2026 How to Become a Mortgage Broker: Salary & Career Paths

Co-Founder and Chief Data Scientist

Becoming a mortgage broker can be a strong career move for people who want to work at the intersection of real estate, lending, sales, compliance, and client advising. The mortgage brokerage services market is projected to reach $151.6 billion by 2028, with an annual growth rate of 10.3%, which points to continued opportunity for professionals who can help borrowers compare loan options and move through a complex financing process. The path, however, is regulated: you need licensing, pre-licensing education, a passing NMLS exam score, state registration, and ongoing compliance.

This guide explains how to become a mortgage broker in 2026, what education is useful, how licensing works, what skills matter, how much brokers earn, where salaries are highest, how technology is changing the field, and how to decide whether this career or business path fits your goals.

Quick answer: how do you become a mortgage broker?

To become a mortgage broker, you generally need at least a high school diploma or GED, 20 hours of NMLS-approved pre-licensing education, a passing score on the NMLS exam, state registration, a mortgage broker bond, and an approved license application. Many brokers also pursue college coursework or degrees in finance, business, accounting, or real estate to strengthen their credibility and improve their understanding of lending, credit, compliance, and property markets.

Key things you should know about becoming a mortgage broker

- A high school diploma is typically the baseline education requirement, but many brokers earn degrees in finance, business, accounting, or real estate to build stronger market knowledge and client trust.

- Legal practice requires more than sales ability: you must complete pre-licensing education, pass the NMLS exam, satisfy state requirements, and register properly before operating.

- Most states require annual continuing education, and license renewal usually depends on completing CE, paying renewal fees, and keeping required bonds active.

- Income can be high, but it is often tied to commissions, market conditions, lender relationships, lead generation, and the broker’s ability to close loans efficiently and ethically.

- Technology is making the work faster and more data-driven, but it also raises the bar for compliance, cybersecurity awareness, customer communication, and digital workflow management.

- What education do you need to become a mortgage broker?

- What licensing steps are required for mortgage brokers in 2026?

- Do mortgage brokers need continuing education?

- What skills do mortgage brokers need most?

- How much do mortgage brokers make in 2026?

- Which cities have the highest mortgage broker salaries?

- Is there demand for mortgage brokers in 2026?

- How is technology changing mortgage brokerage?

- How can mortgage brokers advance their careers?

- How can brokers improve operational efficiency?

- How can you future-proof a mortgage brokerage?

- How do you start a mortgage brokerage?

- Mortgage broker vs. loan officer: what is the difference?

- Can an MBA help mortgage brokers lead and scale?

What education do you need to become a mortgage broker?

You do not need a specific college degree to become a mortgage broker, but education can affect how prepared you are for the work. The minimum entry requirement is usually a high school diploma or GED, followed by state licensing steps. Still, many professionals choose college programs because mortgage brokerage requires comfort with financial documents, credit analysis, real estate transactions, federal and state regulations, and client advising.

According to Zippia, 64% of mortgage brokers have a bachelor’s degree, making it the most common education level in the field. Another 17% hold an associate degree, and 8% have a master’s degree. These figures do not mean a degree is legally required, but they show that many brokers use formal education to strengthen their professional foundation.

| Education path | When it makes sense | How it can help a mortgage broker |

| High school diploma or GED plus licensing | You want the fastest regulated entry path and plan to learn through work experience. | Meets the baseline education expectation before completing licensing requirements. |

| Associate degree | You want college-level business or finance training without committing to a longer program. | Can introduce accounting, business communication, economics, and consumer finance concepts. |

| Bachelor’s degree | You want broader preparation for lending, sales management, compliance, or future business ownership. | Can improve your understanding of finance, real estate, marketing, law, and client advisory work. |

| Master’s degree | You are targeting leadership, entrepreneurship, financial strategy, or specialized advisory roles. | Can support advanced decision-making, business planning, risk analysis, and operations strategy. |

Useful majors include finance, business administration, accounting, economics, and real estate. A real estate bachelor’s program online can be especially relevant for students who want coursework in property markets, real estate finance, valuation, and ethics while keeping a flexible schedule.

