2026 Best Student Loan Refinance for New Graduates

Student Finance & Loan Expert

Many recent graduates face the challenge of managing high-interest student loans that strain their finances as they start their careers. Rising debt payments can delay essential milestones like saving for a home or building credit. Refinancing offers an option to reduce interest rates, consolidate debt, or adjust repayment terms, easing monthly burdens. However, navigating lender options and understanding eligibility can be complex and overwhelming. This article examines the best student loan refinance options available, providing clear guidance to help new graduates make informed decisions and improve their financial outlook efficiently.

- What is student loan refinancing and when does it make sense for new graduates? What is student loan

- How can I compare the best student loan refinance rates and terms right now? How can I compare

- Do I lose federal protections and forgiveness options if I refinance my student loans? Do I lose federal

- What credit score, income, and debt-to-income ratio do refinance lenders typically require? What credit score, income,

- How do fixed vs variable refinance interest rates affect long-term costs for graduates? How do fixed vs

- Which lenders offer the best refinance options for undergraduate, graduate, and professional degrees? Which lenders offer the

- How can new graduates decide between refinancing, federal consolidation, or staying in current plans? How can new graduates

- What steps are involved in the refinance application, approval, and disbursement process? What steps are involved

- How does refinancing impact monthly payments, payoff timelines, and total interest paid? How does refinancing impact

- What refinance strategies can help new graduates manage risk and protect their credit? What refinance strategies can

What is student loan refinancing and when does it make sense for new graduates?

Student loan refinancing replaces existing loans with a new loan that usually offers a lower interest rate or better terms. This process helps borrowers reduce monthly payments, lower overall interest costs, or shorten repayment periods. Refinancing options for new graduates work best when they have strong credit and stable income, qualifying them for rates better than federal or original private loans.

Many federal Direct Loan borrowers face high interest rates; among those entering repayment, over half have rates above 5%, with a significant portion exceeding 7%, according to the U.S. Department of Education's Federal Student Aid Data Center. Refinancing can secure rates below these, especially with competitive private lenders, potentially saving thousands over the life of a loan.

Benefits include lower monthly payments via reduced rates or extended terms, flexible repayment plans to match income or career changes, and simplified finances through loan consolidation. Refinancing also allows converting variable-rate loans to fixed-rate for stability. However, it involves losing federal protections such as income-driven repayment plans and forgiveness programs. New graduates considering when to refinance student loans after graduation should evaluate their financial stability and need for federal benefits carefully.

Key factors when comparing offers are:

- Interest rates relative to current loans

- Loan terms and flexibility

- Eligibility impact for federal assistance

For those needing urgent funding, exploring quick student loans might be worthwhile. Ultimately, refinancing is strategic for graduates who can improve loan terms without sacrificing essential protections.

How can I compare the best student loan refinance rates and terms right now?

To secure the best student loan refinance rates for new graduates, compare detailed offers from various lenders focusing on the annual percentage rate (APR), which shows the loan's true cost including fees. Consider whether fixed or variable rates fit your needs: fixed rates offer payment stability, while variable rates often start lower but can rise over time.

When you compare student loan refinance terms and offers, take note of loan lengths. Shorter terms reduce total interest but increase monthly payments, while longer terms lower monthly payments at the expense of more interest paid. Choose a repayment schedule that balances your budget and debt goals.

Eligibility criteria vary; some lenders require minimum credit scores, steady income, or a co-signer. Assess your credit and employment status to target lenders where approval is realistic. Also, look for benefits like unemployment protection, autopay discounts, or flexible payment options which could ease financial stress.

Online comparison tools can help aggregate offers, but verify details on official lender websites to avoid outdated rates. For example, a 5.0% APR fixed rate over 10 years should be weighed against a 4.5% variable rate that might increase.

The average federal student loan balance for borrowers under age 25 has grown significantly, highlighting the importance of refinancing wisely. For those applying without parental assistance, check resources on FAFSA without parents.

Do I lose federal protections and forgiveness options if I refinance my student loans?

Refinancing federal student loans into a private loan eliminates critical federal protections lost when refinancing student loans, including income-driven repayment plans, deferment and forbearance options, and eligibility for forgiveness programs like Public Service Loan Forgiveness (PSLF). Private lenders govern the new loan without these federal safeguards.

