2026 Best Student Loans for Transfer Students

Student Finance & Loan Expert

Transferring to a new institution often complicates existing financial aid, leaving many students uncertain about their loan options. Confusion arises from differing eligibility criteria, loan limits, and repayment terms after transfer. This uncertainty can delay enrollment or lead to accumulating unnecessary debt. Understanding the best student loans available specifically for transfer students is essential to making informed decisions and minimizing financial stress. This article reviews key loan types and lenders tailored to the needs of transfer students, aiming to provide clarity and practical guidance for securing affordable and suitable financing for continued education.

- What types of student loans are available specifically for transfer students? What types of student

- How can transfer students maximize federal loans before considering private options? How can transfer students

- How do you compare and choose the best student loan when changing schools? How do you compare

- Do transfer students need to submit a new FAFSA and how is aid recalculated? Do transfer students need

- What are typical interest rates, fees, and borrowing limits for transfer student loans? What are typical interest

- How do enrollment status and transferred credits affect loan eligibility and dependency status? How do enrollment status

- What repayment options work best for transfer students juggling loans from multiple schools? What repayment options work

- Can transfer students qualify for loan forgiveness or discharge, and how does school type matter? Can transfer students qualify

- When should transfer students refinance or consolidate, and what risks should they avoid? When should transfer students

- How do payment plans, employer tuition benefits, and scholarships reduce borrowing for transfers? How do payment plans,

What types of student loans are available specifically for transfer students?

Transfer students seeking funding have access to specific federal and private student loans for transfer students that accommodate their unique academic situations. Federal Direct Loans, including Direct Subsidized and Unsubsidized Loans, remain the primary options. These loans offer fixed interest rates and flexible repayment plans, which suit transfer students who often experience changes in eligibility due to credit hour transfers. Graduate transfer students or parents of undergraduates can also access Direct PLUS Loans, which provide funds beyond standard limits but require credit approval.

Private student loans serve as an alternative when federal loan limits fall short. However, these loans usually have variable interest rates and stricter creditworthiness criteria. Transfer students should compare loan terms carefully since some lenders may not recognize all prior credits, potentially limiting the loan amount.

State-specific loan programs may prioritize transfer students by offering competitive rates or forgiveness programs favoring in-state transfers, helping to reduce debt burdens. Additionally, some institutions provide their own loan programs or payment plans to cover gaps between federal aid and tuition.

Awareness of aggregate loan limits is vital. The 2024 National Student Clearinghouse report showed that bachelor's degree earners who transferred multiple times borrowed a median 19% more than non-transfer peers with similar backgrounds. Managing loan amounts, consolidation, or refinancing can ease this burden.

For those looking for the best loan options for transfer students in the US, it is helpful to review resources like federal loans for dental school to better understand federal loan offerings and alternative options.

How can transfer students maximize federal loans before considering private options?

Transfer students should prioritize federal student loan options for transfer students and fully exhaust federal aid before considering private loans, which typically have higher interest rates and fewer borrower protections. To maximize federal aid, complete the Free Application for Federal Student Aid (FAFSA) promptly every academic year. Direct Subsidized Loans are particularly advantageous since they don't accrue interest while you are enrolled at least half-time, making them the most cost-effective federal borrowing choice.

Students can maximize federal lending by carefully monitoring aggregate loan limits: undergraduate dependent students face a combined subsidized and unsubsidized loan cap of $31,000, while independent students have a $57,500 limit. Be sure to check prior borrowing through the National Student Loan Data System (NSLDS) to avoid exceeding these limits, especially after transferring.

Federal Parent PLUS Loans are another valuable resource if parental support is available, offering lower interest rates than many private loans and flexible repayment options. Transfer students should also seek federal grants and work-study opportunities to reduce borrowing needs. Consulting your new school's financial aid office early helps confirm eligibility and preserves federal loan benefits.

The College Board's "Trends in Student Aid 2024" reveals that 92% of undergraduates rely on federal loans, whereas only 14% use private loans, which make up 8% of total loan volume due to larger borrowing amounts. Such data highlights the importance of strategies to maximize federal aid before private loans to keep debt manageable. For students facing credit challenges, exploring student loans for bad credit borrowers may provide additional guidance.

