2026 Can Student Loans Pay for Transportation?

Student Finance & Loan Expert

Imagine a student preparing to begin graduate school who needs reliable transportation for commuting but faces tight financial constraints. The cost of a vehicle or public transit can add significant strain to an already limited budget. For prospective students wondering if student loans can legally and practically cover such transportation expenses, uncertainty often causes confusion. Understanding how student loans can be allocated beyond tuition and fees is crucial. This article explores the eligibility of transportation costs under student loan funding and provides clear guidance to help borrowers make informed financial decisions related to their educational journey.

- Can student loans be used to pay for transportation and commuting costs? Loan transportation

- What types of transportation qualify as allowable education expenses under student aid rules? Eligible transport

- How do colleges define and calculate transportation in the student cost of attendance? COA transport

- Are car payments, gas, insurance, and parking covered by federal student loans? Car expenses

- Can private student loans offer more flexibility for transportation-related costs? Private flexibility

- How do financial aid refunds work if you plan to use them for transportation? Refund use

- What documentation or proof of transportation expenses might schools or lenders require? Expense proof

- How should you decide how much to borrow for transportation without overborrowing? Borrow amount

- What are safer alternatives to borrowing student loans for transportation needs? Alternatives

- How do transportation choices affect total student loan debt and repayment outcomes? Transport impact

Can student loans be used to pay for transportation and commuting costs?

Student loans can cover transportation expenses when these costs are necessary for attending school. The U.S. Department of Education allows loan funds to pay for reasonable travel expenses related directly to enrollment, including public transit passes, gas, parking fees, and vehicle maintenance if a personal vehicle is required.

Eligible transportation costs are part of the broader category of "education expenses," which also includes tuition, books, and housing. For example, students who commute regularly or live off-campus may use loans for monthly bus passes or mileage expenses. Trips required between campuses or clinical sites can also qualify. Using student loan funds for commuting costs should be realistic and documented to avoid scrutiny, as expenses not tied to academic need, like leisure travel or non-essential vehicles, are not eligible.

Loan disbursements typically arrive as lump sums through financial aid packages, so students must plan their budgets to allocate funds for transportation. Some schools offer guidance or stipends to help cover these commuting costs within financial aid counseling. In the 2024-25 academic period, students and parents borrowed $102.6 billion in federal and nonfederal loans for postsecondary education, down significantly from previous years, reflecting ongoing coverage of broad costs including transport (College Board, Trends in Student Aid).

For students exploring whether student loans for cost of living can help, transportation can be included with proper documentation and alignment with educational needs.

What types of transportation qualify as allowable education expenses under student aid rules?

Student loans can cover various transportation expenses that qualify under federal student aid regulations when they are necessary for education. Qualified transportation costs under student aid guidelines typically include costs directly related to commuting between home and school or travel needed to participate in academic activities.

Examples of student loan coverage for transportation expenses include:

- Public transit fares such as buses, subways, or trains used during the academic term.

- Fuel and parking fees if using a personal vehicle for travel to campus.

- Rideshare service costs when affordable public transit is unavailable.

- Travel expenses required to attend internships, clinical placements, or off-campus educational programs.

- Occasional trips between multiple campuses within a school system.

Transportation costs purely personal or recreational are generally not covered by student loans. Documenting transit expenses, fuel receipts, or parking permits strengthens the justification for allocating loan funds toward transportation needs.

The average full-time community college student spends about $1,760 annually on transportation, nearly half the yearly tuition at public two-year colleges. This highlights the importance of budgeting for such expenses carefully. For more insight into student borrowing options that include support for these costs, consider resources like ascent student loans.

Transportation expenses must be reasonable, educationally required, and directly linked to accessing academic programs rather than incidental travel to qualify under student aid rules.

How do colleges define and calculate transportation in the student cost of attendance?

Colleges factor transportation into the student cost of attendance (COA) as anticipated expenses for travel between home and campus and local travel during enrollment. This covers costs like public transit passes, fuel, parking permits, vehicle upkeep, or occasional airfare if the school is far from a student's permanent residence. Institutions use various college transportation cost calculation methods, including standardized allowances based on geography or individualized estimates reflecting actual commuting distances and transportation modes. For instance, students in urban areas using public transit will have different budgets than rural students who commute by car.

