2026 Best Student Loans for Adult Learners

Student Finance & Loan Expert

Many adult learners face challenges securing affordable student loans due to unique financial situations, such as existing debt or variable income streams.

Traditional loan options often lack flexibility, complicating repayment and increasing financial stress. Navigating complex eligibility criteria and interest rates can delay or deter further education, limiting career advancement.

This article examines the best student loan options tailored for adult learners, focusing on programs that offer manageable terms and support diverse financial backgrounds. It aims to guide readers toward informed decisions that align with their educational goals and financial capacity, easing the path to graduate education.

- What types of student loans are best suited for adult learners returning to school? Best loan types

- How do federal and private student loans compare for working adults? Federal vs private

- What eligibility requirements do adult learners face for federal student aid and loans? Adult eligibility

- How should adult learners estimate how much they can safely borrow for college? How much to borrow

- What interest rates, fees, and terms should adult students compare before choosing a loan? Rates and terms

- How do FAFSA and other application steps work for independent and nontraditional students? FAFSA steps

- Which repayment plans work best for adult borrowers balancing family, work, and other debts? Best repayment

- What loan forgiveness and cancellation options can adult learners realistically qualify for? Forgiveness options

- When should adult borrowers consider refinancing or consolidating their student loans? Refinance vs consolidate

- How can adult students avoid delinquency, default, and credit damage on student loans? Avoiding default

What types of student loans are best suited for adult learners returning to school?

Federal student loans are ideal for adult learners returning to school due to their fixed interest rates and flexible repayment options, including income-driven repayment plans that adjust monthly payments based on income and family size. These options help reduce financial stress during career transitions or part-time studies.

For example, Direct Subsidized Loans have interest paid by the government while the borrower is enrolled at least half-time, lowering overall borrowing costs. Adult students looking for the best student loans for adult learners returning to school should also consider state-based loans and employer tuition assistance programs as alternative financing sources.

Private student loans can supplement federal aid when expenses exceed coverage but often come with higher, variable interest rates and fewer borrower protections. Adult learners should compare multiple private lenders, focusing on competitive rates, no prepayment penalties, and flexible repayment terms.

Specialized options such as private dental school loans exemplify niche loan types catering to specific needs.

Parent PLUS Loans are less beneficial for adult learners unless they are dependents with a parent willing to take on debt. Maintaining loans in the student's own name usually offers better control over repayment.

Considering federal trends, fewer first-time, full-time undergraduates received loans recently, with average amounts decreasing, underscoring a move toward borrowing only what is necessary.

Exploring both federal and private loan options for adult students can help borrowers balance cost, repayment flexibility, and borrower protections to support successful educational outcomes.

How do federal and private student loans compare for working adults?

Federal student loans offer key benefits for working adults, including fixed interest rates, income-driven repayment plans, and opportunities for loan forgiveness.

These features create manageable monthly payments based on income and family size, which is essential for adults balancing education with work and family responsibilities. Many adult learners find federal loans to be the safest option, especially compared to private loans.

Private loans, on the other hand, typically have variable interest rates with stricter repayment terms. Approval often depends on strong credit or a co-signer, which can limit access for some students.

Unlike federal loans, private lenders rarely provide income-based repayment or forgiveness, raising financial risks if earnings fluctuate. However, private loans can fill funding gaps due to federal loan limits and may offer higher borrowing amounts or faster disbursement.

The best student loan options for adult learners in the United States involve prioritizing federal loans first to leverage borrower protections. After exhausting federal options, some may consider private solutions cautiously.

It's important to thoroughly evaluate terms and eligibility, including checking federal repayment programs, to avoid future financial hardship. In recent years, federal and nonfederal education loans totaled $102.6 billion for students and parents, reflecting a 38% decline since 2010-11 when adjusted for inflation, according to College Board. This highlights a trend toward more cautious borrowing.

For those exploring alternative funding, the Ascent student loan application offers insights into private lending options designed to assist with education costs.

What eligibility requirements do adult learners face for federal student aid and loans?

Adult learners seeking federal student aid must meet specific eligibility requirements similar to traditional students but with considerations for their nontraditional status. To qualify for most federal aid programs, applicants need to demonstrate financial need, except for unsubsidized loans which do not require this.

