2026 How to Pay for College If Your Parents Won't Help

Student Finance & Loan Expert

Many students find themselves unable to rely on parental support to cover college expenses. This situation creates a significant barrier to accessing higher education, especially for graduate-level programs and career changes.

Navigating financial options independently can be overwhelming without clear guidance. The challenge lies in identifying feasible funding sources while minimizing future debt burdens.

This article explores various student loan options and financial strategies available to prospective graduate students and working professionals. It aims to equip readers with practical advice to manage education costs effectively and make informed decisions when parental assistance is not an option.

- How can I pay for college completely on my own if my parents won't contribute? Paying solo

- Am I considered an independent student for FAFSA if my parents refuse to help? FAFSA independence

- What grants, scholarships, and work-study options can I get without parent support? Free aid options

- How do federal student loans work when your parents won't share financial information? Federal loans

- When should I use private student loans if my parents won't cosign or pay? Private loans

- How can I estimate how much I can afford to borrow and repay after graduation? Borrowing limits

- What strategies help lower college costs when you're paying without parental help? Cutting costs

- How do repayment plans, deferment, and forbearance work for students on their own? Repayment options

- What happens if I can't pay and my student loans go into default? Loan default

- How can I use refinancing or consolidation later to manage debt I took out alone? Refinancing/consolidation

How can I pay for college completely on my own if my parents won't contribute?

Paying for college without parental help involves strategically combining financial resources, time management, and an understanding of available funding options.

Scholarships and grants based on merit, need, or background remain key, as they do not require repayment. Be sure to complete the Free Application for Federal Student Aid (FAFSA) annually to access federal grants like the Pell Grant and work-study programs.

Student loans can fill financial gaps but should be approached cautiously. Federal loans are preferable because of fixed interest rates and flexible repayment options. It's important to understand borrowing limits and avoid excessive debt.

For students seeking ways to afford college on your own, employment during studies is essential. On-campus jobs, internships, and cooperative education programs often accommodate student schedules and build valuable experience.

Housing choices also affect affordability. Consider cost-effective options such as shared apartments, living at home, or attending community colleges for early credits before transferring.

If working while studying, explore employer tuition assistance programs offering reimbursements or scholarships. Careful budgeting of tuition, supplies, and living costs helps prevent financial shortfalls-track cash flow monthly and adjust spending as needed.

Finally, if you're using loans, investigate whether you can apply student loans for off-campus rent to ease housing costs while managing overall expenses.

Am I considered an independent student for FAFSA if my parents refuse to help?

You are not automatically considered an independent student for FAFSA if your parents refuse to help financially. FAFSA independent status when parents do not contribute is determined by specific criteria set by the U.S. Department of Education.

Most undergraduate students under age 24 are classified as dependent unless they meet conditions such as being over 24, married, a veteran, orphaned, or having legal dependents of their own.

Even if parents do not cooperate, you generally must include their financial information on your FAFSA. Failing to provide it without qualifying as an independent student can delay or reduce your aid eligibility.

Students experiencing abandonment, abuse, or similar extreme circumstances can apply for a dependency override through their school's financial aid office to be considered independent. This process requires documentation and professional evaluation.

FAFSA independent status affects Pell Grant eligibility. Dependent undergraduates must report parent income and can receive a maximum Pell Grant of $7,395, while independent students with qualifying need can receive the same amount without parent income reporting, according to Federal Student Aid.

To navigate parental non-cooperation, consider these steps:

- Discuss your situation with your school's financial aid office.

- Apply for a dependency override if abuse, abandonment, or similar conditions apply.

- Look into alternative aid like private scholarships or student loans requiring your own credit, such as federal student loans without parents.

Knowing how to qualify as an independent student for FAFSA without parental support helps maximize aid and avoid application issues when parents don't provide financial help.

What grants, scholarships, and work-study options can I get without parent support?

Students without parental support should focus on federal grants designed for independent applicants. The Pell Grant offers awards up to $7,395 based on financial need, without requiring parental income information.

Additionally, Federal Supplemental Educational Opportunity Grants (FSEOG) can provide extra aid, though eligibility depends on Pell Grant qualification. State and institutional grants also exist, many targeting independent students, veterans, or non-traditional applicants. These often consider your own income rather than your parents'.