Transportation costs are part of the federally regulated COA, which affects the total amount students may borrow through federal student loans. Around 28.6% of undergraduates use federal loans, highlighting how student loan coverage for transportation expenses is often necessary. Financial aid offices add transportation estimates to tuition and housing costs to compile the COA.

When applying for financial aid, students should document their real transportation needs, as aid officers may adjust budgets accordingly. Those living on campus typically face lower transportation costs compared to commuters or remote learners.

Students aiming to manage their loans wisely should explore options like a student loan refinance bonus to reduce overall debt and better handle transportation expenses within their loan budgets.

Are car payments, gas, insurance, and parking covered by federal student loans?

Federal student loans explicitly cover educational expenses such as tuition, fees, books, supplies, and sometimes room and board, but they do not directly cover car payments, gas, insurance, or parking. Students may use portions of their federal loan disbursements for transportation-related expenses only if they are reasonable and deemed necessary to support enrollment and attendance. This means there is no separate federal loan disbursement exclusively for car expenses, although transportation costs may be included in the cost of attendance (COA) budget set by your school.

Cost of attendance calculations often include a conservative allowance for transportation, which can cover commuting or local travel. If your COA includes transportation, federal student loans can indirectly cover that portion. For example, if your school's budget accounts for a $1,000 transportation expense, you may borrow up to that amount within your loan limits. However, actual auto loan payments, insurance premiums, and parking fees must fit reasonably within that transportation allowance, reflecting how federal student loans for car expenses have strict restrictions.

Many students seek private loans to cover additional transportation costs beyond official COA allocations. The average total student loan balance is higher when including private loans, which often fill gaps in non-tuition expenses like car loans and maintenance. When considering whether student loans cover gas and insurance costs, private financing tends to offer more flexibility but fewer protections than federal loans.

Students financing vehicles through loans should assess repayment terms carefully, especially since federal loans typically offer more flexible repayment options. For more detailed guidance on managing education expenses, see how to pay for nursing school.

Can private student loans offer more flexibility for transportation-related costs?

Private student loans offer greater flexibility for transportation-related expenses than federal loans, which are generally limited to direct educational costs like tuition and supplies. Private lenders often permit using loan funds for commuting fees, vehicle maintenance, or even purchasing a reliable car necessary for attending classes or internships.

Transportation costs are significant; the average U.S. household spends about $750 monthly on transportation-over three times the typical student loan payment of $242 per month, according to the Postsecondary National Policy Institute. This highlights the importance of including transportation funding for students managing tight budgets.

Private loans can accommodate different transportation needs, such as:

- Students in rural areas needing funds for car purchase and upkeep due to limited public transit.

- Urban students requiring monthly transit passes or ride-share credits.

- Graduates covering relocation and commuting costs for jobs distant from campus.

However, this flexibility comes with higher interest rates and fewer consumer protections than federal loans. Borrowers should carefully evaluate whether using private loans for transportation expenses increases long-term financial strain. Consulting financial advisors and budgeting carefully are crucial steps to ensure these loans meet immediate needs without creating repayment difficulties.

How do financial aid refunds work if you plan to use them for transportation?

Financial aid refunds occur when the aid awarded exceeds tuition and fees, allowing students to use the surplus for transportation costs such as public transit passes, gas, vehicle maintenance, ride-sharing, and parking permits. After tuition is covered, schools typically disburse these remaining funds via direct deposit or prepaid cards.

Unlike direct campus transit programs, like the U-Pass at St. Louis Community College offering unlimited local rides valued at about $1,760 annually, managing transportation costs through financial aid refunds requires careful budgeting by the student. Loan refunds increase debt because they must be repaid with interest, while grants and scholarships do not but may have limited availability.

- Check your school's financial aid office for disbursement schedules and methods.

- Estimate monthly transportation expenses to avoid overspending.

- Compare campus transit aid programs with independent transportation options financed through refunds.

- Maintain detailed records of transportation spending for budgeting and audits.