Key criteria include U.S. citizenship or eligible noncitizen status, enrollment at least half-time in an eligible program, and a valid Social Security number. These points are essential when reviewing adult learner eligibility requirements for federal student aid.

Maintaining satisfactory academic progress is another requirement, usually involving a minimum GPA and timely degree completion, which varies by institution. Applicants with prior loan defaults or drug convictions might face restrictions or need to resolve these issues first.

Additionally, those who have already earned a bachelor's degree have limited access to federal undergraduate loans but may still qualify for graduate-level federal loans. This highlights important federal student loan qualifications for adult students.

Federal loans generally do not heavily weigh credit history, benefiting adult learners with less established credit profiles. Loan eligibility and amounts depend on the borrower's dependency status.

Most adult learners qualify as independent and can rely on their own income and assets. Understanding repayment options is vital, as federal loans offer income-driven repayment plans and deferment options suited for adults managing work or family commitments.

Private lenders differ by offering fixed APR rates ranging from about 4.19% with autopay for borrowers with excellent credit to nearly 17% for those with lower qualifications. This contrast underscores how creditworthiness significantly influences borrowing costs.

For more information on support available, explore financial aid for adults returning to college.

How should adult learners estimate how much they can safely borrow for college?

Adult learners can calculate safe college loan amounts by first adding tuition, fees, books, supplies, and personal expenses for their entire program. From this total, subtract any scholarships, grants, or personal savings to find the maximum loan needed.

Estimating responsible student loan borrowing for adult learners involves focusing on borrowing only what is essential to avoid financial strain later.

The average bachelor's degree borrower finished with $29,560 in student loan debt, a decrease from $35,600 ten years prior, showing that managing debt loads is achievable despite rising tuition costs.

When deciding how much to borrow, consider these points:

- Estimate your expected entry-level salary to gauge monthly loan payments in relation to income.

- Choose a repayment period fitting your budget, typically 10 to 20 years.

- Use online loan calculators to predict monthly payments and total interest based on current terms.

- Account for extended program lengths if attending part-time or juggling work and school.

- Prioritize federal loans over private loans because of better repayment plans and protections.

Strategies such as budgeting future income against debt and limiting borrowing to essential amounts help manage debt responsibly. Tools like the best banks that refinance student loans can also assist borrowers in managing repayment effectively.

What interest rates, fees, and terms should adult students compare before choosing a loan?

Adult students should carefully compare interest rates, fees, and loan terms to minimize their debt burden. Federal student loans offer fixed interest rates ranging from about 4.99% to 7.54% for undergraduates and graduate students, typically lower than most private loans, which can vary widely and exceed 10%. Fixed rates provide predictable monthly payments, while some private lenders offer variable rates that may increase over time, resulting in higher costs.

Loan fees significantly impact the total repayment amount. Federal loans usually include origination fees around 1% to 1.05%, deducted from the loan disbursement. Private loans can have higher or additional fees such as application charges or prepayment penalties.

Repayment terms range from 5 to 30 years. Federal loans offer flexible options like income-driven repayment plans that adjust monthly payments based on income and family size. This flexibility benefits adult learners with variable incomes or dependents.

