2026 What Can Student Loans Be Used For?

Student Finance & Loan Expert

Many prospective graduate students face uncertainty about how exactly student loans can be applied. This confusion often complicates budgeting and financial planning, raising concerns about eligibility and restrictions. Understanding permissible uses prevents misuse and helps avoid potential loan default.

Clarifying the scope of expenses covered by student loans can also reveal opportunities to optimize funds beyond tuition. This article explains what student loans can be used for and offers clear guidance to help readers make informed financial decisions regarding financing their graduate education.

- What can student loans be used for? Loan Uses

- How do federal and private student loans differ? Federal vs Private

- Who qualifies for student loans and FAFSA aid? Eligibility

- What school expenses can student loans cover? Covered Costs

- How much can you borrow for college? Borrowing Limits

- What interest rates and fees apply to student loans? Rates and Fees

- How do student loan repayment plans work? Repayment Plans

- What student loan forgiveness programs are available? Forgiveness Programs

- When should you consolidate or refinance student loans? Consolidate or Refinance

- What happens if you miss student loan payments? Default Risks

What can student loans be used for?

Student loans in 2026 cover a broad range of education-related expenses essential for completing your studies. Besides tuition and fees, federal student loan funds can be used for room and board, including campus housing or rent and utilities if you live off-campus.

This flexibility allows students to allocate money toward living costs directly related to their education. For more details, see how student loan money for rent and bills is commonly applied.

Other allowed uses include textbooks, course supplies, and essential equipment like laptops or specialized software. Transportation costs-such as fuel or transit passes-also qualify when necessary for attending classes. These uses align with what can student loans cover in the United States, ensuring funds focus on necessary education expenses.

Loans may also support personal expenses tied to study, including childcare or medical costs, provided they arise during your enrollment. Approved study abroad programs qualify as well, broadening loan applicability beyond the traditional campus experience. Awareness of these allowed uses of federal student loan funds helps students borrow responsibly and plan their budgets effectively.