How do you compare and choose the best student loan when changing schools?

When transferring schools, comparing student loan options when changing schools can save you money and stress. Federal student loans typically offer lower interest rates and flexible repayment plans compared to private ones. Make sure your new school participates in federal loan programs to keep eligibility for these benefits. Fixed interest rates help limit future increases, while variable rates may start lower but can rise over time.

Check if you can consolidate or refinance existing loans to lower monthly payments. Refinancing might cut your interest rate but could mean losing federal protections like income-driven repayment plans. Some private lenders require continuous enrollment at the same institution, so look for lenders who support transfer students.

Loan limits can change after transfer. Federal Direct Subsidized and Unsubsidized Loans have cumulative caps, so account for any lost credits or additional semesters needed. A Government Accountability Office report noted students losing more than a semester's credits during transfer took on about 11% more debt and were 23% less likely to graduate, emphasizing careful planning.

For the best student loans for transfer students in the United States, seek advice from financial aid offices on eligibility and repayment options. Use online tools to estimate repayment costs based on different loan terms. You may also explore grants for adults going back to school to reduce debt while completing your degree.

Do transfer students need to submit a new FAFSA and how is aid recalculated?

Transfer students must submit a new Free Application for Federal Student Aid (FAFSA) for each academic year they seek financial aid, including after transferring schools. This answers the common question: do transfer students need to submit a new FAFSA form? Since the FAFSA is school-specific, your new institution requires an updated form to evaluate your eligibility, and without it, federal financial aid is typically unavailable for the new school year.

Financial aid is recalculated when you transfer based on the new school's cost of attendance (COA), which can significantly affect your total aid package and loan limits. This addresses how financial aid is recalculated for transfer students. For instance, transferring from a community college to a public four-year university often raises tuition, but starting at a two-year college before transferring can save about $9,000-$11,000 for a bachelor's degree, according to the College Board's "Trends in College Pricing 2024."

Your Expected Family Contribution (EFC) remains consistent during the award year but applies separately to each institution's COA. Institutional aid won't necessarily transfer and is subject to re-evaluation by the new school.

Key tips for transfer students include submitting FAFSA early, contacting financial aid offices at both schools, and notifying lenders to update enrollment information for any existing loans. For those considering refinancing options, consult the best banks for student loan refinancing.

- Submit FAFSA early to the new school's financial aid office.

- Speak with financial aid offices at both your current and prospective schools.

- Notify lenders about your school change to maintain accurate loan statuses.

What are typical interest rates, fees, and borrowing limits for transfer student loans?

