65 Student Loan Statistics: 2026 Data, Trends & Predictions

Co-Founder and Chief Data Scientist

Most high-paying jobs today require a college degree. If not, one has to have many years of experience before attaining such, especially if the job is at a managerial level. With a bachelor’s degree, one can look forward to earning around $30,000 more than their high school graduate counterparts. Other than banking more earnings, a college diploma also means there are more job opportunities, thus there are fewer unemployed individuals who have a college degree, an unemployment rate of 2.5%.

However, the cost of a college education has steadily increased over the last several years. As it continues to rapidly rise, so do student loan debts, which have reached "disquieting record levels for both graduates and governments" (Chamie, 2017).

This article lays down the crucial facts and figures that shape the trends revolving around the growing debt of students and graduates. It aims to help students make wiser decisions before taking out a student loan. This article may also assist other readers who wish to better understand how the rising student loan debts impact the nation’s people and economy.

The Rising Cost of Higher Education in the USA

The U.S. is among the world’s most popular destinations for quality higher education. However, it is also one of the most expensive. Higher education costs are among the fastest rising in today’s American society. This is in stark contrast to Europe, as there are European countries with free college whose quality can hold their own against American counterparts.

- The College Board reported that the 2025-2026 tuition and fees in public 4Y universities was $11,950 for an in-state student. Non-resident tuition and fees cost $31,880.

- Meanwhile, private nonprofit 4Y institutions charged $45,000 for tuition and fees, and public 2Y institutions charged $4,150.

- Over a ten-year period, tuition and fees in public 4Y and 2Y institutions has decreased by 7% and 10%, but it has increased 2% for private nonprofit institutions.

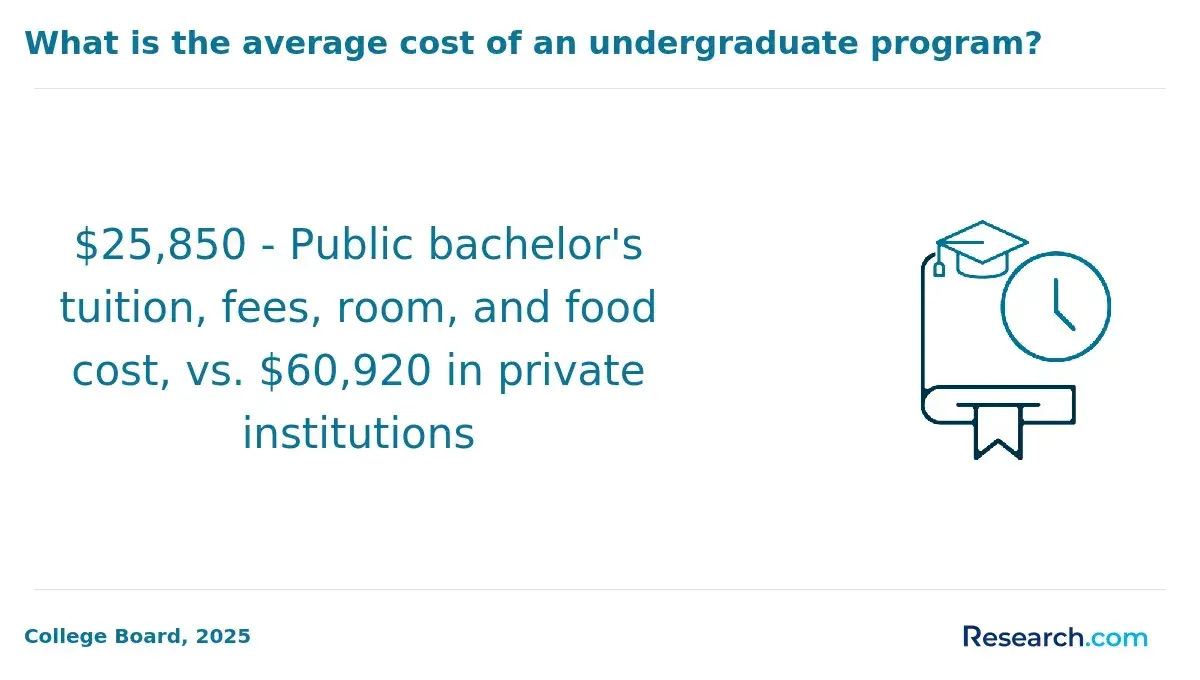

The Average Cost of an Undergraduate Degree in the U.S.

For any student looking to get quality higher education in the U.S., they should look at these figures to get an idea of how much it will cost them to earn a U.S. degree.

- In the USA, tuition fees range between $5,000 and $50,000 per year. For example, if one wanted to have a geography job in the future, they have to shell out between $20,000 and $50,000 per year for a degree.

- After financial aid, students in public 4Y institutions would pay $21,340.

- Meanwhile, in private nonprofit universities, students would pay $37,380 after aid.

- In public 2Y institutions, this amounted to $15,980.

Non-Tuition Costs That Add to College Students’ Expenses

Studying comes with other costs besides tuition fees. These are the top non-tuition costs U.S. students often encounter.

- Housing and food for community college students cost around $10,850.

- Public university students pay an average of $13,900 for housing and food.

- Meanwhile, private nonprofit university students pay more, at $15,920.

- Transportation cost around $2,000 for community college students.

- In comparison, public 4Y university students pay around $1,380, and private university students pay $1,190.

- Course materials for all types of institutions cost an average of $330.

- Other supplies vary, with public 2Y institutions charging $1,240.