Merit scholarships remain accessible without parental involvement and often reward academic achievement, special talents, or community service. Civic groups, employers, or associations linked to your major regularly offer such scholarships.

Use specialized platforms to find scholarships and college grants for adults tailored to independent or returning students.

Work-study programs available without parental financial information provide federally funded part-time jobs on or off campus. These roles pay at least minimum wage and help cover educational expenses with no loan repayment required. Selecting "independent" on the FAFSA boosts your chances for work-study funding.

Starting at a public in-state college can be financially smart. The average published in-state tuition was $11,790, significantly less than private nonprofit colleges, making it easier to combine affordable tuition with grants and work-study to finance your education.

How do federal student loans work when your parents won't share financial information?

Federal student loans enable dependent students to borrow from the government even without submitting parental financial information, but certain steps are necessary. When parents refuse or cannot provide their details, students must still file the Free Application for Federal Student Aid (FAFSA).

If parental info is missing, an appeal process called a "dependency override" or special circumstances review allows the financial aid office to evaluate the student's independent status using documented evidence.

In cases of applying for federal student aid without parental income information, the most accessible option is the Direct Unsubsidized Loan, which does not require parental data and can reach up to $5,500 for first-year undergraduates.

The Direct Subsidized Loan, dependent on financial need and parental info, may be unavailable. Graduate and professional students are automatically classified as independent borrowers and don't face these restrictions.

Students lacking parental details should:

- Contact their institution's financial aid office to request a dependency override.

- Submit verification from counselors, social workers, or courts if applicable.

- Consider alternative funding like private loans when federal aid is limited.

Because supplementing student loans with grants and scholarships is crucial, it's worth noting that 72% of families rely on these funds to cover roughly 18% of college expenses. This support helps reduce loan dependence and debt, especially when parental help isn't available.

Those looking for the best options to manage or refinance loans further can explore resources featuring the best bank student loan refinance rates. Understanding how federal student loans work without parents' financial details can inform better financial decisions throughout college.

When should I use private student loans if my parents won't cosign or pay?

Federal student loans should be your primary funding source before considering private student loans.

Independent undergraduates can borrow up to $57,500 in Direct Subsidized and Unsubsidized Loans, nearly double the $31,000 limit for dependent students, and do not require a cosigner. This higher limit can provide significant financial relief if you qualify as independent.

Private loans are best used only after you have exhausted federal options and other financial aid such as grants, scholarships, and work-study. Consider private loans when:

- You've reached your federal loan borrowing limits.

- Your financial aid package doesn't cover all tuition, fees, and living expenses.

- Grants, scholarships, and work-study funds fall short of your needs.

Choosing a private loan without a cosigner often results in higher interest rates and tougher credit requirements. Carefully evaluate your credit score and income before proceeding. Some lenders offer private loans that do not require cosigners, but they usually cost more.

If, for example, you've maxed out your $57,500 federal loan but still need $10,000 to cover expenses, a no-cosigner private loan may be necessary. Alternatively, explore options like income-share agreements or institutional payment plans first.

Federal loans provide flexible repayment, deferment, and lower fixed interest rates, so prioritize them. Use private loans only when federal aid and other resources have been fully utilized and you understand the long-term financial implications.

How can I estimate how much I can afford to borrow and repay after graduation?

Estimate your borrowing capacity by comparing your expected postgraduation income to typical student loan repayment limits. Financial experts advise that total student loan debt should generally stay below 1.5 times your starting annual salary. For instance, if your first salary is $40,000, borrowing no more than $60,000 helps keep repayments manageable.

Online loan calculators can help you model monthly payments with different interest rates and repayment terms. Assess whether these payments fit your budget by accounting for living expenses and other debts. Income-driven repayment plans offer flexibility by adjusting payments based on your income.

Working during school can reduce the amount you need to borrow. According to the National Center for Education Statistics, 41% of full-time undergraduates worked an average of 22 hours weekly. Part-time jobs or tuition-reimbursement roles help lower your future debt burden.