The best education choice depends on your career goal. If you want to enter the field quickly, licensing and supervised experience may matter more than a degree. If you plan to run a brokerage, recruit staff, manage compliance, or serve higher-value clients, business and finance education can provide long-term advantages.

What licensing steps are required for mortgage brokers in 2026?

Mortgage brokerage is a regulated profession because brokers help consumers secure major financial products. Requirements vary by state, but most aspiring brokers must complete NMLS education, pass an exam, register with the state, provide documentation, and maintain required bonding or financial responsibility standards.

1. Complete NMLS-approved pre-licensing education

The standard first step is completing 20 hours of pre-licensing education through the Nationwide Mortgage Licensing System (NMLS). This training covers federal law, state rules, ethics, mortgage origination practices, and consumer protection topics. Treat this course as more than a box to check; it is the foundation for legally and ethically advising borrowers.

2. Pass the NMLS licensing exam

After pre-licensing education, candidates must pass the NMLS exam. The exam includes federal and state material, and a minimum score of 75% is required on each section. Strong preparation matters because the test evaluates regulatory knowledge as well as practical understanding of loan origination.

If financial statements, ledgers, cash flow, and basic accounting are unfamiliar, a bookkeeping certificate program may help you build financial fluency before advising clients on complex borrowing decisions.

3. Register the business or employment arrangement with the state

After passing the exam, you must follow your state’s process for registration. This may include filing business documents, paying state fees, submitting background information, and securing a mortgage broker bond. The bond is designed to protect consumers if a broker violates applicable rules or engages in misconduct.

4. Submit the license application and required documentation

The final step is submitting your license application with the required paperwork, fees, proof of bond, and any state-specific documents. Once the state reviews and approves the application, you can legally operate under the license terms that apply in that jurisdiction.

| Licensing step | Purpose | Decision tip |

| Pre-licensing education | Builds knowledge of mortgage law, ethics, and origination practices. | Choose an NMLS-approved provider and schedule study time before the exam. |

| NMLS exam | Confirms that you understand federal and state mortgage rules. | Use practice questions and review weak areas before testing. |

| Business registration | Creates a compliant legal structure for operating in your state. | Check whether your state has requirements for entities, branch offices, or sponsorship. |

| Mortgage broker bond | Provides consumer protection if violations occur. | Confirm the bond amount and renewal rules with your state regulator. |

| License application | Allows the state to approve you for legal practice. | Do not submit incomplete documentation; missing items can delay approval. |

The chart below shows the educational background distribution among mortgage brokers and can help you see how common college preparation is in the profession.

Do mortgage brokers need continuing education?

Yes. Most states require mortgage brokers to complete annual continuing education through the NMLS or another approved process. These courses help brokers stay current on federal and state lending rules, ethics, fraud prevention, consumer protection, and changes in mortgage practices.

A common requirement is around eight hours of continuing education each year, although the exact requirement depends on the state. License renewal typically requires proof that CE is complete, payment of renewal fees, and confirmation that the required mortgage broker bond remains active.

Continuing education should not be treated as a last-minute renewal task. Brokers who plan early are less likely to miss deadlines, and they can use CE to strengthen areas that directly affect performance, such as compliance, borrower communication, loan products, or risk management. Brokers who want deeper accounting knowledge may also compare options such as the most affordable online master’s in accounting programs to build advanced skills for financial analysis or future leadership.

If your long-term plan includes moving into executive finance roles, Research.com also offers a guide on how to become a chief financial officer.

What skills do mortgage brokers need most?

Mortgage brokers need a mix of technical lending knowledge, sales discipline, compliance awareness, and client communication. The role is not only about finding rates. A broker must understand borrower needs, analyze documentation, coordinate with lenders, explain trade-offs, manage timelines, and keep the transaction compliant from application to closing.

