2026 Best Student Loans for Online Bachelor's Degrees

Student Finance & Loan Expert

Choosing the right student loan can become overwhelming when pursuing an online bachelor's degree, especially for those balancing work and study. Interest rates, repayment terms, and borrower protections differ widely, affecting long-term financial health. Many applicants struggle to compare options and understand eligibility requirements.

Navigating this landscape without clear guidance increases the risk of costly debt. This article examines the best student loans suited for online bachelor's degrees, highlighting key features to help borrowers select the most advantageous financing and avoid common pitfalls in loan decision-making.

- What are the best federal and private student loans for online bachelor's degrees? Best loans

- How do federal student loans compare to private loans for online undergrads? Federal vs private

- How can I estimate how much I should borrow for an online bachelor's? Borrowing amount

- What eligibility rules apply to getting student loans for online bachelor's programs? Eligibility rules

- How do I use the FAFSA and other applications to get loans for online study? FAFSA steps

- What interest rates, fees, and borrowing limits apply to online bachelor's loans? Rates & limits

- Which repayment plans work best for online bachelor's borrowers after graduation? Repayment plans

- What loan forgiveness and cancellation options exist for online bachelor's graduates? Forgiveness options

- When does refinancing or consolidating student loans make sense for online students? Refinance vs consolidate

- How do deferment, forbearance, and default affect online bachelor's student loan debt? Hardship & default

What are the best federal and private student loans for online bachelor's degrees?

Federal student loans offer some of the most reliable federal student loan options for online bachelor's degrees, featuring fixed interest rates, borrower protections, and flexible repayment plans.

For 2024-25, Direct Subsidized and Unsubsidized Loans have a fixed interest rate of 6.53%, significantly lower than private loan rates, which range from 9.37% to 15.09% as of early 2025. Subsidized loans are particularly beneficial since the government pays the interest while students are enrolled, lowering overall costs.

Private student loans can complement federal aid but generally should be pursued only after fully using federal options. These loans often require credit checks and may have variable rates that can increase over time. Lenders specializing in the best private loans for online bachelor's degree programs, like Sallie Mae and Discover Student Loans, offer competitive fixed rates and flexible terms.

Additional factors to consider include income-driven repayment plans, deferment options, and loan forgiveness programs, which are mostly exclusive to federal loans. Public service loan forgiveness is an important benefit for those entering related careers. Students facing urgent financial needs might also explore resources on student loans for tuition deadline.

Choosing federal loans first reduces financial risk and ensures access to these valuable protections, making them a crucial part of financing an online bachelor's degree.

How do federal student loans compare to private loans for online undergrads?

Federal student loans offer lower interest rates and more flexible repayment options compared to private loans for online undergraduates. For instance, Direct Subsidized Loans come with fixed interest rates well below those of private loans, and the government pays the interest while students are enrolled.

Federal loans also include income-driven repayment plans, deferment, and forbearance options that are rarely matched by private lenders, reducing default risk and providing financial flexibility during hardships.

With private student loans, eligibility heavily depends on creditworthiness, often requiring a co-signer for applicants with limited credit history. Their interest rates can be fixed or variable but are generally higher than federal loans, increasing overall borrowing costs.

Private lenders typically offer fewer protections if a graduate experiences unemployment or a loss of income. This is an important factor in the comparison of federal and private student loans for online bachelor's degrees.