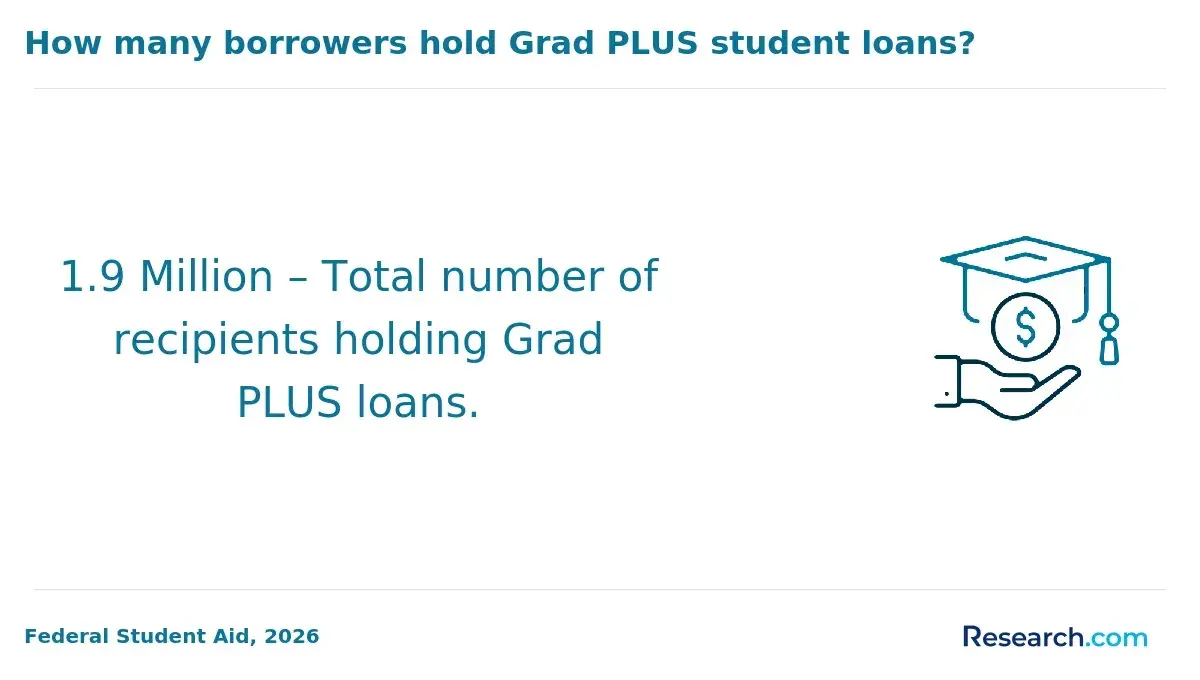

Transfer student loans feature varying interest rates depending on the loan type. Federal Direct Subsidized and Unsubsidized Loans offer fixed rates generally between 5.5% and 6.0% for undergraduates. In contrast, Parent PLUS and Grad PLUS Loans have higher fixed rates, typically near 7.5% to 8.5%. Private loans can range broadly, from about 4% for borrowers with excellent credit to more than 12% for those with lower scores.

Fees also differ. Federal loans usually include origination fees from 1% to 4.5%, deducted before funds are disbursed. Private lenders may charge application or origination fees but often waive them for transfer students with strong credit or a cosigner.

Borrowing limits vary by academic year and loan type. First-year undergraduates using Federal Direct Loans are limited to $5,500 annually, increasing up to $7,500 for upperclassmen. Aggregate federal undergraduate loan limits cap at $31,000 for dependent students. Parent PLUS and private loans generally offer higher or unlimited borrowing potential based on credit and the cost of attendance.

- Federal loans usually provide lower interest rates and greater borrower protections.

- Private loans often allow higher amounts but carry higher interest rates and fewer flexible repayment options.