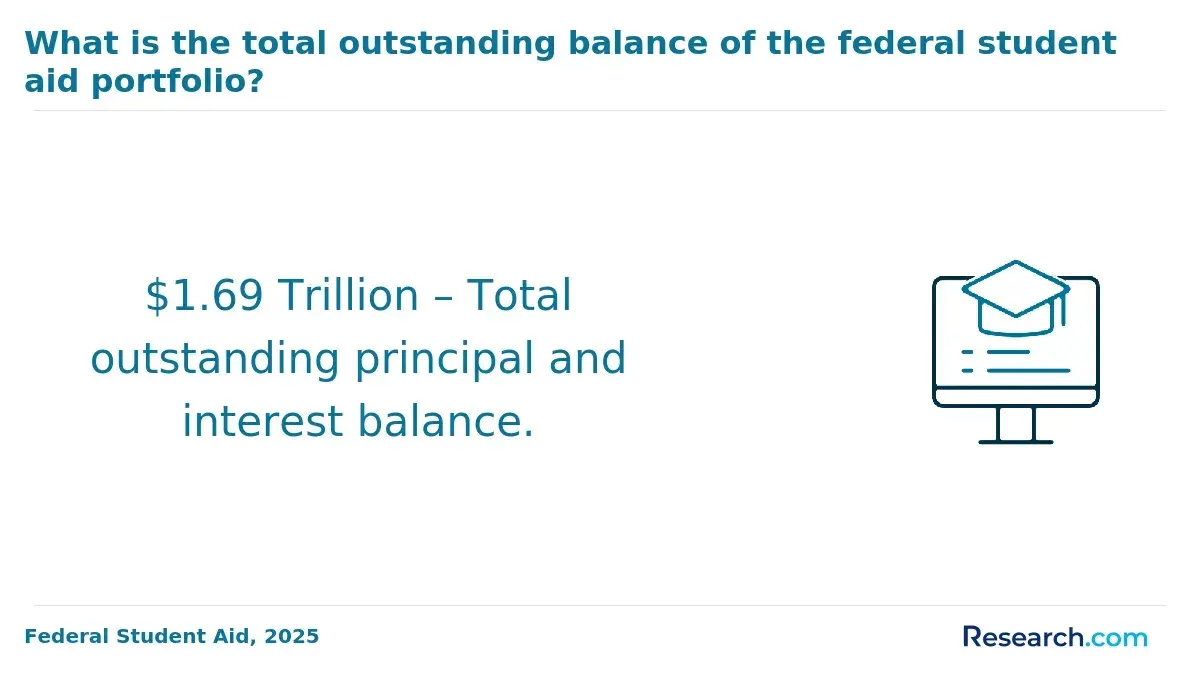

In the 2024-25 academic cycle, $102.6 billion was borrowed by students and parents, with 74% from federal Direct Loans like unsubsidized, subsidized, and PLUS loans. These figures from LendingTree's analysis of U.S. Department of Education data illustrate that student loans widely support comprehensive education costs, not solely tuition fees.

How do federal and private student loans differ?

Federal and private student loans differ mainly in eligibility, interest rates, repayment flexibility, and borrower protections. Federal loans, offered through the Free Application for Federal Student Aid (FAFSA), are accessible to most students regardless of credit history.

In contrast, private loans come from banks or lenders and typically require credit approval and sometimes a co-signer. This distinction is important when considering federal vs private student loan differences.

Federal loans generally feature fixed and lower interest rates-for example, Direct Subsidized Loans for undergraduates have rates around 4.99% for 2026-while private loans can range from 3% to over 12%, depending on creditworthiness.

Repayment options also vary: federal loans provide income-driven plans, deferment, and forbearance, allowing flexibility based on the borrower's financial situation. Private loans often lack these protections, which can make them riskier if unexpected hardships occur.

The choice between federal and private loans often depends on tuition costs and financial needs. Average tuition and fees vary widely, with public four-year in-state institutions averaging $11,720 versus $42,440 at private nonprofit schools. Students seeking how federal and private student loans compare may find federal loans preferable for cost-effectiveness and borrower safeguards.

Private loans may become necessary if federal aid limits are reached or extra funds are needed. Prospective borrowers should also explore options on how to get student loans without parents to better understand their financing choices.

Who qualifies for student loans and FAFSA aid?

Federal student loans and FAFSA aid are mainly available to U.S. citizens and eligible non-citizens enrolled in qualifying degree or certificate programs. To qualify, applicants typically must demonstrate financial need, though some federal loans like Direct Unsubsidized Loans do not require proof of need.

Pell Grants and subsidized loans focus on assisting low- to moderate-income students, reflecting specific qualifications for federal student loans.

The Free Application for Federal Student Aid (FAFSA) must be completed annually, assessing factors such as family income, assets, dependency status, and enrollment to establish eligibility criteria for FAFSA financial aid.

Independent students-those over 24, married, veterans, or with dependents-are often evaluated based on their own finances instead of parental information.

Both part-time and full-time undergraduate and graduate students maintaining satisfactory academic progress can qualify. For instance, graduate students in master's programs can access Direct Unsubsidized Loans but not Pell Grants, which are reserved for undergraduates.

FAFSA aid can cover various costs including tuition, housing, and meal plans. The College Board reports that living expenses like room and board at public universities often exceed tuition fees, emphasizing the broader coverage of federal aid.

Eligibility also requires maintaining enrollment status-usually at least half-time-and not being in default on prior federal loans. International students generally do not qualify, except in specific cases for eligible non-citizens. Working professionals interested in advanced degrees should consider exploring MBA loan options suitable for their needs.

What school expenses can student loans cover?

Student loans cover a variety of educational expenses, going beyond just tuition fees. Approved costs covered by student loans often include tuition, room and board, and mandatory school charges. These loans can also pay for off-campus housing expenses such as rent and utilities, which supports students living independently.