This loss impacts borrowers relying on federal loan forgiveness options. Federal loans provide essential relief during financial hardships such as unemployment or disability, offering temporary payment pauses that private loans rarely match. Refinancing often trades borrower safety nets for potentially lower interest rates.

Average fixed refinance rates for borrowers with credit scores above 720 decreased from 7.11% to 5.84% in recent years, according to Credible's Student Loan Refinance Rate Report. While attractive, this rate reduction comes with the risk of losing federal protections. Borrowers with stable incomes and emergency savings might benefit, but those facing financial volatility could face greater challenges.

Your decision should align with your financial stability and repayment goals. Borrowers aiming for forgiveness programs or federal relief should avoid refinancing federal loans. Those focused solely on reducing interest payments may want to explore private refinancing carefully. For more information on various options, see best student loan refinance offers.

What credit score, income, and debt-to-income ratio do refinance lenders typically require?

Refinance lenders generally require a minimum credit score between 650 and 700 for new graduates to qualify. Borrowers with scores below 650 often face higher interest rates or denial, while those above 700 gain access to better terms. These credit score requirements for student loan refinancing play a crucial role in approval decisions. Income and debt to income ratio criteria for refinance lenders typically include a stable monthly income enough to cover debt and living expenses, often requiring $2,000 to $3,000 per month in gross earnings. Some lenders also accept co-signers if income is insufficient.

Debt-to-income (DTI) ratios are important; most lenders require a DTI below 40% to 45%. This means total monthly debt payments, including rent and loan installments, should not exceed this percentage of gross monthly income. For example, a graduate earning $3,000 per month should ideally have no more than $1,200 to $1,350 dedicated to debt repayments.

Credit rebuilding is common after graduation. Experian's "State of Credit" report shows the average VantageScore for borrowers aged 22-25 improves by 41 points within two years of full-time employment, reinforcing the importance of consistent on-time payments and managing credit wisely.

Applicants should check their credit score and DTI ratio before applying. Those who do not meet criteria can increase approval chances by boosting income, reducing debt, or partnering with a creditworthy co-signer. For those interested in financial support beyond refinancing, resources like financial aid for nursing school can offer additional guidance.

How do fixed vs variable refinance interest rates affect long-term costs for graduates?

Fixed refinance interest rates offer stability by keeping payments consistent throughout the loan term. This predictability helps graduates budget effectively, especially when market interest rates rise. Locking in a fixed rate today means knowing your monthly payment and total repayment costs upfront. However, fixed rates typically start higher than variable rates, which might increase initial expenses.

Variable refinance interest rates generally begin lower, helping reduce short-term payments. This option suits borrowers expecting income growth or planning early loan repayment. Yet, variable rates fluctuate with market trends, potentially raising monthly payments over time. This uncertainty can lead to increased costs if interest rates climb.

Key factors to consider when choosing between fixed and variable rates include financial stability and risk tolerance:

- Stable income and a fixed budget may make fixed rates preferable.

- Anticipated income growth might justify accepting the risk of variable rates for lower initial payments.

Additionally, repayment plans greatly influence overall costs. For example, federal income-driven repayment plans accounted for a median payment of 4.2% of discretionary income, compared to 10.7% under standard 10-year plans, according to the Congressional Budget Office's analysis.

Refinancing decisions should be made alongside repayment strategies, as the interaction between loan type and repayment plan affects cash flow and long-term expenses differently.

Which lenders offer the best refinance options for undergraduate, graduate, and professional degrees?

Top lenders like SoFi, Earnest, and CommonBond offer competitive student loan refinance options tailored to diverse degree programs and credit profiles. These lenders provide fixed and variable interest rates starting as low as 2.99% APR, with repayment terms ranging from 5 to 20 years.

Key benefits include:

- SoFi: No-fee refinancing, unemployment protection, and career coaching to support borrowers during employment changes.

- Earnest: Personalized loan terms based on income and expenses, ideal for those with variable earnings.

- CommonBond: Competitive pricing combined with social impact initiatives funding education for underserved communities.

Professional degree holders benefit from longer loan terms and higher borrowing limits, allowing manageable monthly payments during residency or early careers. Many lenders also offer co-signer release after consistent on-time payments, reducing financial burden as careers advance.