Zippia identifies several common skills found on mortgage broker resumes. These include loan applications, FHA and VA loan knowledge, loan programs, credit reports, the loan process, collaboration with real estate brokers, credit history analysis, cold calling, loan origination, commercial loans, loan products, business relationship building, loan packaging, and financial services.

| Skill area | Why it matters | How to build it | How to build it |

| Loan application accuracy | Incomplete or incorrect applications can slow approvals and frustrate borrowers. | Practice document review, checklist use, and lender-specific submission standards. | |

| FHA and VA loan knowledge | Government-backed loans can be important options for eligible borrowers. | Study eligibility rules, documentation needs, and program limitations. | |

| Loan product comparison | Borrowers rely on brokers to explain fixed-rate, adjustable-rate, jumbo, commercial, and other loan options. | Track lender guidelines and learn how product features affect borrower risk and cost. | |

| Credit report analysis | Credit history affects loan eligibility, pricing, and borrower options. | Learn how lenders evaluate credit profiles and how to explain issues clearly to clients. | |

| Communication and trust building | Borrowers may be making one of the largest financial decisions of their lives. | Use plain language, set expectations early, and document important conversations. | |

| Referral development | Many brokers grow through relationships with real estate agents, lenders, and repeat clients. | Build a consistent outreach system and focus on reliability after every referral. | |

| Compliance discipline | Mistakes can lead to penalties, license problems, or consumer harm. | Stay current with CE, state updates, lender rules, and written procedures. |

People from non-finance backgrounds can still succeed if they build the required lending and compliance knowledge. For example, graduates with an online history degree may already have research, writing, and analytical skills that transfer well to document-heavy advisory work. Likewise, professionals interested in workplace behavior and client decision-making may find Research.com’s business psychologist career path useful for exploring adjacent skill sets.

The chart below provides a data-based view of the skills commonly reported by mortgage brokers.

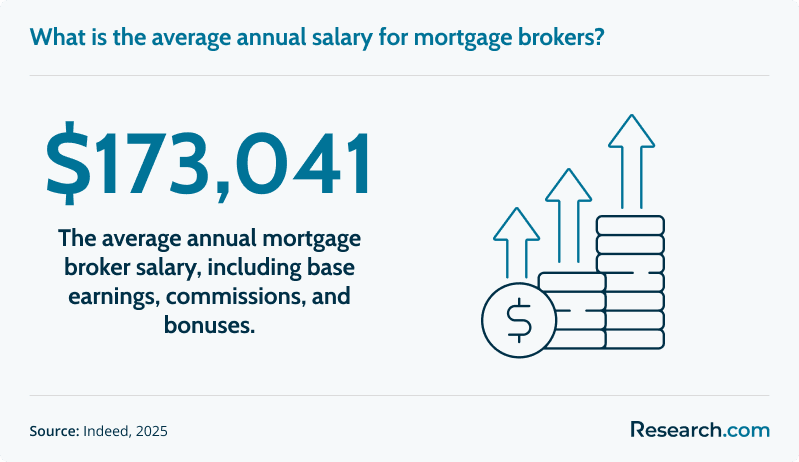

How much do mortgage brokers make in 2026?

According to Indeed, the average salary for a mortgage broker in the US is $173,041 per year. This figure can include commissions and bonuses, so actual earnings may vary widely depending on loan volume, market conditions, location, client base, experience, and whether the broker works independently or within a firm.

Compensation in mortgage brokerage is often performance-sensitive. A broker with strong referral relationships, reliable lender access, efficient processing systems, and a good closing record may earn more than someone who depends only on sporadic leads. At the same time, slower real estate markets, higher competition, weaker lead generation, or compliance issues can reduce income.

Factors that can affect mortgage broker income

- Local housing market: Areas with more transactions or higher property values may create larger commission opportunities.

- Experience level: Experienced brokers often understand lender requirements better and can manage complex files more efficiently.

- Specialization: Commercial lending, VA loans, jumbo loans, or luxury real estate may require deeper expertise but can support stronger positioning.

- Referral network: Relationships with real estate agents, builders, financial advisors, and past clients can drive repeat business.

- Operational systems: Fast document collection, CRM use, and clear client communication can improve conversion and closing speed.

- Employment model: Independent brokers and firm-employed brokers may have different commission structures, expenses, and support levels.

Professionals with property, project, or construction backgrounds may also find the transition natural because they already understand timelines, risk, contracts, and real estate coordination. If that applies to you, Research.com’s guide to the most affordable online construction management degree programs may be relevant for comparing related education paths.

