2026 Best Student Loans for Graduate Certificates

Student Finance & Loan Expert

Many prospective graduate students confront the challenge of funding certificate programs without clear guidance on loan options. Navigating various student loan products can become overwhelming, especially for those shifting fields after an undergraduate degree. The risk of borrowing unsuitable loans or facing high interest rates can deter education advancement.

Understanding available loans tailored for graduate certificates is essential for informed financial decisions and minimizing long-term debt. This article analyzes key student loan options, highlighting their terms and benefits to help readers select appropriate financing solutions and avoid common pitfalls in securing funds for graduate certificate studies.

- What counts as a graduate certificate program for student loan eligibility? Qualifying Graduate Certificates for Student Loans

- Which federal student loans are available for graduate certificate students? Federal Loan Options for Graduate Certificate Students

- How do private student loans for graduate certificates compare to federal loans? Private vs. Federal Student Loans for Graduate Certificates

- What are the current interest rates and borrowing limits for graduate certificate loans? Rates & Limits for Graduate Certificate Loans

- How do you qualify and apply for loans for a graduate certificate program? Qualifying and Applying for Graduate Certificate Loans

- Which lenders offer the best private loans specifically for graduate certificates? Best Private Loans for Graduate Certificates

- What repayment plans work best for short, intensive graduate certificate programs? Best Repayment Plans for Short Certificate Programs

- Are graduate certificate student loans eligible for forgiveness or income-driven plans? Forgiveness Options for Graduate Certificate Loans

- When does refinancing or consolidating graduate certificate loans make financial sense? Refinancing Options for Graduate Certificate Loans

- How can you minimize borrowing and out-of-pocket costs for a graduate certificate? Lowering Costs for a Graduate Certificate

What counts as a graduate certificate program for student loan eligibility?

Graduate certificate programs eligible for student loans must be offered by accredited institutions and provide advanced training beyond a bachelor's degree, though typically less comprehensive than a master's degree. These programs emphasize specialized skills in areas such as healthcare, education, technology, or business. For eligibility, federal student aid requires the program to be recognized by the U.S. Department of Education as qualified for Title IV funding.

Programs usually range from 12 to 30 credit hours and can often be completed in under a year. They are designed for working professionals seeking career advancement without enrolling in a full master's program. Examples include certificates in data analytics, project management, cybersecurity, or instructional design.

Students interested in financing should understand the criteria for student loan eligibility for graduate certificates, as private lenders vary in their support for certificate loans; some approve only degree programs. It is critical to distinguish graduate certificates from undergraduate ones, which rarely qualify for graduate-level loans. Confirming program classification and accreditation with a school's financial aid office is essential.

According to the National Center for Education Statistics, U.S. institutions conferred around 410,000 post-baccalaureate and post-master's certificates-reflecting a 70% increase over the past decade-signaling expanding loan opportunities. However, potential borrowers should carefully evaluate costs and aid eligibility, including whether loans cover additional expenses like rent, as explained in can you use student loans to pay for rent.

Which federal student loans are available for graduate certificate students?