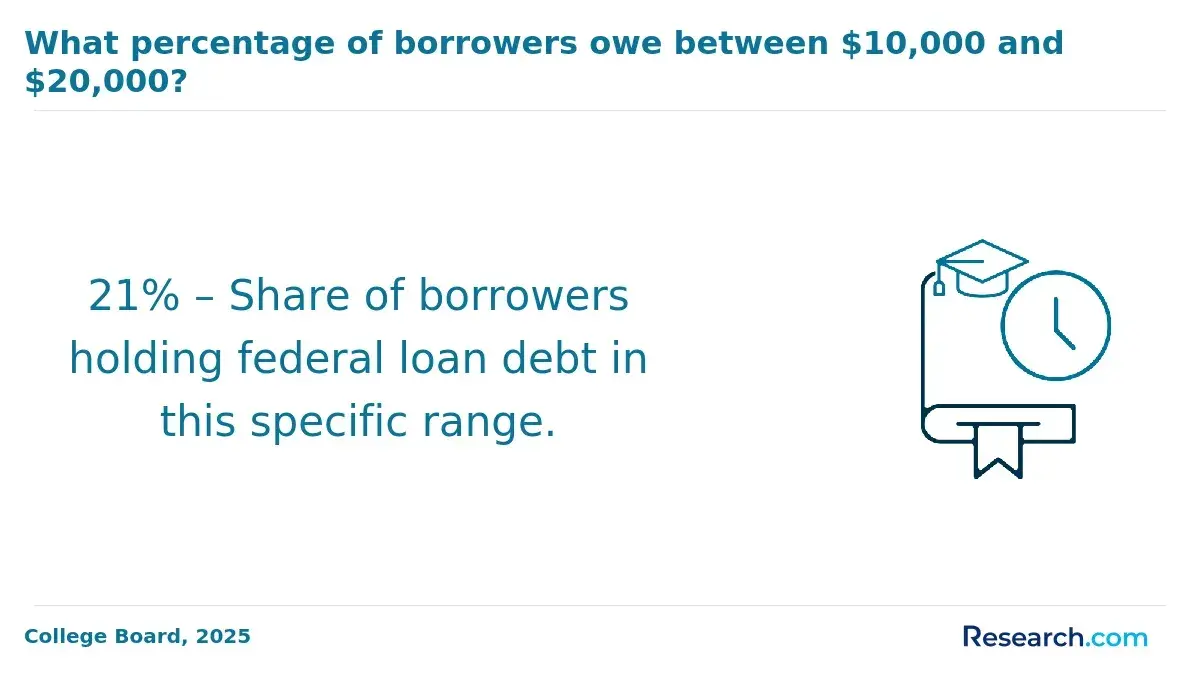

The College Board reports that borrowers with federal balances under $20,000-often mid-career adults-represent 53% of borrowers but only 12% of outstanding federal debt, highlighting many adult learners carry relatively low balances that can be managed with these plans.

Private loans rarely provide income-based repayment or forgiveness, often featuring fixed repayment schedules and fewer borrower protections, increasing risk for adult students. Consider deferment, forbearance options, or consolidation to improve loan management.

How do FAFSA and other application steps work for independent and nontraditional students?

Independent students, such as those over 24, married, veterans, or with dependents, need to provide their own financial information when applying for FAFSA, excluding parental data. This includes reporting income, assets, and tax information from the prior-prior year (for upcoming FAFSA cycles, that means 2024 tax details).

Essential steps include:

- Gathering federal tax returns, W-2s, and bank statements for income verification.

- Completing the FAFSA application online at fafsa.gov or via the official app, where dependency status is determined automatically.

- Selecting up to ten schools to receive your FAFSA results; make sure to include every college you're applying to.

- Submitting the FAFSA as soon as possible after October 1, 2025, to optimize chances for grants and scholarships with limited funds.

- Reviewing your Student Aid Report (SAR) carefully to ensure all information is accurate and promptly correcting any mistakes.

Nontraditional students may need extra documentation such as proof of active military service or legal guardianship. They should explore scholarships and grants targeting adult learners, as most first-time, full-time undergraduates receive award-based aid, reducing loan dependency according to the National Center for Education Statistics.

Meeting FAFSA deadlines and submitting complete applications increases eligibility for federal grants, like Pell Grants, which do not require repayment. Many private and state aid programs also mandate FAFSA submission, making it critical regardless of independent status. Incomplete or inaccurate FAFSA forms can delay aid or limit loan options.

Which repayment plans work best for adult borrowers balancing family, work, and other debts?

Income-driven repayment (IDR) plans benefit adult borrowers juggling family, work, and multiple debts by capping monthly payments at 10% to 20% of discretionary income. This reduces financial stress and helps avoid default during times of lower or irregular earnings.

Plans like Revised Pay As You Earn (REPAYE) and Income-Based Repayment (IBR) adjust payments annually based on income and family size. For example, a family of four earning $50,000 yearly might pay $300 monthly instead of a fixed $600.

Graduated repayment plans support those anticipating income growth by starting with lower payments that increase every two years. This feature helps adult learners manage current expenses while preparing for higher future earnings.

Private student loan borrowers face challenges since these loans typically lack IDR options or federal protections. Private loans represent about one-fifth of new borrowing annually but only 8-9% of total student debt, creating difficulties for those who have maxed out federal aid, according to The Institute for College Access & Success (TICAS).

Refinancing private loans with flexible terms or longer repayment schedules can ease monthly payments but may raise total interest costs. Careful evaluation of this trade-off is essential for budgeting.