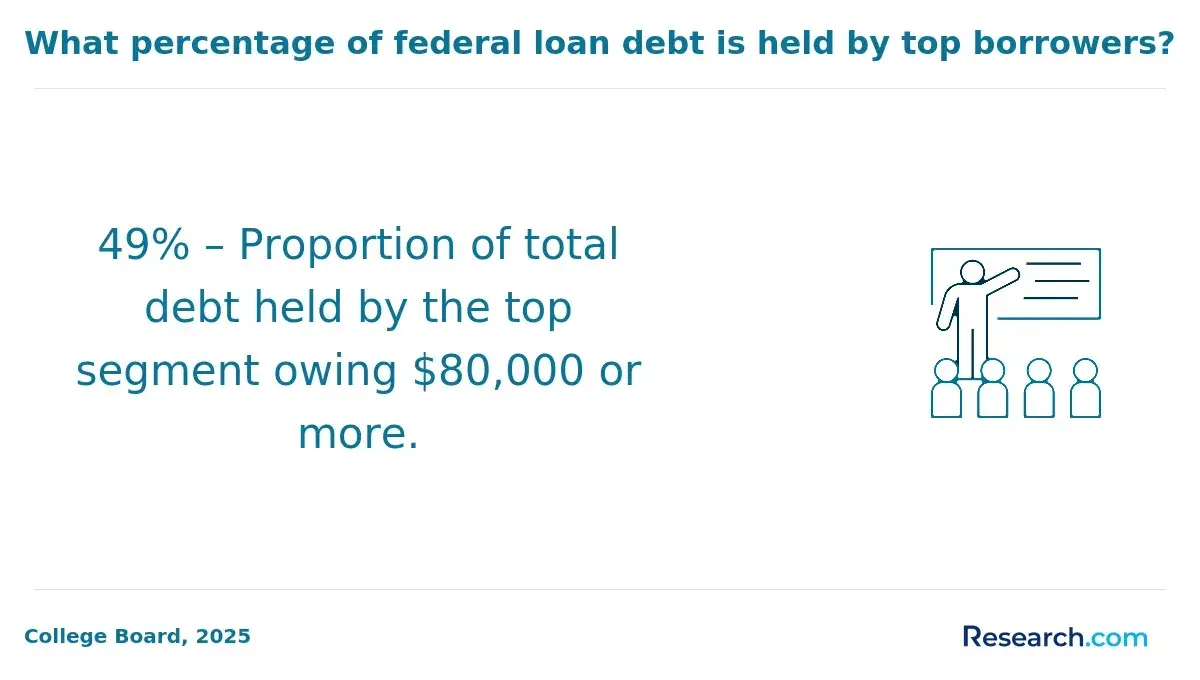

Refinancing federal loans into private options forfeits eligibility for government programs like Public Service Loan Forgiveness or income-driven repayment forgiveness. Approximately 8.1 million borrowers qualified for such federal benefits, but a notable portion entered ineligible plans or refinanced privately, losing these protections.

Careful comparison of lender offers and consideration of career plans and loan forgiveness eligibility is essential to securing refinance terms best suited to individual educational and financial goals.

How can new graduates decide between refinancing, federal consolidation, or staying in current plans?

Graduates weighing options among refinancing, federal consolidation, or staying in current student loan plans should carefully assess their financial situation and long-term goals. Refinancing usually offers lower interest rates by leveraging improved credit scores or steady employment. Data from the Federal Reserve Bank of New York notes the median annual earnings for workers aged 22-27 with a bachelor's degree is around $63,000, which can enhance eligibility for favorable refinancing terms.

Federal consolidation merges multiple loans into one with a fixed interest rate based on the weighted average, making repayment simpler but generally not reducing rates. This option preserves access to federal benefits such as income-driven repayment and loan forgiveness programs, which private refinancing could eliminate.

Staying with current federal plans remains wise for those qualifying for Public Service Loan Forgiveness or with low-interest loans. Income-driven repayment options remain available only through federal servicing.

Important considerations include:Do you qualify for a substantially lower interest rate by refinancing?Are you seeking the simplicity of federal consolidation while maintaining federal program benefits?Will income-driven repayment or forgiveness options be forfeited by refinancing?

Borrowers with strong credit and steady income near the $63,000 median often gain most from refinancing. Those unsure about job stability or reliant on federal protections might prefer consolidation or current plan retention.

What steps are involved in the refinance application, approval, and disbursement process?