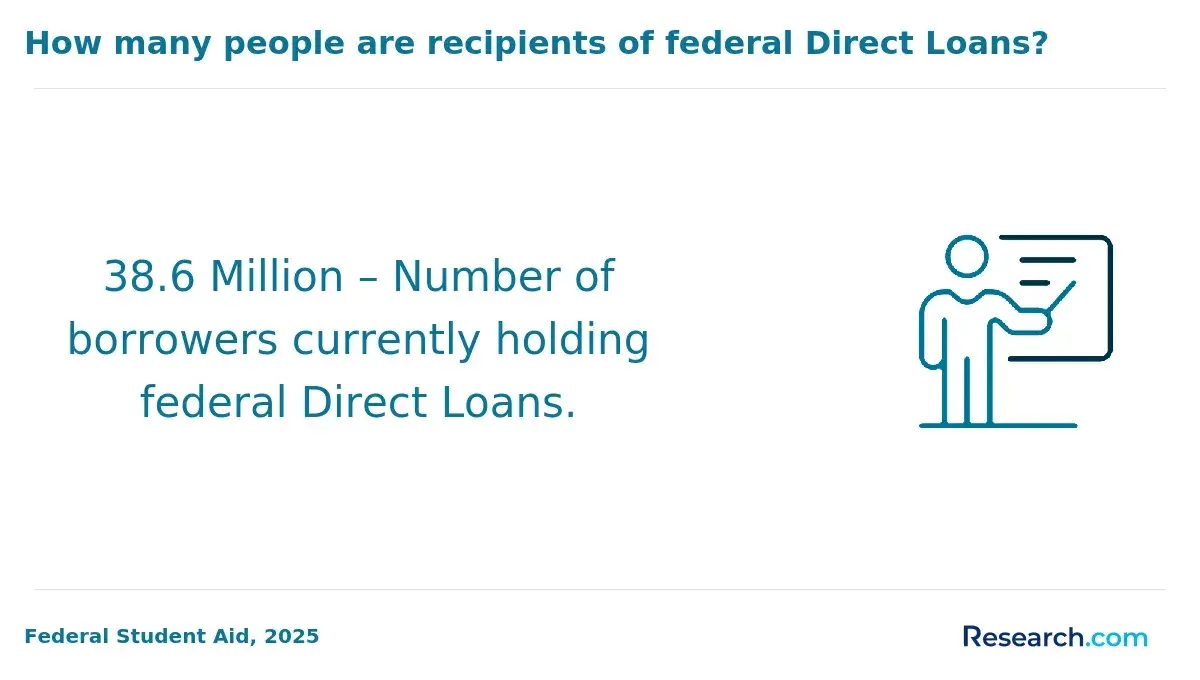

Federal student loans available for graduate certificate students primarily include Direct Unsubsidized Loans and Direct PLUS Loans. Direct Unsubsidized Loans have fixed interest rates and permit borrowing up to $20,500 annually without requiring credit approval. Interest begins accruing immediately after disbursement, which can increase repayment costs if not managed carefully. Direct PLUS Loans provide additional funding beyond the unsubsidized loan limit but require a credit check and typically carry higher interest rates.

Graduate certificate programs usually have lower tuition costs, with a median of around $13,000 according to EducationData.org's analysis, compared to about $39,000 for master's degrees. This difference means students often only need Direct Unsubsidized Loans for tuition and fees, helping them avoid higher-cost debt. Eligibility criteria for federal loans for graduate certificate students excludes subsidized loans and federal work-study opportunities. The Perkins Loan program is no longer available for these students, so private loans may be necessary if federal loan limits are insufficient.

Completing the FAFSA annually is required to apply for Direct Loans. Students should explore income-driven repayment plans that adjust monthly payments based on earnings, an important option for working professionals pursuing certificates. Those interested in taking out loans independently can find useful guidance about student loans without parent information.

Understanding these federal loan types and their terms is essential for managing graduate certificate education finances responsibly.

How do private student loans for graduate certificates compare to federal loans?

Private student loans vs federal loans for graduate certificates present notable differences that affect borrowing choices. Federal loans offer benefits such as fixed interest rates, income-driven repayment plans, and loan forgiveness options, which are largely unavailable with private loans. In contrast, private student loans for graduate certificates often have variable rates and stricter repayment terms, potentially leading to higher long-term costs.

Graduate certificate students tend to rely more on private lenders because federal loans cap annual and total borrowing amounts, which may not fully cover costs especially at private or out-of-state institutions. According to U.S. Department of Education data, private loans make up about 8% of overall student loan debt but represent nearly 22% among graduate and professional borrowers.

Private lenders usually require a creditworthy cosigner and lack the flexible repayment options found in federal loans. These options include deferment, forbearance, and payment postponement during enrollment or economic hardship without damaging credit. Using private loans as a supplement rather than a replacement ensures students retain federal protections and minimize overall debt burdens.

Students should carefully compare interest rates, fees, and repayment flexibility. Exploring resources such as best student loan refinance bonus programs can help manage debt. Prioritizing federal borrowing maximizes the benefits of federal loans compared to private student loans for graduate certificates.

What are the current interest rates and borrowing limits for graduate certificate loans?

Interest rates for graduate certificate loans in 2026 generally range between 5% and 12% for federal unsubsidized loans, varying by loan type and origination year. Private lenders offer more varied rates starting around 4% and reaching up to 15%, largely depending on the borrower's credit and presence of a cosigner. Borrowers with strong credit scores above 720 and a qualified cosigner often secure rates 2 to 3 percentage points lower. LendEDU's 2025 review highlights approval rates over 90% for such applicants.

Borrowing limits for graduate certificate student loans typically follow federal loan guidelines. Federal Direct Unsubsidized Loans allow about $20,500 annually, with a lifetime cap of $138,500 including previous graduate loans. Private loans may fund up to 100% of school-related expenses such as tuition, fees, books, and living costs, with limits influenced by credit and program costs.

