

To apply for federal student aid for returning college students, several steps must be followed:

- Submit the FAFSA for the applicable academic year and renew annually if necessary.

- Enroll at least half-time in an eligible institution.

- Maintain satisfactory academic progress as defined by the school.

Independent status impacts loan limits since parental income is not considered. Examples include being over 24 years old, married, a veteran, or having dependents other than a spouse, which often leads to higher borrowing limits.

Returning students should also review their loan balances carefully because federal loan limits are cumulative across all borrowing periods.

Direct Subsidized Loans are awarded based on financial need with stricter caps, while Unsubsidized Loans do not require demonstrated need but accrue interest during enrollment. After FAFSA approval, students receive a Student Aid Report (SAR) detailing their eligibility.

Schools then provide financial aid packages, including loan offers that require acceptance through a Master Promissory Note and entrance counseling explaining borrower responsibilities. For insight into borrowing options, students may explore the best MBA student loans.

What borrowing limits and interest rates apply when you go back to school?

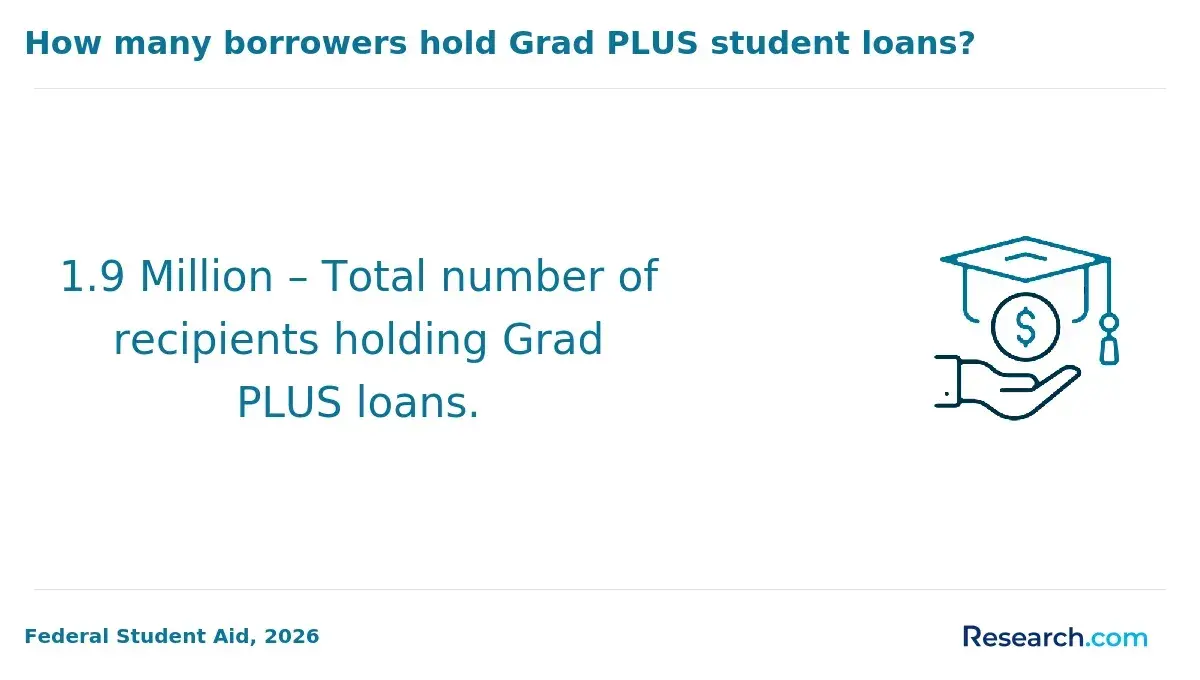

Borrowers returning to college in 2026 must navigate updated borrowing limits and interest rates on student loans for returning college students. Graduate students face a new lifetime Direct Loan borrowing cap of $100,000 starting July 1, 2026, as Grad PLUS loans are phased out.

This consolidates all graduate borrowing under one cap, simplifying the process but requiring careful tracking to avoid exceeding limits. Undergraduate students still follow standard annual and aggregate loan limits, usually up to $57,500 in total federal loans, based on their dependency status.

Interest rates vary by loan type and disbursement date but are generally fixed annually by the U.S. Department of Education. For example, Direct Subsidized and Unsubsidized Loans for undergraduates disbursed mid-2026 are expected to have rates near 5%, while graduate Direct Unsubsidized Loans have rates around 6.5%. These fixed rates affect the total cost of borrowing throughout the loan term.