If you are comparing management careers more broadly, you can also review Research.com’s guide on how much managers make and how to become one.

Which cities have the highest mortgage broker salaries?

Mortgage broker pay can differ sharply by location. Local property values, buyer demand, real estate activity, competition, and cost of living all influence compensation. According to Indeed, the following cities report some of the highest average annual salaries for mortgage brokers:

| City | Average Annual Salary |

| Southfield, MI | $170,345 |

| Miami, FL | $161,634 |

| Atlanta, GA | $141,017 |

| Los Angeles, CA | $130,780 |

| Tampa, FL | $127,211 |

| Dallas, TX | $123,318 |

| Houston, TX | $94,250 |

| New York, NY | $90,412 |

| Philadelphia, PA | $89,443 |

Do not choose a market based on salary data alone. A high-paying metro may also have higher business costs, stronger competition, more expensive lead generation, and stricter client expectations. Before relocating or opening a branch, compare licensing rules, cost of living, lender access, referral opportunities, and the number of active real estate professionals in the area.

Career changers with creative or marketing experience may be able to use branding, design, and communication skills to stand out in competitive cities. Research.com’s overview of careers for graphics design master’s degree graduates can help creative professionals think through transferable skills.

Is there demand for mortgage brokers in 2026?

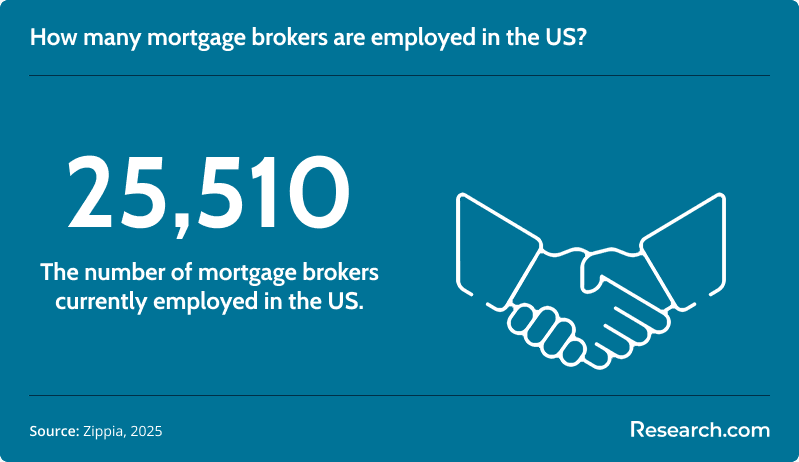

Demand for mortgage brokers remains supported by borrowers’ need for guidance in comparing loan options, understanding approval requirements, and navigating lender documentation. According to Zippia, about 12,600 new mortgage broker positions are expected to be created by 2028, with a projected growth rate of 4% over the decade. Zippia also reports that there are currently 25,510 mortgage brokers employed in the US.

Demand is not uniform across all markets. Brokers may see stronger opportunity where there is active real estate development, steady homebuying activity, complex borrower needs, or a strong network of referral partners. Market cycles still matter, so brokers should avoid assuming that demand automatically guarantees stable income.

Who is this career a good fit for?

- People who are comfortable with sales, follow-up, and relationship-based business development.

- Professionals who can explain financial details clearly without overwhelming clients.

- Detail-oriented workers who can manage documents, deadlines, lender conditions, and compliance tasks.

- Self-directed individuals who can handle income variability and build a referral pipeline.

- Career changers from banking, real estate, insurance, construction, accounting, or financial services.

Who should consider another path?

- People who want a fixed daily routine with little client communication.

- Workers who dislike sales, outreach, or commission-sensitive income.

- Anyone uncomfortable with strict regulatory requirements and documentation standards.

- Professionals who are not prepared to keep learning as loan products, technology, and state rules change.

How is technology changing mortgage brokerage?

Technology is reshaping mortgage brokerage by making lead management, borrower communication, document collection, underwriting coordination, and compliance tracking more efficient. Brokers now commonly work with loan origination systems, customer relationship management tools, e-signature workflows, digital document portals, automated underwriting support, and cloud-based collaboration platforms.