Several factors should be considered when comparing loan options:

- Federal loans provide fixed interest rates and flexible repayment plans but generally lower borrowing limits.

- Private loans involve credit checks; cosigners improve both approval chances and interest rates.

- Loan approval and competitive rates depend heavily on credit history and institutional eligibility.

Careful assessment of loan terms is vital, especially when seeking funds for non-degree programs. For specialized needs, explore resources about private nursing school loans as a relevant example of tailored lending options.

How do you qualify and apply for loans for a graduate certificate program?

To access loans for graduate certificate programs, enrollment in an accredited institution offering these certificates is required. Federal student loans are accessible after submitting the Free Application for Federal Student Aid (FAFSA) and meeting eligibility criteria such as U.S. citizenship or an eligible non-citizen status. Private lenders typically require a credit check and proof of enrollment before approval.

Approximately 65% of graduate private student loans involve cosigners, as reported by Credible's internal data. When a borrower has limited credit history or income, a cosigner with strong credit increases the likelihood of loan approval significantly.

Key steps in the loan application process include:

- Completing FAFSA to qualify for federal aid.

- Submitting verification of enrollment to lenders.

- Comparing interest rates and loan terms from several lenders.

- Providing income information and consent for credit checks if required.

- Requesting the desired loan amount and agreeing to loan terms.

Many borrowers are unaware they can apply for cosigner release after demonstrating consistent, on-time payments and improved credit scores. Less than 10% pursue cosigner release, an option that can reduce financial responsibility and increase borrower independence. It is important to review each lender's specific policy on cosigner release. Early loan applications help avoid processing delays, and seeking financial aid counseling is recommended to fully understand loan obligations and options.

Which lenders offer the best private loans specifically for graduate certificates?

Private loans designed for graduate certificates often come from lenders such as SoFi, Discover, and College Ave, who cater to the needs of working professionals and nontraditional students. These lenders typically offer competitive interest rates, flexible repayment options, and frequently do not require a cosigner, making financing more accessible.

SoFi's loans feature both fixed and variable interest rates starting near 5.99%, with no origination fees in many cases. Additionally, SoFi provides benefits like unemployment protection and career coaching, which support students balancing employment and education.

Discover offers loans with rates beginning around 6.99% and includes a 1% cash-back reward on the first payment, helping certificate students offset costs. College Ave stands out for its customizable loan terms, allowing borrowers to align repayments with their budget and program length, with rates starting close to 5.95%. Its simple online application process is suited for one- to two-year certificate programs.

These lenders base approval on creditworthiness, including income verification, making them ideal for graduate students currently working or returning to the workforce.

A report from the Georgetown University Center on Education and the Workforce notes that graduates with certificates in fields like cybersecurity and nursing can expect median earnings gains of 15-25% within three years, reinforcing the value of thoughtfully selected private loans paired with flexible terms and reasonable rates.

What repayment plans work best for short, intensive graduate certificate programs?

Income-driven repayment (IDR) plans offer valuable flexibility for students pursuing short graduate certificate programs, adjusting monthly loan payments based on income and family size. These plans help keep payments manageable during and after studies, which is essential for programs typically under two years. Graduates often benefit from the Revised Pay As You Earn (REPAYE) or Income-Based Repayment (IBR) plans, capping payments at 10-15% of discretionary income and providing forgiveness after 20-25 years.

These options are particularly helpful for certificate holders who may face fluctuating incomes early in their careers. In contrast, private loans tend to lack such income-based flexibility, increasing the risk of default. According to the U.S. Department of Education's 2024 repayment data, borrowers with graduate or professional certificates have a three-year default rate of about 6%, compared to roughly 11% for bachelor's degree holders, highlighting the benefits of tailored repayment strategies.

For those with consistent income, standard 10-year repayment plans can reduce long-term interest costs, though they require steady employment. Key strategies include:

- Using IDR plans to maintain affordable payments

- Reviewing loan servicer options for optimal benefits

- Considering loan consolidation cautiously to avoid extended repayment without increased costs

- Prioritizing federal loans before private loans without income-based options

Aligning repayment choices with program length and expected earnings can reduce financial stress and default risk for graduate certificate borrowers.

Are graduate certificate student loans eligible for forgiveness or income-driven plans?

Graduate certificate student loans that are federal Direct Loans qualify for federal income-driven repayment (IDR) plans, which adjust monthly payments based on income and family size. These plans can offer valuable relief for borrowers earning short-term graduate credentials. However, programs like Public Service Loan Forgiveness (PSLF) require consistent payments on qualifying federal loans for at least 10 years, which may not align well with many certificate holders' shorter study periods and loan amounts.