What loan forgiveness and cancellation options can adult learners realistically qualify for?

Adult learners can access several federal student loan forgiveness and cancellation programs based on their employment sector and repayment plan.

Public Service Loan Forgiveness (PSLF) offers forgiveness after 120 qualifying payments while working full-time in government or nonprofit roles. Income-Driven Repayment (IDR) plans forgive any remaining debt after 20 to 25 years of payments adjusted for income and family size.

Teacher Loan Forgiveness targets educators working full-time in low-income schools for five consecutive years, potentially forgiving up to $17,500. Borrowers with documented disabilities that prevent substantial gainful employment may qualify for Total and Permanent Disability (TPD) Discharge.

Bankruptcy discharge of student loans is rare and requires proving "undue hardship" through legal processes. Closed school discharge protects borrowers if their school closes while they are enrolled or soon after withdrawal.

Maintaining accurate employment and repayment records is essential, especially for PSLF, which requires annual employment certification. Job changes can disrupt qualifying payments and delay forgiveness.

Financial planning should weigh borrowing against potential earnings gains. Research from Georgetown University Center on Education and the Workforce shows adults completing a bachelor's degree after age 24 can earn a median $20,000 more annually. This income boost makes managing student loans more practical despite extended forgiveness timelines.

When should adult borrowers consider refinancing or consolidating their student loans?

Adult borrowers often weigh refinancing and consolidation options to manage student loan debt effectively. Refinancing offers a chance to replace existing loans with a new private loan, typically lowering interest rates and monthly payments for those with strong credit and stable income.

However, refinancing federal loans into private ones eliminates federal protections like income-driven repayment plans and loan forgiveness programs.

Consolidation, on the other hand, combines multiple federal loans into a single Direct Consolidation Loan. This simplifies payments and may extend repayment terms, reducing monthly burdens but possibly increasing total interest.

It preserves federal benefits, making it suitable for borrowers who want to maintain access to forgiveness programs and flexible repayment options.

Financial goals and circumstances influence the decision. For example, a 62-year-old with average debt around $42,780 might choose consolidation to protect federal options while managing retirement finances.

Younger borrowers with steady income might prefer refinancing to cut interest costs and shorten repayment periods.

How can adult students avoid delinquency, default, and credit damage on student loans?

Adult learners should maximize federal loan options before considering private loans, which often have higher interest rates and fewer repayment benefits. According to The Institute for College Access & Success (TICAS), nearly one-third of undergraduates used private loans without exhausting federal aid, risking increased financial strain.

To reduce risk of default, borrowers should:

- Enroll in income-driven repayment plans that adjust payments based on income.

- Contact loan servicers promptly after missed payments to explore options like deferment or forbearance.

- Set up automatic payments to avoid accidental missed payments and qualify for interest rate discounts.

- Create realistic budgets prioritizing loan payments and emergency savings.

- Avoid additional borrowing unless necessary and compare interest rates and repayment benefits.

Federal loans offer protections like public service loan forgiveness and flexible schedules not commonly available with private loans. Adult students balancing work and study should consider income fluctuations when planning payments.

Missed payments over 90 days can trigger delinquency and eventually default, which seriously damages credit scores and may lead to wage garnishment.

Staying in communication with loan servicers, regularly reviewing statements, and seeking financial counseling can help maintain credit health.

Other Things You Should Know About the Best Student Loans for Adult Learners

Work experience itself does not directly affect eligibility for federal or private student loans. Lenders primarily consider credit history, income, and enrollment status when determining loan approval and terms. However, steady employment and income can strengthen your loan application by demonstrating repayment ability.

Many federal and private lenders allow part-time students to apply for loans, but eligibility and loan amounts may differ from full-time enrollment. Federal student loans generally require at least half-time enrollment, while private lenders have varying policies. It is important for part-time adult learners to confirm enrollment requirements with the lender before applying.

For federal unsubsidized loans and most private loans, interest continues to accrue during deferment or forbearance periods, increasing the total repayment amount. Subsidized federal loans do not accrue interest during deferment. Adult learners should carefully consider the impact of deferment or forbearance on loan costs before choosing these options.

Yes, federal and many private student loans can be used for qualified education expenses beyond tuition, such as books, supplies, housing, and transportation. Lenders specify allowable costs, so borrowers should ensure their loan funds are used according to guidelines to avoid issues with loan compliance.