The refinance application process involves a detailed review of your credit profile, income, and existing student loans. Lenders require documentation such as recent pay stubs, tax returns, and current loan statements to verify income stability and loan details. This assessment determines eligibility and suitable loan terms.

After submitting your application, the lender performs a credit check and validates all provided information. This stage can take from a few days up to two weeks, depending on the lender and how quickly you provide necessary documents. Delays often occur when employment or income requires extra verification.

Approval depends on credit score, debt-to-income ratio, and repayment history. Applicants with credit scores above 680 and steady employment typically receive better interest rates and faster approval. Experts recommend improving your credit score to boost approval chances.

Once approved, you'll receive a new loan agreement detailing interest rates, repayment terms, and fees to review and sign promptly to avoid expiration.

Funds are then disbursed directly to your current loan servicers to pay off existing balances, completing the refinance. This process usually takes 30 to 45 days.

Despite 47% of borrowers having rates above 6%, only 12% of 2020-2023 graduates refinanced their loans, signaling many miss opportunities to reduce costs. Education Data Initiative's "Student Loan Refinancing Statistics" (2025) highlights this trend.

How does refinancing impact monthly payments, payoff timelines, and total interest paid?

Refinancing student loans can substantially reduce monthly payments by lowering interest rates and adjusting loan terms. For instance, borrowers refinancing graduate loans lowered their average interest rate from 7.3% to 4.9%, resulting in notable monthly savings. Reduced interest means less accrual each month, which, combined with repayment timelines tailored to borrower goals, can shorten or extend payoff periods accordingly.

Choosing the right repayment term is crucial: shorter terms increase monthly payments but reduce total interest, while longer terms lower monthly costs but lead to more interest paid overall. Borrowers should consider income stability and future earnings when setting these terms to balance immediate budget needs with long-term savings.

Data from SoFi, cited in Money's "Best Student Loan Refinance Companies," shows that refinancing a $70,000 balance over 10 years can save approximately $13,800 in interest, emphasizing its financial benefits under favorable conditions.

Key points to consider includeLower interest rates help reduce both monthly payments and total interest.Repayment terms impact monthly cash flow and overall interest costs.Refinancing offers flexibility to adjust payments if income changes.Improved credit and income can lead to better rates.New graduates should carefully compare offers and assess their financial stability to optimize loan refinancing outcomes.

What refinance strategies can help new graduates manage risk and protect their credit?

Refinancing student loans can yield significant financial benefits when approached with care. Prioritize lenders offering refinance bonuses, as these can provide immediate cash incentives. For example, the Student Loan Planner's "Best Student Loan Refinance Bonuses" survey reports bonuses up to $1,750 for balances above $200,000, surpassing previous caps. These bonuses help lower debt and improve monthly cash flow.

Choose a repayment plan tailored to your income to avoid missed payments that could harm your credit. Fixed-rate loans lock in predictable monthly payments, reducing the risk caused by interest rate changes. Evaluate loan terms carefully: shorter terms reduce total interest but require higher monthly payments, while longer terms ease monthly costs but increase overall interest. Align your decision with your career path and earning potential.

- Maintain a manageable debt-to-income ratio by refinancing only what you can realistically repay without strain.

- Avoid consolidating federal loans with private refinances to preserve important protections like deferment and income-driven repayment options.

- Monitor your credit score before and after refinancing to catch errors or declines early.

Regular credit reviews help prevent long-term damage, while refinancing with a strong credit profile grants access to better rates and terms. For more guidance on managing these choices effectively, consulting reliable sources can be invaluable.

Other Things You Should Know About

Yes, new graduates can refinance private student loans. Many lenders offer refinancing options specifically for recent graduates to help lower interest rates or reduce monthly payments. Eligibility typically depends on creditworthiness and income, so having a stable job after graduation improves chances of approval.

Refinancing usually does not restrict prepayment on your student loans. Most refinance lenders allow borrowers to pay off loans early without penalties, which can save on interest over time. It's important to verify this with the specific lender before signing the refinance agreement.

Refinancing can positively impact your credit score if you make on-time payments on the new loan. It may also reduce your overall debt-to-income ratio by lowering monthly payments or interest rates. However, applying for refinancing can cause a small, temporary drop due to credit inquiries.

Most student loan refinancing companies do not charge application or origination fees, but it varies by lender. Some lenders may charge late fees or returned payment fees if payments are missed. It is important to review all terms and fees before committing to a refinancing offer.