The opportunity is clear: faster workflows can improve client experience and reduce bottlenecks. The risk is also clear: poor data handling, weak cybersecurity habits, or overreliance on automation can create compliance and trust problems. Brokers still need judgment, ethical decision-making, and the ability to explain loan options in human terms.

| Technology trend | How it helps brokers | What to watch carefully |

| Automated underwriting support | Can speed up eligibility checks and lender comparisons. | Automation does not replace compliance review or professional judgment. |

| CRM platforms | Helps organize leads, referrals, follow-ups, and repeat client outreach. | Client data must be protected and updated accurately. |

| Digital document collection | Reduces back-and-forth delays and improves file organization. | Borrowers may still need help understanding what documents are required. |

| Analytics and reporting | Can show where leads come from, which files stall, and which partners convert. | Metrics are useful only if the broker acts on them consistently. |

| Digital communication tools | Allows faster updates through email, portals, video calls, or messaging systems. | Important disclosures and sensitive details must be handled properly. |

Brokers who want deeper training in finance and technology may compare programs such as the most affordable online master’s degrees in finance, especially if they plan to move into strategy, analytics, or leadership roles.

How can mortgage brokers advance their careers?

Mortgage brokers can grow by increasing loan volume, specializing in a niche, managing teams, opening a brokerage, or moving into related financial and real estate advisory work. Advancement usually depends on performance, reputation, compliance record, lender relationships, and the ability to generate repeat business.

| Advancement path | Best for | What it requires |

| Senior broker or team lead | Brokers who want leadership without fully owning a firm. | Strong production history, coaching ability, and reliable compliance habits. |

| Brokerage owner | Entrepreneurial brokers who want control over operations, branding, hiring, and lender relationships. | Licensing, business registration, systems, capital planning, marketing, and risk management. |

| Specialist broker | Professionals who want to serve defined borrower groups or property types. | Deep knowledge of VA loans, FHA loans, commercial lending, jumbo loans, or luxury real estate. |

| Real estate or financial advisory transition | Brokers who want broader advisory work beyond mortgage placement. | Additional credentials, licenses, or education depending on the target role. |

| Operations or compliance leadership | Detail-oriented brokers who prefer systems, process improvement, or regulatory oversight. | Knowledge of workflows, audits, documentation, staff training, and policy implementation. |

Some brokers eventually move into technology, cybersecurity, or information risk roles because mortgage businesses handle sensitive financial data. If that direction interests you, Research.com’s guide to information security manager requirements may help you compare a different professional track.

How can brokers improve operational efficiency?

Operational efficiency is a major competitive advantage in mortgage brokerage because clients and referral partners value speed, accuracy, and transparency. A broker who can collect documents quickly, communicate clearly, resolve lender conditions, and keep files moving is more likely to earn repeat business and referrals.

Practical ways to improve brokerage operations

- Standardize intake: Use a consistent borrower checklist so every file starts with the right information.

- Track every lead: A CRM can reduce missed follow-ups and help you understand which referral sources produce qualified clients.

- Create workflow stages: Define each step from first contact to closing so clients know what happens next.

- Measure bottlenecks: Review which steps slow files down, such as missing documents, lender conditions, appraisal delays, or unclear borrower communication.

- Use templates carefully: Standard emails and checklists save time, but they should still be customized for each borrower’s situation.

- Protect client data: Efficiency should never come at the expense of security or compliance.

Brokers who want formal training in scheduling, workflow design, and resource coordination may find accelerated online project management bachelor’s degree programs useful for building operations-focused skills.

How can you future-proof a mortgage brokerage?