Many institutions restrict the use of refunds for non-educational purposes, so verify with your financial aid office if transportation costs qualify. Smart use of refunds combined with campus aid programs can reduce student transportation expenses by over $1,700 annually.

What documentation or proof of transportation expenses might schools or lenders require?

Documentation is crucial when verifying transportation expenses for student loans. Accepted proofs often include receipts for transit passes, monthly bus or train tickets, and toll invoices. For those commuting by car, mileage logs showing daily travel between home and campus, fuel receipts, and maintenance bills are commonly required. Some institutions may also request car insurance policies and registration documents to confirm ownership and associated costs.

Lenders and schools might ask for sworn affidavits or detailed monthly budget statements if transportation costs surpass typical amounts. Students who rely on rideshare services or taxis due to disability or limited public transit can submit invoices or payment confirmations as valid evidence.

The verification process varies: community colleges generally require less detailed proof than four-year universities, where financial aid officers carefully review expense claims. Many schools cap loan amounts for transportation based on reasonable, documented expenses.

Accurate record keeping is essential since exaggerated or unverified expenses can cause loan delays or denials. Early consultation with the financial aid office helps clarify specific documentation requirements.

When deciding whether to borrow additional funds for transportation, keep in mind trends showing an average total student loan debt of about $29,560 among bachelor's degree recipients, down from $35,600 a decade ago, signaling cautious borrowing despite rising commute costs.

How should you decide how much to borrow for transportation without overborrowing?

Calculate your actual transportation costs carefully before borrowing student loan money. Include daily commuting fares, fuel, maintenance, insurance, and potential repairs. Use past spending records or local transit rates instead of guessing maximum expenses. For instance, if transit costs are about $100 monthly and you attend school for 10 months, plan for roughly $1,000 annually.

Think of transportation within your full budget, which covers tuition, housing, and food. Avoid borrowing extra "just in case," as overborrowing increases debt and repayment pressure. U.S. student loan debt reached $1.73 trillion, with 10.0% of federal student loans delinquent, illustrating how combined expenses can affect graduation chances (Education Data Initiative, Student Loan Debt Statistics 2026).

Consider alternative transportation. Walking or biking lowers borrowing needs considerably. If a vehicle is essential, opt for affordable, reliable used cars and include insurance costs accurately. Remember, loan funds spent on transportation contribute to your monthly repayments after graduation.

Prioritize loans for core academic expenses and cover transportation through savings, scholarships, or part-time work when possible. Excess borrowing raises your debt burden and delinquency risk unnecessarily.

- Calculate actual transportation expenses carefully

- Include in overall budget with non-transportation costs

- Explore alternatives like biking or walking

- Borrow only for needs, not extra

- Loan money spent impacts future repayments

What are safer alternatives to borrowing student loans for transportation needs?

Students should seek safer alternatives to borrowing student loans for transportation to avoid adding to their debt. Public transit support programs can save an average full-time community college student nearly $1,800 per year, covering typical transportation costs and reducing the need for extra funding (Association of Community College Trustees, "Transportation Costs in Student Living Expenses").

Some cost-saving options include:

- Using campus shuttle services, often free or low-cost and tailored to student schedules.

- Applying for local government transit subsidies or student discounts that significantly lower fares.

- Carpooling with classmates or neighbors to share commuting expenses and reduce vehicle wear.

- Biking or walking when feasible, which eliminates transit costs and benefits health.

- Choosing housing near campus or work to cut down on expensive daily travel.

In addition, campus programs may offer transit passes or hardship grants for transportation support, which help reduce financial strain without increasing loan balances. Borrowing for a vehicle typically involves long-term expenses such as maintenance, insurance, and interest, which public transit alternatives avoid.

Prioritizing student loan funds for educational expenses only is critical. By researching and accessing available support programs, students can prevent unnecessary borrowing and improve their financial health during and after college.

How do transportation choices affect total student loan debt and repayment outcomes?