Essential school supplies like books, technology, and other materials are also included, reflecting the significant rise in related costs. For instance, average expenses for books and supplies at public four-year institutions totaled $1,330 recently.

Technology purchases such as laptops and software are crucial, especially as many schools require digital materials. This broad scope of student loan uses for educational expenses also extends to transportation costs directly tied to attending school, like bus passes, fuel, or airfare for distance learners.

Loans may additionally cover necessary personal expenses, such as internet access and childcare for student-parents, provided these are essential for attendance and properly documented. It's important to note that student loans cannot be used for non-educational purposes like luxury items or unrelated travel, to avoid repayment issues.

Students should carefully document their expenses to ensure compliance with lender requirements. Those interested in specialized funding options can learn more about nursing school loans, which often have their own specific guidelines and benefits.

How much can you borrow for college?

Federal student loan borrowing limits are set by your academic year and dependency status. Dependent undergraduates can borrow up to $5,500 in their first year, increasing to $7,500 for the second and remaining undergraduate years.

Independent undergraduates have higher limits, beginning at $9,500 for the first year and up to $12,500 annually thereafter. Graduate and professional students may borrow as much as $20,500 per year in federal direct loans.

Your school's calculated cost of attendance (COA) plays a major role in determining loan eligibility. COA includes tuition, fees, room and board, plus additional expenses such as transportation and personal costs. For instance, public four-year institutions estimate transportation and miscellaneous expenses around $3,190 annually. These figures help ensure loans cover more than just tuition.