Future-proofing a brokerage means building a business that can adapt to changing mortgage rates, housing demand, technology, regulations, and consumer expectations. The most resilient brokers do not rely on one lender, one referral source, one marketing channel, or one outdated workflow.

| Risk | Why it matters | Better strategy |

| Depending on a single referral source | If that partner slows down or leaves, your pipeline can drop quickly. | Build multiple relationships across real estate agents, builders, financial advisors, and past clients. |

| Ignoring regulatory changes | Compliance mistakes can threaten your license and reputation. | Schedule CE early and monitor state and federal updates. |

| Using outdated technology | Slow systems can frustrate clients and referral partners. | Adopt secure tools for CRM, document collection, loan tracking, and reporting. |

| Competing only on rates | Borrowers may leave when another provider appears cheaper. | Compete through education, responsiveness, lender access, and problem-solving. |

| Failing to specialize | A generalist message can be hard to differentiate in crowded markets. | Develop expertise in a borrower segment, loan type, or property niche. |

Strategic education can also help brokers who want to lead teams, manage risk, and scale operations. An online MBA degree may be worth considering if your goal is business ownership, leadership, or long-term growth planning.

How do you start a mortgage brokerage?

Starting a mortgage brokerage requires both professional readiness and legal compliance. You need licensing, a compliant business structure, lender relationships, technology, operating procedures, and a plan for generating clients. Do not launch before checking your state’s exact requirements.

- Build industry experience first. Learn loan origination, borrower documentation, lender guidelines, compliance expectations, and client communication before taking on the risk of ownership.

- Complete licensing requirements. Finish pre-licensing education, pass the NMLS exam, and satisfy your state’s mortgage broker licensing rules.

- Select a legal structure. Decide whether to operate as a sole proprietorship, LLC, or corporation, then register the business as required.

- Obtain an EIN and complete state filings. Follow federal and state business registration steps, including name registration when applicable.

- Secure a mortgage broker bond. Confirm the bond amount and renewal requirements for your state.

- Submit the necessary applications and approvals. File licensing documents, background checks, financial information, and any state-required business materials.

- Create lender and referral relationships. Build connections with lenders, real estate agents, title companies, builders, financial advisors, and past clients.

- Choose technology carefully. Set up a secure loan origination system, CRM, website, digital document process, and compliance recordkeeping system.

- Document your workflow. Create procedures for intake, disclosure, document review, status updates, file submission, issue resolution, and closing follow-up.

- Plan for marketing and cash flow. Budget for licensing, bonds, software, insurance, lead generation, professional services, and slower early months.

Questions to ask before opening a brokerage

- Which state agency regulates mortgage brokers where I plan to operate?

- What bond, net worth, background check, or entity requirements apply?

- Which lenders will work with my brokerage, and what approval standards do they use?

- How will I generate leads without violating advertising or consumer protection rules?

- What system will I use to protect borrower documents and sensitive financial data?

- How much cash reserve do I need before revenue becomes consistent?

- Will I hire processors, assistants, loan originators, or compliance support?

Mortgage broker vs. loan officer: what is the difference?

Mortgage brokers and loan officers both help borrowers pursue real estate financing, but they operate under different business models. The key difference is whom they represent and which loan products they can offer.

| Role | Who they work for | Loan options | Best fit for borrowers who... |

| Mortgage broker | Acts as an intermediary between borrowers and multiple lenders. | Can compare products from different lending sources, depending on the broker’s network. | Want help shopping across lenders or have a situation that may require more than one option. |

| Loan officer | Works for a specific bank, credit union, or lending institution. | Offers the loan products available through that employer. | Already trust a specific institution or want a direct path through one lender. |

The US Bureau of Labor Statistics (BLS) notes that loan officers often work with residential and commercial loans and may develop business through relationships with real estate firms and other referral sources. A mortgage broker may offer broader lender comparison, while a loan officer may provide a more direct connection to one institution’s products. Neither option is automatically better; the right choice depends on the borrower’s goals, qualifications, and preference for comparison shopping versus working directly with a lender.

What do mortgage brokers say about their career journey?

-

: "

Working as a mortgage broker gave me the independence to build a business while helping families move toward homeownership. Each closing feels meaningful because clients are often reaching a major life goal. I entered the field without prior experience, but mentorship and steady learning helped me grow into the role. Samantha

"

-

: "

I moved from banking into brokerage because I wanted more control over my schedule and income potential. The work is demanding, but it improved my negotiation skills and taught me how to explain complicated lending details clearly. Strong relationships with clients and lenders became the foundation of my business. Raymond

"

-

: "

My business started with a small local client base and eventually expanded statewide. The most rewarding part is the trust I have built with realtors, repeat borrowers, and referral partners. The work changes constantly, but guiding people through major financial decisions keeps it worthwhile. Elena

"

Can an MBA help mortgage brokers lead and scale?