The upcoming elimination of the Grad PLUS Loan for new graduate borrowers starting in 2026 poses a significant challenge. Credible's 2025 policy brief on the Obey-Byrd Borrowing and Budget Act highlights a funding shortfall of $8,000-$15,000 per graduate student annually. This gap often leads students to private loans that typically lack income-driven repayment options or forgiveness programs, increasing financial risk.

Prospective students should:

- Maximize borrowing through federal Direct Loans to maintain eligibility for IDR and forgiveness programs.

- Consult financial aid offices regarding alternative funding or scholarships before resorting to private loans.

- Assess whether the graduate certificate's potential income uplift justifies private loan risks.

Federal loan borrowers need to monitor loan types and repayment plans carefully, since while Grad PLUS loans will no longer be available, federal Direct Loans will still allow access to income-driven plans and forgiveness.

When does refinancing or consolidating graduate certificate loans make financial sense?

Refinancing or consolidating graduate certificate loans can reduce interest costs and simplify repayment, especially for borrowers with high-interest private loans who have improved their credit scores since graduation. For instance, lowering a 9% private loan to 5% interest can save thousands in interest over the loan's life. Consolidation combines multiple federal loans into one payment, easing management but often extending repayment periods, which may increase total interest paid.

Career outcomes also impact loan decisions. A Strada Education Foundation survey reports 58% of graduate certificate holders in STEM and healthcare fields experience significant pay increases or career advancements. These graduates may benefit from faster repayment to minimize interest costs, making refinancing an attractive option.

By contrast, only 34% in business and 27% in social sciences report similar gains. For them, consolidation might provide needed payment relief through longer terms, despite higher cumulative interest. Income-driven repayment plans remain viable if refinancing causes loss of federal protections.

Consider these factors when deciding:

- Current interest rates and credit score improvements

- Loan type: federal versus private

- Expected income growth based on field-specific ROI statistics

- Need for payment flexibility or loan forgiveness options

Ultimately, refinancing or consolidating makes financial sense if it lowers costs or simplifies repayment without sacrificing key federal benefits or significantly extending loan terms.

How can you minimize borrowing and out-of-pocket costs for a graduate certificate?

Minimizing borrowing and out-of-pocket expenses for a graduate certificate involves strategic use of all available funding sources. Prioritize scholarships aimed specifically at graduate certificates, as many institutions and foundations offer targeted awards that reduce loan dependence. Investigate employer tuition assistance programs, since 51% of U.S. employers provide tuition support and 63% of those include coverage for short-form credentials like graduate certificates.

Use employer benefits to cover tuition costs before considering loans. Consult your HR department to understand eligibility, application procedures, and whether flexible repayment or reimbursement plans tied to continued employment are available. Evaluate federal student loans prior to private ones, as federal loans usually have lower interest rates and more flexible repayment options. Borrow only the amount necessary within established limits.

Choosing public or online institutions can often lower tuition expenses. Community colleges and state universities may offer graduate certificates at a fraction of private school costs. Participating in work-study programs or part-time jobs related to your field can help offset other expenses.

Additionally, explore grants or scholarships from professional associations and carefully budget for non-tuition costs like books and fees to avoid unexpected borrowing. Effective financial planning significantly reduces the need for costly loans.

Other Things You Should Know About

Yes, student loans can typically cover qualified education expenses beyond tuition, including fees, books, supplies, and sometimes living costs. Federal loans also allow for some flexibility in covering necessary education-related expenses while enrolled in a graduate certificate program. However, it is important to check with your loan servicer or lender to understand exactly what costs are eligible under your specific loan.

Federal student loans generally do not require a credit check, so they have minimal impact on credit scores at the time of borrowing. Private loans usually involve credit evaluations, and missing payments can negatively affect your credit. Managing your loan payments responsibly while pursuing your graduate certificate is important to maintain a healthy credit profile.

Yes, many federal student loans offer deferment and forbearance options that allow temporary suspension or reduction of payments during financial hardship or other qualifying circumstances. Private lenders may offer similar options, but they vary widely, so borrowers should review terms carefully. These tools can provide relief if you face unexpected challenges during or after your graduate certificate studies.

Repayment duration depends on the loan type, amount borrowed, and repayment plan chosen. Graduate certificate loans may have shorter repayment terms compared to full degree loans due to the usually smaller amounts borrowed. Standard federal loan repayment terms range from 10 to 25 years, but income-driven and accelerated repayment plans can adjust this timeline accordingly.