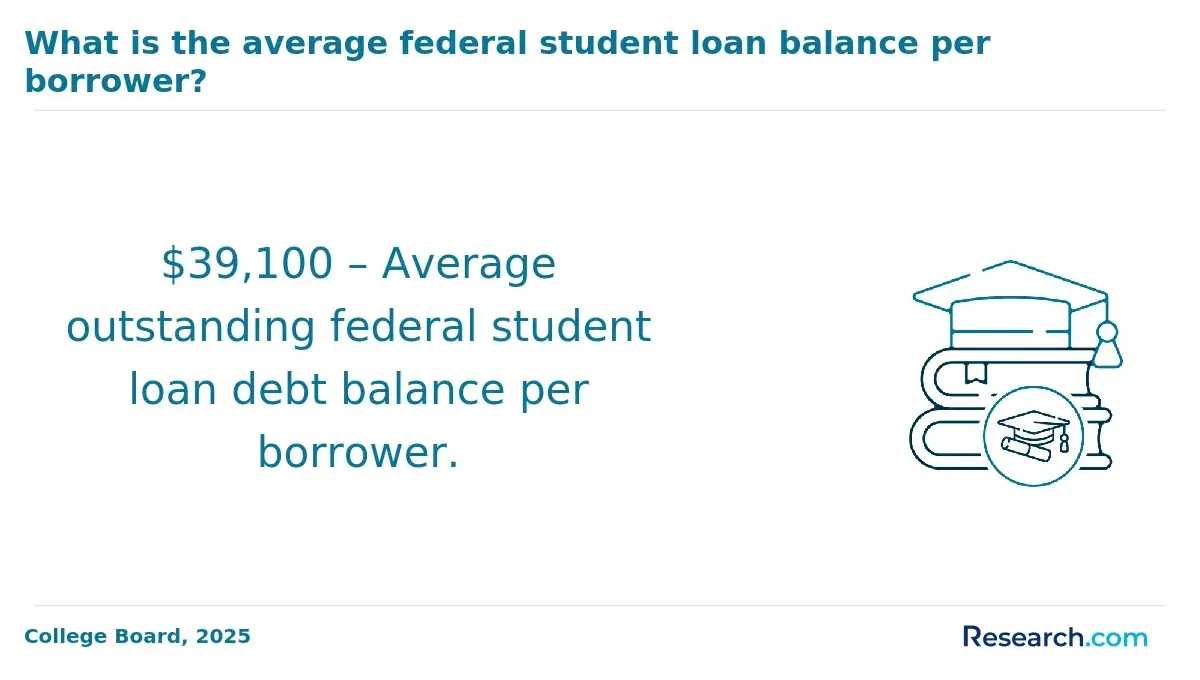

Private student loans often provide flexibility by covering the gap between COA and financial aid but may require a creditworthy cosigner. Federal loan limits are strict, with annual and aggregate caps designed to prevent excessive debt. Graduate students, for example, have a $138,500 aggregate cap, which includes undergraduate borrowing.

- Dependent Undergraduate Borrowing Limits: $5,500 to $7,500 annually.

- Independent Undergraduate Limits: $9,500 to $12,500 annually.

- Graduate/Professional Loan Limit: $20,500 annually.

- Graduate Aggregate Loan Cap: $138,500 including undergrad loans.

Loan amounts reflect your true financial need by covering both direct educational expenses and reasonable personal costs, supporting a comprehensive approach to funding your education.

What interest rates and fees apply to student loans?

U.S. federal student loan interest rates in 2026 are fixed based on the loan type and disbursement date. Direct Subsidized and Unsubsidized Loans for undergraduates disbursed between July 1, 2025, and June 30, 2026, carry a 5.50% fixed interest rate.

Graduate students with Direct Unsubsidized Loans pay a higher fixed rate of 7.05%. Direct PLUS Loans for graduate/professional students and parents have an 8.05% fixed rate in the same period. Private student loan rates can vary significantly, typically from 4% to more than 14%, depending on creditworthiness and lender policies, and may be fixed or variable.

Federal loans also include an origination fee deducted upfront, usually between 1.057% and 4.228% of the loan amount for loans disbursed in 2026. For example, a $10,000 loan with a 1.057% fee will withhold $105.70 at disbursement. Private loans often charge origination fees, late fees, and other costs, which vary by lender.

Students financing short-term study abroad programs-55% of which last eight weeks or less (Institute of International Education, Open Doors 2024)-often prefer federal loans due to their stable fixed rates and manageable fees. This approach helps cover program expenses and travel without risking fluctuating rates common in private lending.

How do student loan repayment plans work?

Student loan repayment plans help borrowers manage their debt after leaving school by setting monthly payments and repayment terms tailored to their financial situation and loan type. Options include standard, graduated, extended, and income-driven plans.

Standard repayment requires fixed monthly payments over 10 years, while graduated plans start with lower payments that increase every two years. Extended plans allow terms up to 25 years, lowering monthly payments but increasing total interest. Income-driven plans base payments on discretionary income, usually 10-20%, adjusting annually with changes in income and family size. After 20-25 years on an income-driven plan, any remaining balance may be forgiven.

Borrowers can switch plans if their financial situation changes, such as during unemployment or reduced income, to avoid default. Federal loans typically offer more flexible repayment options and protections than private loans, which usually have fixed payments and fewer adjustment possibilities.

It's important to note what student loans do not cover. Over half of undergraduates reported using personal savings, credit cards, or family income to pay for expenses outside the official cost of attendance. Loans cannot legally fund consumer purchases or other non-allowable costs.

- Plan monthly budgets around allowable loan uses and additional expenses.

- Select repayment plans based on expected income and long-term financial goals.

What student loan forgiveness programs are available?

Public Service Loan Forgiveness (PSLF) is a key student loan forgiveness program for borrowers working full-time in government or qualifying non-profit jobs. After 120 qualifying payments under eligible repayment plans, the remaining loan balance can be forgiven tax-free.

Teacher Loan Forgiveness provides up to $17,500 in debt relief for educators working five consecutive years in low-income schools, directly reducing federal Direct Loan balances for teachers dedicated to underserved communities.