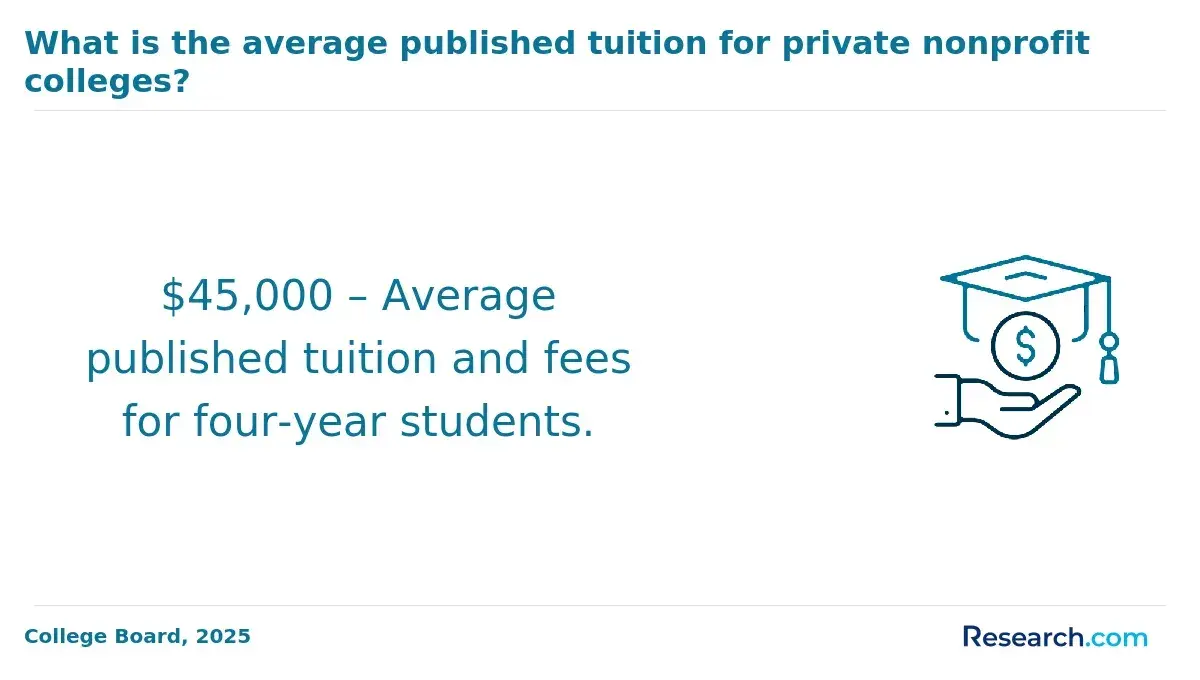

The average annual tuition and fees at public online colleges are about $10,940, whereas private nonprofit online institutions average $42,410. This discrepancy leads many students to borrow considerably, with federal loans capping borrowing limits based on year and dependency status.

Students attending public online colleges often cover most costs with federal aid and lower tuition, making federal loans the safer primary choice.

Those considering private loans should apply for federal aid first and use private options sparingly, carefully weighing interest rates, fees, and repayment terms. Students can also explore resources like the ascent student loan application process to help with private borrowing decisions.

How can I estimate how much I should borrow for an online bachelor's?

Estimate how much to borrow for an online bachelor's degree by calculating your total education costs and subtracting grants, scholarships, and personal contributions.

Begin with tuition, fees, books, and technology expenses, plus additional costs like internet access or software required by your program, and include living expenses if applicable. This approach is essential for accurately estimating borrowing needs for an online bachelor's degree program.

Federal Student Aid sets loan limits: dependent undergraduates can borrow up to $31,000 combined in Direct Subsidized and Unsubsidized Loans, while independent students may borrow up to $57,500. Students attending higher-priced online universities may encounter coverage gaps exceeding these limits.

Consider these steps:

- Identify your school's total cost of attendance.

- Subtract expected financial aid that does not require repayment.

- Calculate your remaining unmet need up to federal loan limits.

If your uncovered costs exceed federal loan limits, look into alternatives such as private loans, payment plans, or additional scholarships. To find resources, explore grants for adults going back to school. Avoid borrowing more than necessary to minimize future debt.

When deciding how to calculate student loan amount for an online bachelor's degree, evaluate your expected post-graduation earning potential compared to the total amount borrowed. Online programs vary in cost and career outcomes, so assess how your specific program's price aligns with its value.

Use loan calculators and consult your school's financial aid office to refine your borrowing estimate. This strategic method helps reduce the risk of excessive debt while responsibly covering educational expenses.

What eligibility rules apply to getting student loans for online bachelor's programs?

Eligibility criteria for student loans in online bachelor's programs mainly depend on enrollment at an accredited institution approved for federal student aid.

Students must be U.S. citizens or eligible noncitizens, maintain satisfactory academic progress, and enroll at least half-time to qualify for most federal loans such as Direct Subsidized and Unsubsidized Loans. Financial need determines eligibility for subsidized loans, while unsubsidized loans are available to all regardless of income.

Parent PLUS Loans have specific requirements: parents cannot have an adverse credit history and the student must be a dependent undergraduate enrolled at least half-time. For 2024-25, these loans have a fixed 9.08% interest rate and a 4.228% origination fee. Borrowing limits reach the total certified cost of attendance minus other aid; the average Parent PLUS loan balance is about $29,000.