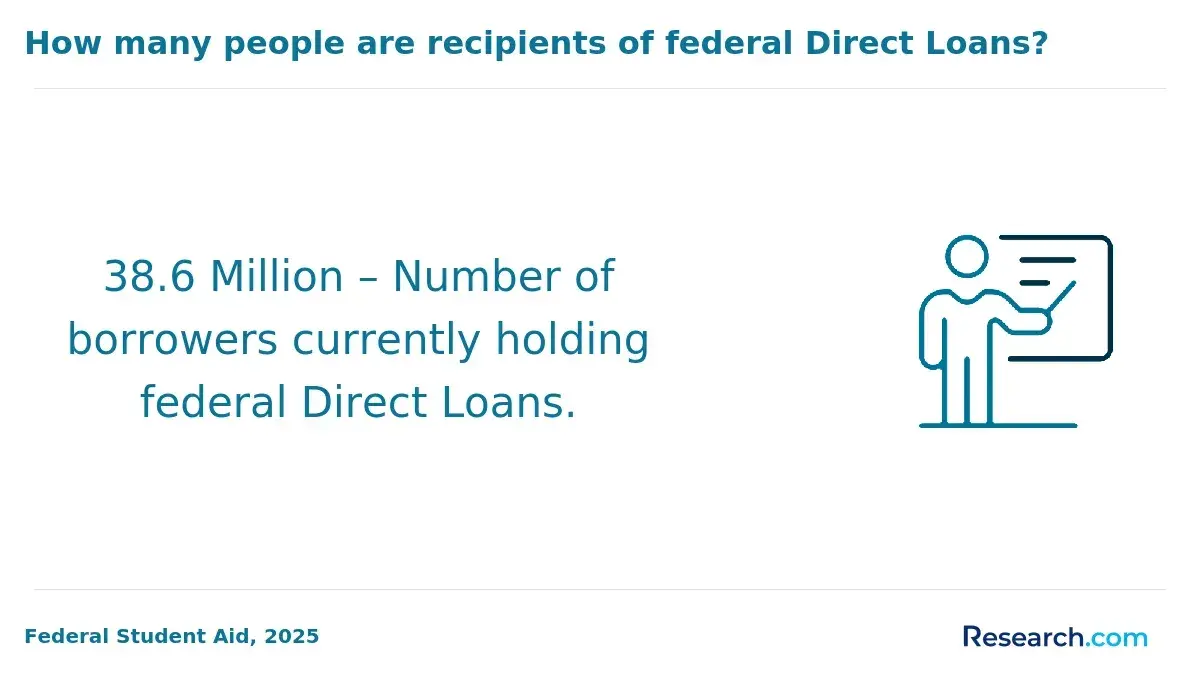

- Data from the U.S. Department of Education's 2024 portfolio shows Direct Subsidized and Unsubsidized Loans represent about 67% of federal borrowers, while Parent and Grad PLUS Loans account for nearly 30% of outstanding federal debt despite fewer borrowers.

How do enrollment status and transferred credits affect loan eligibility and dependency status?

Loan eligibility for transfer students depends heavily on enrollment status and how transferred credits are evaluated. Federal student loans require students to be enrolled at least half-time. If transferring credits lowers your course load below this, you may lose eligibility. For example, transferring many credits often means enrolling in fewer classes, which can reduce loan options.

Transferred credits also affect federal loan dependency status. Students with enough credits-usually 24 or more-toward their degree may be considered independent borrowers, increasing borrowing limits and removing the need for a parent or cosigner.

Private loans tend to have stricter requirements, with lenders focusing on credit history. Over 90% of new private undergraduate loans involve cosigners, according to a report by MeasureOne. Having a creditworthy cosigner can lower interest rates by 2-3 percentage points.

Key points to consider include:

- If enrollment drops below half-time after credit transfer, confirm your eligibility with your school's financial aid office before applying.

- Transferred credits can reduce required courses, impacting loan eligibility and dependency status.

- A creditworthy cosigner significantly improves private loan terms.

Maintaining ongoing communication with financial aid advisors is essential for navigating these changes and optimizing loan opportunities as you leverage transferred credits.

What repayment options work best for transfer students juggling loans from multiple schools?

Transfer students managing loans from multiple schools benefit from repayment options that simplify payments and reduce stress. Federal Direct Consolidation Loans allow borrowers to combine multiple federal loans into a single monthly payment, easing administrative tasks and providing access to alternative repayment plans tied to federal programs.

Income-Driven Repayment (IDR) plans such as Income-Based Repayment (IBR) or Pay As You Earn (PAYE) adjust monthly payments based on income and family size. This flexibility is especially helpful for transfer students whose financial situations can change, preventing payments from becoming unmanageable while juggling debts from several institutions.

Graduated repayment plans offer low initial payments that gradually increase over time, aligning well with expectations of career and income growth. Fixed repayment plans provide predictable payments but may strain budgets if loan interest rates are high. According to the Federal Reserve's 2025 Report on the Economic Well-Being of U.S. Households, borrowers with interest rates above 7% were nearly twice as likely to feel financially worse off than those with loans under 5% interest.

For private loans from various schools, refinancing can consolidate debt at lower rates but often eliminates federal protections such as eligibility for IDR plans and loan forgiveness programs. Transfer students should carefully weigh these benefits and risks when considering refinancing.

- Federal Direct Consolidation Loans simplify multiple federal loans.

- Income-Driven Repayment plans adjust payments to income.

- Graduated plans support rising income scenarios.

- Refinancing private loans can lower rates but may remove protections.

Can transfer students qualify for loan forgiveness or discharge, and how does school type matter?

Federal student loan forgiveness programs can benefit transfer students, depending on the loan type and the institution they attend. Direct Loans may be eligible for Public Service Loan Forgiveness (PSLF) if the borrower works full-time for qualifying employers and completes 120 qualifying payments. This eligibility is maintained even if the student transferred schools during their degree. Private student loans, however, rarely offer forgiveness or discharge options, making federal loans a more favorable choice for many borrowers.