Also, remember that interest often accrues during school, especially on unsubsidized loans, increasing total debt. Accurately estimating borrowing helps protect your financial stability and avoid excessive debt after graduation.

What strategies help lower college costs when you're paying without parental help?

Attending in-state public universities is a cost-effective way to reduce college expenses without parental support, as tuition is much lower than at private schools. Starting at community colleges to complete general education credits before transferring can also save money.

Maximize use of all eligible federal grants and scholarships since these funds don't require repayment. Participating in work-study programs offers part-time jobs that help cover costs while gaining professional experience.

Manage student loans carefully to keep debt manageable. Prioritize federal Direct Subsidized and Unsubsidized Loans, which generally have lower interest rates and more flexible repayment options than private loans.

According to the College Board's Trends in Student Aid 2024, private loans accounted for only 7.8% of education debt but carried 2-5 percentage points higher interest rates, making them riskier.

Adopt strict budgeting and consider living arrangements like staying at home or sharing housing to cut expenses. Taking summer or heavier course loads can shorten time to degree and reduce overall tuition.

How do repayment plans, deferment, and forbearance work for students on their own?

Repayment plans for federal student loans vary to help borrowers manage monthly costs. The standard plan requires fixed payments over a decade, while income-driven plans adjust payments based on a percentage of discretionary income, often lowering monthly amounts.

Deferment allows a temporary pause on payments without accruing interest on subsidized loans, useful during unemployment or continued schooling. Forbearance also pauses payments but interest continues accumulating, increasing the total balance owed.

Borrowers should contact their loan servicer directly to apply for these options. Eligibility for deferment generally depends on criteria like economic hardship or active enrollment, while forbearance is usually granted more flexibly but for shorter time frames. Both options help prevent loan default but can increase the overall repayment amount if used extensively.

Key strategies include:

- Confirming loan type to understand if interest accrues during deferment or forbearance.

- Choosing income-driven repayment to align payments with current income.

- Using deferment for short-term payment relief when interest-free.

- Reserving forbearance for urgent, temporary needs when deferment isn't available.