Private loans differ widely in eligibility, often requiring credit checks and cosigners. Comparing terms carefully and exploring federal options first is critical for borrowers considering private loans or looking to refinance federal student loans.

Enrollment status impacts eligibility significantly. Dropping below half-time can stop disbursements or trigger repayment. Valid FAFSA submission and verification are mandatory before funds release, and previous loan defaults can disqualify students until resolved.

Meeting all requirements and maintaining academic progress preserve loan eligibility, safeguarding the financial support necessary for online bachelor's studies.

How do I use the FAFSA and other applications to get loans for online study?

Start by completing the Free Application for Federal Student Aid (FAFSA) on the official site to determine your eligibility for federal grants, work-study, and loans such as Direct Subsidized and Unsubsidized Loans.

Submit FAFSA early, ideally by your school's priority deadline, as some aid is limited. Use accurate financial information from you and your family to calculate your Expected Family Contribution (EFC) precisely.

After you apply, review your Student Aid Report (SAR) carefully to confirm all details and understand your aid eligibility. Contact your school's financial aid office if you find errors or have questions. Federal student loans usually offer fixed interest rates, borrowing caps, and flexible repayment options, making them the safest borrowing choice.

If federal aid doesn't cover all tuition or expenses, private student loans can fill the gap. These loans often require credit checks and sometimes co-signers. Private lenders have variable rates and fewer borrower protections. Applications vary but typically involve online prequalification plus income and credit verification.

Private loans accounted for about 8% of total education debt but 13% of new undergraduate borrowing, reflecting growing reliance on them as federal limits remain capped while tuition costs rise.

- File FAFSA annually to maximize federal aid.

- Respond quickly to requests for additional information.

- Compare private loan offers, focusing on interest rates, fees, and repayment terms.

What interest rates, fees, and borrowing limits apply to online bachelor's loans?

Interest rates for online bachelor's degree loans differ based on loan type. Federal Direct Undergraduate Loans have a fixed interest rate of 6.53% with a 1.057% origination fee deducted at disbursement. Private student loans often carry fixed rates between 7% and over 12%, influenced by creditworthiness and lender policies. They commonly include origination fees and may use variable rates that change over time.

Federal loans impose annual and total borrowing limits: first-year undergraduates may borrow up to $5,500, sophomores up to $7,500, and the total undergraduate borrowing limit is $57,500. Private lenders generally allow borrowing up to the full cost of attendance, but approval depends on credit checks or having a cosigner.

Fees add significantly to costs. Federal loans charge upfront fees around 1% of the principal. Private loans may impose origination fees of 5% or more, plus possible late payment or prepayment penalties, so verifying exact fees beforehand is essential.

Repayment examples highlight the cost gap: a $30,000 federal loan at 6.53% interest might require about $337/month with $10,440 in interest over 10 years; the same amount at an 11% private rate could mean $414/month and $19,680 in interest. This difference underscores potential long-term savings with federal borrowing when rates and fees are lower.

Which repayment plans work best for online bachelor's borrowers after graduation?

Graduates with online bachelor's degrees should consider income-driven repayment (IDR) plans and graduated repayment plans to manage student loans effectively. IDR plans like Income-Based Repayment (IBR) and Pay As You Earn (PAYE) adjust monthly payments based on income and family size, helping borrowers with fluctuating entry-level salaries maintain financial stability and build savings.

Graduated repayment plans begin with lower payments that increase every two years, aligning with typical salary growth. This benefits recent graduates expecting income increases within 10 years but needing lower initial payments.

Federal loan borrowers benefit significantly from IDR plans, which provide forgiveness options after 20 to 25 years of qualifying payments. Early application to these plans post-graduation can help avoid default and unmanageable fixed payments.

Fixed repayment plans offer predictable monthly bills but may strain borrowers with entry-level income or multiple financial commitments. These plans are best for those with stable or higher post-graduation earnings.

Private loan borrowers have limited flexibility but should explore lenders offering repayment assistance or refinancing options. Refinancing can reduce interest rates but may sacrifice federal protections.

According to the U.S. Bureau of Labor Statistics, median annual earnings for full-time bachelor's degree holders were $77,844, much higher than $46,748 for high school graduates. This earnings premium supports choosing repayment plans that balance manageable payments with the goal of faster loan payoff based on expected income growth.

What loan forgiveness and cancellation options exist for online bachelor's graduates?