Income-Driven Repayment (IDR) plans calculate monthly payments based on income and family size, forgiving any remaining debt after 20 or 25 years. Borrowers should track their progress yearly, as amounts forgiven under IDR may be taxable.

Additional forgiveness programs exist for specific professions such as nurses, healthcare workers, and military personnel. Many states offer loan repayment assistance for graduates working in public interest roles locally.

- Nearly 29% of undergraduates received loan refunds due to excess aid.

- Of these students, 41% admitted using some funds for non-educational expenses, which can increase debt burdens.

Borrowers should verify eligibility requirements carefully, maintain thorough documentation, and stay updated on legislative changes impacting forgiveness programs to maximize benefits and avoid unnecessary debt growth.

When should you consolidate or refinance student loans?

Consolidating or refinancing student loans can improve your financial situation by lowering interest rates, reducing monthly payments, or making loan management easier. Consolidation merges multiple federal loans into one, often extending repayment terms to reduce monthly bills.

This method suits borrowers who struggle with budgeting or managing payments across several loans. Refinancing replaces existing loans with a new private loan, usually offering a lower interest rate, but may eliminate federal protections like income-driven repayment or loan forgiveness options.

Consider consolidating if:

- You have multiple federal loans with different servicers and want one monthly payment.

- You find it difficult to track payments and want to simplify your budget.

- You can extend your repayment period to lower monthly costs.

Refinance only if:

- Your income is stable and your credit score qualifies you for better rates.

- You no longer need federal benefits such as deferment or forgiveness programs.

- You aim to pay off loans faster with a lower interest rate.

Maintaining a written budget and tracking spending greatly aids repayment management. For example, undergraduates who budgeted were notably more prepared for unexpected expenses, highlighting the crucial role of financial planning before changing loan terms.

What happens if you miss student loan payments?

Missing student loan payments lead to immediate and serious consequences. When a payment is overdue by more than 30 days, the loan becomes delinquent. If unpaid for 270 days on federal loans, delinquency escalates to default, which severely damages your credit score and complicates obtaining housing, employment, or other credit.

In default, the full loan balance can be demanded instantly, with collection fees up to 25% added. The government may also garnish wages, seize tax refunds, and withhold Social Security benefits without court approval to recover the debt.

Borrowers struggling to keep up should take action:

- Contact loan servicers promptly to discuss hardship assistance.

- Request income-driven repayment plans that adjust payments based on your income and family size.

- Consider deferment or forbearance to temporarily suspend or reduce payments during financial difficulties.

The share of delinquent federal student loans rose sharply, with 10.0% delinquent by the fourth quarter of 2025 and loans 90+ days late increasing over 9 percentage points since late 2024. This trend underscores how quickly financial challenges impact repayment (Education Data Initiative, Student Loan Debt Statistics 2026; LendingTree analysis of U.S. Department of Education data).

Managing payments proactively, seeking assistance early, and understanding repayment options are vital to avoiding severe financial penalties linked to missed student loan payments.

Other Things You Should Know About

Yes, student loans can impact your credit score. Making timely payments can help build a positive credit history, while missed or late payments can harm your credit. The loan balance and your repayment behavior are reported to credit bureaus, influencing your overall creditworthiness.

Generally, student loans are not easily discharged through bankruptcy. Borrowers must demonstrate undue hardship in court to have their loans forgiven, which is a challenging legal standard to meet. Most student loans remain a financial obligation even after declaring bankruptcy.

Student loans cannot be used to pay for homeschooling costs. These loans are intended to cover expenses related to accredited postsecondary institutions and approved educational programs. Homeschooling typically does not qualify as an eligible education expense for these funds.

Yes, student loans can be used to finance study abroad programs if the program is approved by the borrower's home institution and qualifies for federal or private student aid. Eligible costs may include tuition, travel, and living expenses associated with the study abroad experience.