Loan eligibility also depends on enrollment status-part-time students may qualify for smaller amounts. Loan disbursements correspond to cost of attendance minus any financial aid received, not discretionary choices, reflecting careful regulation of maximum loan amounts for returning students in the United States.

Those who have borrowed heavily or used Grad PLUS loans before should plan carefully, as the new caps impact repayment and consolidation options. When managing existing debt, explore options like student loan refinancing to potentially lower interest rates or monthly payments.

Which federal loan programs work best for part-time, online, or career-changer students?

Federal loan programs that support part-time, online, and career-changing students include Direct Subsidized and Unsubsidized Loans, along with the Federal PLUS Loan for parents and graduate students.

Direct Subsidized Loans offer interest-free periods while enrolled at least half-time, which benefits students with varied course loads. Direct Unsubsidized Loans don't require proof of financial need, making them accessible to many nontraditional students.

The Federal PLUS Loan is especially helpful for career changers or part-time students facing borrowing limits or income restrictions. These loans require a credit check and often a co-signer, which can impact approval chances. Ascent's 2025 data shows approval rates over 90% for applicants with a creditworthy co-signer, compared to much lower rates for independent borrowers, according to NerdWallet's 2026 lender analysis.

Students enrolled less than half-time should consider loans that don't enforce a half-time enrollment minimum. While Direct Loans require half-time status, private loans with co-signers might be necessary for those taking fewer credits.

Loan deferment and income-driven repayment plans within federal programs can accommodate uncertain employment periods for career changers returning for certificates or associate degrees. Applying for FAFSA early ensures access to these federal options, regardless of enrollment format or schedule.

How do income-driven repayment plans work when you return to college later in life?

Income-driven repayment (IDR) plans adjust student loan payments based on your income and family size, often setting payments between 10% and 20% of discretionary income.

These plans typically offer repayment terms of 20 to 25 years, after which remaining balances may be forgiven. Annual recertification of income and family size is required; missing this step increases payments to standard amounts.

For those returning to school or experiencing drops in income, IDR payments can decrease significantly, sometimes to $0, providing vital financial relief during studies. After graduation, if your income rises, payments will adjust upward accordingly.

IDR plans are especially valuable for professionals entering high-demand fields such as registered nursing, software development, and medical/health services management. These sectors are expected to add over 600,000 jobs with median salaries ranging from $86,000 to $136,000, helping graduates manage debt while transitioning to higher earnings.

Common IDR options include Revised Pay As You Earn (REPAYE), Pay As You Earn (PAYE), Income-Based Repayment (IBR), and Income-Contingent Repayment (ICR). Each has specific eligibility criteria and payment calculations to consider.

Using IDR supports manageable payments aligned with income changes, reduces default risk, and promotes long-term financial health, crucial for balancing education and career growth.

What loan forgiveness and discharge options can returning students realistically use?

Several student loan forgiveness and discharge options are available for federal student loans, particularly benefiting returning students. Income-Driven Repayment (IDR) plans like the SAVE plan provide relief by adjusting monthly payments according to income.

Over 8 million borrowers enrolled in SAVE, with about 4 million qualifying for $0 monthly payments, highlighting its accessibility. After 20 or 25 years of qualifying payments under IDR, remaining loan balances may be forgiven.

Public Service Loan Forgiveness (PSLF) fully forgives loans after 120 qualifying monthly payments for borrowers working full-time in eligible government or nonprofit roles. This is ideal for students pursuing careers in education, healthcare, or social services.

Loan discharge options apply in specific situations, such as Total and Permanent Disability (TPD) discharge, closed school discharge when an institution shuts down during enrollment or shortly after withdrawal, and borrower defense discharge if the school violated laws or misled students.

Eligibility requires federal loans, as private loans rarely offer forgiveness. Success in these programs involves:

- Working full-time in qualifying public service jobs.

- Enrolling and maintaining payments in IDR plans.

- Tracking qualifying payments.

- Submitting annual income documentation.

Careful management and documentation help ensure borrowers fully benefit from available relief options.

How do parent, PLUS, and graduate loans fit into funding a return to college?

Parent PLUS loans help parents of dependent undergraduates cover tuition costs not met by other aid. These loans have fixed interest rates higher than undergraduate loans and require a credit check, which can limit eligibility. This option allows parents to invest directly in their child's education when other funding falls short.