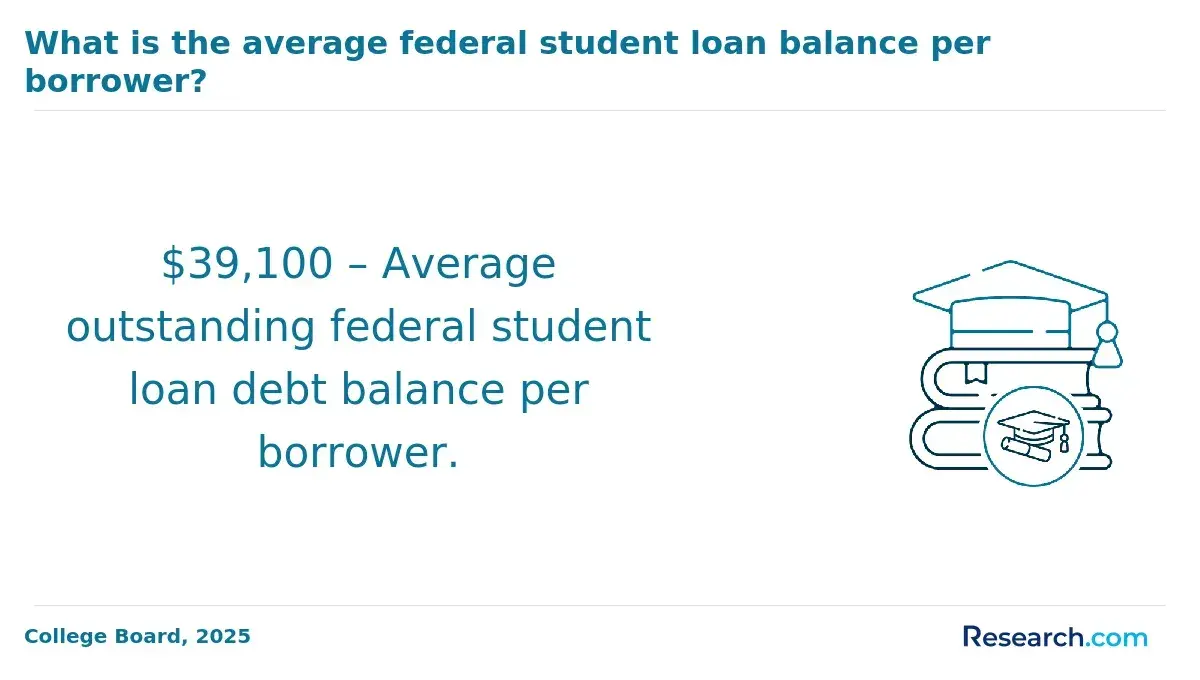

Transportation expenses can significantly increase total student loan debt when students borrow to cover these costs. Federal student loan debt averages $39,547 nationwide, rising to $43,333 when private loans are included (Education Data Initiative, Student Loan Debt Statistics 2026). Adding transportation costs to loans increases the overall amount borrowed, leading to longer repayment periods and higher interest charges.

Opting for affordable transportation methods-such as public transit or biking-helps reduce the need for additional loans. On the other hand, financing a car through student loans adds ongoing costs including insurance, maintenance, and fuel, which further elevate debt.

Higher transportation-related debt increases monthly payments, intensifies the risk of default, and causes financial strain after graduation. Those carrying larger loan balances may delay important milestones like homeownership or career progression.

Students with long commutes should consider:

- Strictly budgeting to cover transportation without borrowing.

- Seeking campus housing or living closer to school.

- Taking advantage of any employer or school transit benefits.

Being aware of how transportation choices impact loan balances promotes smarter borrowing decisions and more stable financial futures. For more information on managing student loans effectively, visit the Education Data Initiative.

Other Things You Should Know About

Yes, student loans impact your credit score. Timely payments can help build a positive credit history, while missed or late payments can harm your credit score and make it harder to secure future loans or credit cards.

Many federal student loans offer options for deferment or forbearance, allowing you to temporarily pause payments under certain circumstances such as financial hardship or enrollment in school. Private student loans may have more limited or no such options, depending on the lender.

Federal subsidized loans do not accrue interest during enrollment at least half-time, while unsubsidized loans begin accruing interest immediately. Private loans typically start accruing interest as soon as the funds are disbursed.

Generally, student loans are difficult to discharge through bankruptcy and require proving undue hardship in court. This makes student debt a long-term financial obligation unless exceptional circumstances arise.