Eligibility for federal forgiveness depends heavily on the school's accreditation. Loans from accredited institutions qualify for these programs, and transferring between regionally or nationally accredited schools generally does not affect eligibility. Attendance at non-accredited or for-profit schools, though, can limit discharge options.

Additional loan discharges like Total and Permanent Disability (TPD) discharge and Closed School Discharge are available but require federal loans to be in good standing. Death discharge applies regardless of school type.

- A 2025 Sallie Mae update reveals 86% of undergraduate private loan borrowers used a cosigner.

- Cosigned private loans approve at rates over three times higher than solo applications.

- This indicates transfer students without cosigners may face challenges securing private loans.

When should transfer students refinance or consolidate, and what risks should they avoid?

Transfer students with multiple loan types, especially private loans obtained after switching schools, should consider refinancing or consolidating their student loans to lower interest rates and simplify payments. Refinancing works best for those with a strong credit profile and stable income, while federal loan consolidation combines balances into a single loan, possibly extending repayment terms and lowering monthly payments, though it may increase total interest paid.

Beware of losing federal loan benefits when refinancing federal loans into private ones, such as eligibility for Income-Driven Repayment plans or Public Service Loan Forgiveness. Refinancing too soon may also forfeit transfer-specific scholarships, which have seen a 28% increase recently. Applying for these awards can reduce your loan balances before refinancing or consolidation.

Avoid refinancing if your credit is weak or if interest rates are high. Waiting to improve credit and comparing offers can lead to better terms. Those experiencing federal loan hardship should carefully evaluate refinancing since federal loans often provide forbearance options unavailable with private loans. Some federal consolidation programs may reset repayment benefits and forgiveness progress, so reviewing contract terms carefully is crucial.

Assess your loan types, credit status, and financial goals thoroughly. Consulting a financial advisor can help determine if refinancing or consolidation fits your long-term repayment plan.

How do payment plans, employer tuition benefits, and scholarships reduce borrowing for transfers?

Structured payment plans, employer tuition benefits, and scholarships play a crucial role in reducing the loan amounts transfer students need to borrow. Payment plans that break tuition into semesterly or monthly installments allow students to avoid large upfront loans and minimize early interest accumulation. This helps keep overall debt lower by spreading costs over time.

Employer tuition benefits provide financial assistance by covering education costs for eligible employees, often applicable for part-time or full-time workers. Some employers offer tuition reimbursement after course completion, encouraging students to manage borrowing wisely and reduce loan reliance.

Scholarships are especially valuable for transfer students, addressing challenges linked to transferring credits or adjusting curricula. These awards require no repayment and can offset tuition, fees, or living expenses. Applying early and broadly can improve chances of securing funding.

Research from the Federal Reserve highlights that 56% of borrowers without a budgeting or repayment plan felt they borrowed beyond their means, compared to just 32% who planned ahead. This data emphasizes the financial benefits of careful planning through payment options, employer benefits, and scholarships.

- Explore institutional payment plan options available to transfer students

- Consult your employer about tuition support programs

- Apply aggressively for transfer-specific scholarships early

Combining these strategies can limit loan amounts and enhance repayment success for transfer students facing unique financial challenges.

Other Things You Should Know About

Yes, transfer students can use student loans to cover non-tuition expenses such as housing, textbooks, transportation, and other education-related costs. Both federal and private student loans typically allow disbursements beyond just tuition and fees, helping students manage their overall college budget while transitioning schools.

Transfer students generally need to submit their current enrollment verification, proof of previous academic credits, and updated financial information. Lenders may also require transcripts from the previous institution and may ask for additional documentation to confirm eligibility and loan limits specific to the new school and academic program.

Federal student aid has aggregate loan limits that apply regardless of how many schools a student attends. Transfer students must keep track of their combined borrowing from all institutions to avoid exceeding these limits, as doing so can affect eligibility for future federal loans and grant aid.

Transferring schools does not reset the grace period on federal student loans. The grace period typically begins after a student graduates, drops below half-time enrollment, or leaves school altogether. Transfer students should confirm their enrollment status with their loan servicer to understand when repayment must begin.