Graduate loans, including Grad PLUS loans, target graduate and professional students. They provide funding after federal Direct Unsubsidized loans are maxed out, covering tuition, fees, and living expenses.

Borrowers are the students themselves, assuming full repayment responsibility. Like Parent PLUS loans, Grad PLUS loans require credit approval and carry higher interest rates than undergraduate loans.

Working adults returning to school often combine federal loans with employer tuition benefits. The Society for Human Resource Management reports average tuition reimbursement of about $5,250 per employee annually. This support helps reduce debt by lowering the loan amount needed.

- A graduate student with $15,000 annual tuition and $5,250 reimbursement could use a Grad PLUS loan or a mix of unsubsidized and Grad PLUS loans to cover the $9,750 balance.

- A parent supporting an undergraduate returning student might use a Parent PLUS loan after scholarships, grants, and employer tuition reimbursement are applied.

Knowing credit requirements, loan types, and employer tuition benefits is key to managing education costs effectively.

When should returning borrowers use refinancing or consolidation to manage old and new loans?

Returning borrowers with multiple student loans can simplify repayment by refinancing or consolidating. Refinancing suits those with strong credit and steady income who want to secure a lower interest rate. For instance, consolidating several federal and private loans into a single private loan with a fixed lower rate can save substantial monthly payments.

Consolidation is ideal for borrowers holding multiple federal loans, allowing them to combine these into one Direct Consolidation Loan. This option maintains federal loan benefits such as income-driven repayment plans and forgiveness eligibility. Consolidation also extends loan terms from 10 up to 30 years, reducing monthly payments but increasing total interest costs.

Data from the Federal Reserve Bank of New York shows borrowers without degrees default at nearly three times the rate of degree holders, underscoring the dangers of unmanaged loans and unapproved repayment plans.

Refinancing is ill-advised for those relying on federal protections like deferment, forbearance, or Public Service Loan Forgiveness because private loans cancel these benefits. Consolidation preserves such protections but typically offers no interest rate reduction beyond the weighted average of current loans.

Key factors motivating refinancing or consolidation include:

- Seeking lower interest rates with strong credit through refinancing.

- Desire to combine multiple federal loans without losing repayment options via consolidation.

- Aiming for affordable monthly payments with longer terms through consolidation.

- Eligiblity for federal forgiveness programs requiring retention of federal loans.

How do deferment, forbearance, and default impact returning students' credit and future aid?

Deferment pauses loan payments temporarily without accruing interest on subsidized loans, helping protect credit and maintain eligibility for federal aid. It is typically granted during times of school enrollment or economic hardship, allowing students to avoid penalties and stay in good standing.

Forbearance allows delayed payments, but interest accumulates on all loan types during this period. While it doesn't directly harm credit scores, extended or frequent forbearance may indicate financial stress to lenders. Loans in forbearance remain in good standing, so federal aid eligibility is preserved, but borrowers should be aware of increased debt due to added interest.

Default, occurring after 270 days of missed payments, significantly damages credit scores and triggers collections. It disqualifies students from federal aid programs until loans are rehabilitated or consolidated, a process that can take months and requires consistent payments.

Default also extends repayment periods substantially; the Consumer Financial Protection Bureau notes that many borrowers now take 17-20 years to repay student loans, well beyond the typical 10-year term.

Students facing hardship should contact loan servicers promptly to explore deferment options before considering forbearance. Proactively managing loan status protects credit and access to aid, helping maintain financial stability and progress toward educational goals.

Other Things You Should Know About

Yes, student loans can often be used to cover a variety of education-related expenses beyond tuition. These can include fees, books, supplies, housing, and transportation costs. Federal student loans typically allow borrowing for these expenses as part of the cost of attendance determined by the school.

Returning to college can impact your existing student loans, especially if you re-enroll at least half-time and qualify for in-school deferment or forbearance. In many cases, you may be able to pause payments on prior federal loans while you remain enrolled. However, this depends on the specific loan terms and whether you notify your loan servicer properly.

While there are no federal student loans exclusively for adult or non-traditional students, some federal loan programs and income-driven repayment plans are designed to accommodate a variety of enrollment statuses and income levels. Additionally, certain private lenders may offer loans tailored for returning students, but these tend to vary widely by lender.

Returning to college and borrowing new student loans counts toward your aggregate borrowing limits, which may affect future eligibility. Maintaining good academic standing and making timely payments can help preserve access to federal aid. Failure to do so or defaulting on loans may limit your ability to receive future assistance.