An MBA is not required to become a mortgage broker, but it can be useful for brokers who want to move beyond individual production into ownership, leadership, strategy, recruiting, operations, finance, or market expansion. The value is strongest when the degree supports a clear business goal, such as opening a brokerage, managing a team, improving profitability, or building a more data-driven growth strategy.

An advanced business degree may help brokers think more systematically about pricing, risk, marketing, process design, customer acquisition, and financial planning. If speed and flexibility are priorities, you can compare options such as the fastest online MBA programs.

Common mistakes to avoid when becoming a mortgage broker

- Assuming licensing is the same in every state: State rules differ, so always verify requirements where you plan to work.

- Choosing education based only on speed: A fast program may be convenient, but it should still teach skills you will actually use.

- Waiting until the last minute for continuing education: Missed CE or renewal deadlines can interrupt your ability to work legally.

- Underestimating sales work: Mortgage brokerage requires consistent outreach, follow-up, and relationship building.

- Focusing only on salary averages: Commission-based income can vary, and high averages do not guarantee individual earnings.

- Neglecting compliance documentation: Poor recordkeeping can create legal, financial, and reputational problems.

- Buying software without fixing workflow: Technology helps only when paired with clear processes and staff discipline.

- Opening a brokerage too early: Ownership requires capital, lender access, compliance systems, and operational maturity.

Key Insights

- The mortgage brokerage services market is projected to reach $151.6 billion by 2028, growing at an annual rate of 10.3%, but opportunity still depends on licensing, market conditions, and business execution.

- You can enter the field with a high school diploma or GED, but many brokers pursue college education; Zippia reports that 64% of mortgage brokers in the US hold a bachelor’s degree.

- The core licensing path includes 20 hours of NMLS-approved pre-licensing education, the NMLS exam, state registration, a mortgage broker bond, and an approved license application.

- Indeed reports an average US mortgage broker salary of $173,041 per year, including commissions and bonuses, but individual income varies by location, experience, specialization, and lead generation.

- Zippia projects about 12,600 new mortgage broker positions by 2028, with a projected growth rate of 4%, and reports 25,510 mortgage brokers currently employed in the US.

- Southfield, MI has the highest salary listed in the city data at $170,345 annually, followed by Miami, FL at $161,634 and Atlanta, GA at $141,017.

- Technology can improve speed and client service, but brokers still need compliance discipline, ethical judgment, secure data handling, and strong borrower communication.

- Opening a brokerage is best suited for licensed brokers who already understand lending operations, have referral relationships, can manage compliance, and have enough capital to handle startup costs and income variability.

References:

- BLS. (2025, April 18). Loan officers. BLS.

- Indeed. (2025, April 19). Mortgage broker salary in United States. Indeed.

- Research and Markets. (2025, January 6). Mortgage Brokerage Services Industry Report 2024-2033, Competitive analysis of JPMorgan Chase & Co, Federal National Mortgage Association, Wells Fargo, Fairway Independent Mortgage, & Rocket Mortgage. GlobeNewswire News Room. globenewswire.com.

- Zippia. (2025, January 8). Best colleges and degrees for mortgage brokers. Zippia.

- Zippia. (2025, January 8). Mortgage Broker Demographics and Statistics [2025]: Number of mortgage brokers in the US. Zippia.

- Zippia. (2025, January 8). Mortgage Broker skills for your resume and career. Zippia.

Other Things You Should Know About Becoming a Mortgage Broker

To become a successful mortgage broker in 2026, one must typically complete pre-licensure education, often around 20 hours of coursework, pass the National Mortgage Licensing System (NMLS) exam, and complete any state-specific requirements. Continuous education is crucial to stay updated with industry regulations and market trends.

The job outlook for mortgage brokers in 2026 remains steady, primarily due to consistent demand for housing and refinancing options. However, technological advancements and increased competition may influence job growth, requiring brokers to enhance digital skills and service offerings to meet market demands.