Federal loan forgiveness and cancellation programs provide essential relief for online bachelor's degree holders managing student debt. Programs like Public Service Loan Forgiveness (PSLF) cancel remaining balances after 120 qualifying monthly payments while working full-time in government or nonprofit jobs. Income-Driven Repayment (IDR) plans may forgive debt after 20 to 25 years of consistent payments, depending on the specific plan selected.

Eligibility requires loans to be federal Direct Loans; private loans seldom offer such forgiveness. Borrowers in teaching careers might qualify for Teacher Loan Forgiveness, which cancels up to $17,500 after five years in qualifying low-income schools.

Temporary relief options such as deferment and forbearance help during financial hardships but do not reduce loan principal. Additionally, some federal programs provide Total and Permanent Disability Discharge for qualified borrowers.

Graduates must carefully track employment eligibility for forgiveness programs and submit required annual documentation, as errors can delay or prevent loan cancellation.

Data from Western Governors University shows that online bachelor's graduates typically increase their average salary by $22,200 within four years, far surpassing average tuition costs ranging from $15,000 to $18,000. This income growth improves the ability to repay loans or benefit from income-driven forgiveness plans, offering a significant financial advantage.

When does refinancing or consolidating student loans make sense for online students?

Refinancing or consolidating student loans can reduce interest rates, lower monthly payments, or streamline repayment for online students. Combining multiple loans with different rates into one payment can prevent missed bills and ease financial management.

Refinancing is particularly useful if your credit score has improved since you took out your loans, allowing you to secure a lower interest rate. For instance, reducing a 7% rate to 4% may save thousands in interest over time. Many online students turn to alternative lenders such as MPower Financing and Prodigy Finance, which serve over 1 million international and DACA students, 90% of whom are enrolled in online or hybrid programs.

Refinancing or consolidation also makes sense if your financial situation has improved or stabilized. You can unify federal and private loans by refinancing through a private lender, but this means losing federal protections like income-driven repayment plans and loan forgiveness eligibility.

Consider these points before deciding:

- Are current interest rates higher than offers from new lenders?

- Do you have a solid credit history and steady income?

- Would a single monthly payment simplify repayment?

- Are you prepared to forgo federal loan benefits when refinancing privately?

These considerations help determine if refinancing or consolidation fits your financial goals and loan profile.

How do deferment, forbearance, and default affect online bachelor's student loan debt?

Deferment and forbearance provide ways for online bachelor's degree students to temporarily pause or reduce student loan payments, but they affect loan balances differently. During deferment, interest on subsidized federal loans is paused, preventing the loan balance from growing.

Forbearance also pauses payments but interest accrues on all loan types, causing total debt to increase. These options offer short-term relief but can extend repayment periods and increase overall costs.

Default happens when payments are missed for 270 days on federal loans, severely damaging credit scores and triggering immediate actions like wage garnishment, tax refund seizure, and increased collection fees. Defaulted loans are hard to rehabilitate, so proactive repayment management is critical for online students.

Data shows about 1 in 5 borrowers with federal undergraduate loans between 2016 and 2020 defaulted within 12 years, with higher rates among students at primarily online, for-profit institutions (U.S. Department of Education, College Scorecard 2024 cohort analysis). This underscores the importance of using deferment and forbearance wisely and exploring other federal options.

Students facing hardship should consider income-driven repayment plans alongside deferment or forbearance. Forbearance is suited for short-term crises, while deferment applies to students in school, active military, or unemployed. Ignoring repayment leads to default, so contacting loan servicers immediately is essential.

Other Things You Should Know About

Yes, student loans can typically be used for a range of education-related expenses beyond tuition. This includes fees, textbooks, supplies, technology needed for online learning, and sometimes living expenses if you qualify for sufficient loan amounts. However, loan funds must be used for approved costs as defined by your school's financial aid office.

Most federal student loans offer the same borrower protections regardless of whether the degree is earned online or on-campus. These include flexible repayment options, income-driven plans, deferment, and forbearance. Private loans, however, may vary by lender, so it is important to check the specific terms for loans intended for online students.

Enrollment status matters when qualifying for student loans, including those for online programs. Generally, you need to be enrolled at least half-time in an eligible program to qualify for most federal loans. Full-time or part-time status can influence loan amounts and disbursement schedules, so verify your program's classification with the financial aid office.

Student loans are available for online programs at for-profit institutions, but eligibility depends on whether the school is accredited and participates in federal financial aid programs. Some private lenders may have additional restrictions or higher interest rates for for-profit school borrowers. It is crucial to confirm your school's status before applying for loans.