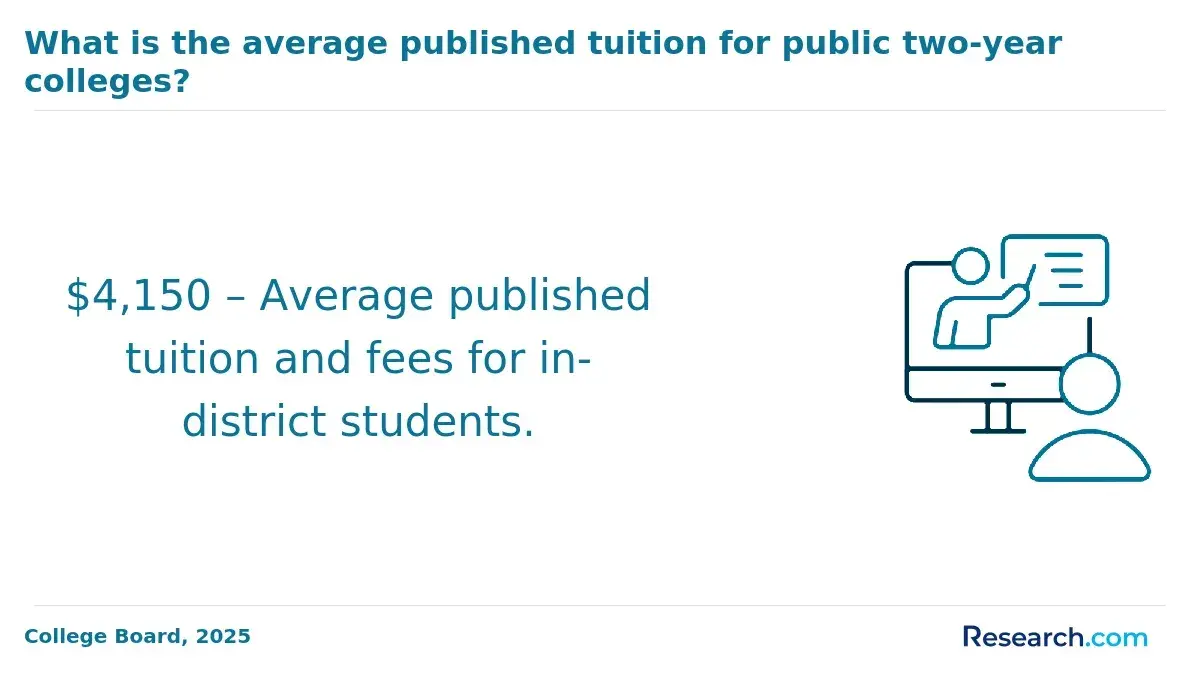

Attending a public two-year college significantly lowers upfront tuition costs, averaging $3,990 yearly, about one-third the cost of public four-year institutions according to the College Board. Starting at community colleges can reduce loan dependency and support more manageable repayment options after transferring.

What happens if I can't pay and my student loans go into default?

Missing student loan payments leads to serious financial consequences. After a missed payment, your loan servicer marks your account delinquent, and within 270 days, the loan defaults.

Default can trigger the full loan balance due immediately, legal action, wage garnishment, and tax refund offsets. Your credit score will be severely damaged, staying impaired for up to seven years, which affects housing, jobs, and future credit opportunities.

Federal financial aid eligibility may be revoked, limiting access to grants and new loans, which complicates continuing or returning to school. Collection fees often add to your total debt, increasing your financial burden.

Options to remove default status include rehabilitation or loan consolidation:

- Rehabilitation requires making nine on-time payments within ten months.

- Consolidation replaces defaulted loans with a new loan but has eligibility criteria.

Communicating with loan servicers is crucial. Income-driven repayment plans adjust your monthly payments based on earnings, helping reduce default risk. Working part-time or delaying college to save money can help manage repayments.

According to a Federal Reserve Report on the Economic Well-Being of U.S. Households in 2023, 26% of high school graduates who delayed college cited working and saving as their main reason, reducing future loan risks.

Ignoring default leads to escalating penalties and loss of financial flexibility. Early action and informed repayment strategies can protect your credit and maintain educational options.

How can I use refinancing or consolidation later to manage debt I took out alone?

Refinancing and consolidation can help manage student loan debt by lowering interest rates, reducing monthly payments, or combining multiple loans into one. Refinancing replaces your current loans with a new one at a potentially lower interest rate, saving money and simplifying repayment.

Consolidation combines federal loans into a single loan with one payment, often extending the repayment period to lower monthly costs but possibly increasing total interest paid.

Private lenders offering refinancing typically require good credit and steady income. For example, refinancing several loans with rates of 6% to 8% to a single loan at 4% can significantly decrease monthly payments and overall interest. This option is especially useful after graduation when income stabilizes.

Federal loan consolidation provides access to income-driven repayment plans and forgiveness programs but may reset forgiveness progress if you switch to a Direct Consolidation Loan.

Consider your individual loan terms, credit score, and job stability before deciding. The U.S. Bureau of Labor Statistics reports that bachelor's degree holders aged 25-34 earn a median of $65,000, supporting favorable refinancing options compared to high school graduates earning $40,000.

Review federal protections carefully since private refinancing can mean losing benefits like deferment and income-driven plans.

Other Things You Should Know About How to Pay for College If Your Parents Won't Help

Yes, you can apply for federal student loans without a credit check, as they are generally based on financial need rather than credit history. However, private student loans usually require a credit check or a cosigner with good credit. This makes federal loans more accessible for students who do not have an established credit record.

Taking out student loans on your own means you are solely responsible for repayment, even if your parents do not assist. This can affect your credit score if payments are missed and may limit your borrowing options. However, it also allows you to build credit independently and control your own loan terms.

Student loans do not usually affect your eligibility for grants and scholarships, which are based on financial need or merit. However, excessive loan borrowing can impact your overall financial aid package. Schools might reduce loan offers if you request less funding, so it's important to balance loans with other aid carefully.

There are federal loan limits based on your year in school and enrollment status, which restrict how much you can borrow each year and in total. Private lenders may set their own limits based on creditworthiness. You cannot have unlimited loans; responsible borrowing within set limits is crucial to avoid excessive debt.