- Then, supplies in 4Y institutions cost around $1,000.

Student Debt Increase

Now that the cost of getting a college degree in the USA has been established, it is time to look at how most students fund their education: student loans. Student debt has been increasing in the past several years as education costs also continue to rise. However, unlike other types of debts, a student loan cannot be easily discharged by filing bankruptcy based on federal rules. Here are some striking data.

- 22% of students in the U.S. have debt amounting between $20,000 to $39,999 in 2025.

- Meanwhile, 21% of students owed $10,000 to $19,999.

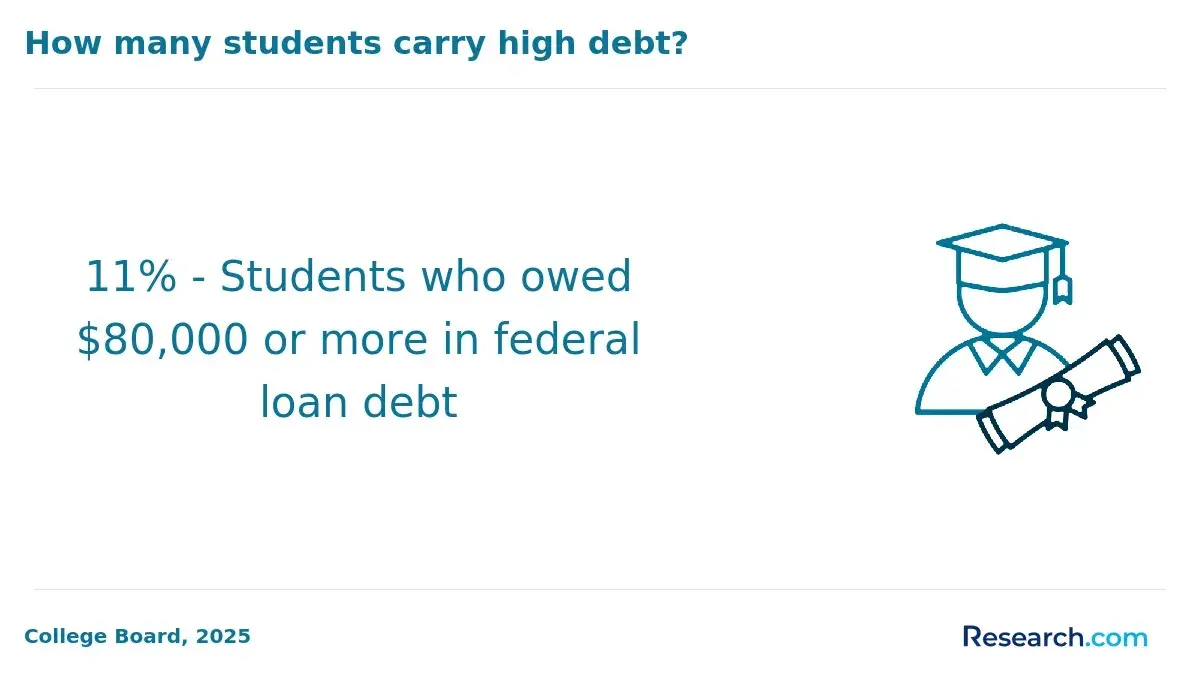

- 6% of students possessed a debt of around $100,000 to $199,999.

- Only 2% of students owed more than $200,000 of debt.

The Extent of Student Loan Debts

Below are more statistics that show the extent of student loan debts.

- 42.8 million students owe federal student debt.

- Public university students typically borrow $31,960 to earn a bachelor's degree.

- As of Q1 2026, total outstanding debt is $1,696.3 bn.

- Federal Direct Loans account for the highest share of student aid, accounting for $1,534.0bn in 2026.

- Among age groups, those aged 35 to 49 have the highest debt, totaling to $681.5bn.

- They are followed by those aged 25 to 34, with a total debt of $472.8bn.

- 3.56 million borrowers owe between $20K to $40K of debt, amounting to a total outstanding debt of $100.81bn.

- Meanwhile, 0.11 million borrowers owe between $40K to $60K of debt, amounting to a total outstanding debt of $5.27bn.

Student Loan Debt By Education Level and Discipline

It is also worth noting that it is not just undergraduate students who finance their studies through student loans.

- Undergraduate students have an average debt of $25,670.

- Master's degree-holders owe a debt of around $69,140.

- PhD-holders possess about $72,560 of debt.

- Law graduates owe around $140,870 of debt.

- Medical students, on the other hand, have a debt of $199,220.

Student Loan Debt By Institution

Student loan statistics vary from institution to institution, and concerned stakeholders can better grasp the state of education financing by looking at these figures and facts.

- As of February 2026, there are more borrowers from public institutions, at 8,922,300.

- Meanwhile, there were 5,070,400 private nonprofit borrowers.

Furthermore, many students dream of attending leading universities in the United States. Unfortunately, these institutions are also among the most expensive. Although most of the universities have programs that help ensure students graduate with as little debt as possible, many students still graduate with a considerable amount of debt.

- The average debt of Princeton University students is $9,059.

- Harvard University student borrowers owe an average of $13,372.

- Meanwhile, Yale University students have a cumulative student loan average of $14,575.

Student Loan Data By State

Student loan amount averages also vary depending on location. Here are the latest figures.

- The top states with the highest average student loan debt were: $43,781 in Maryland, $42,226 in Georgia, $40,287 in Virginia, $39,574 in Florida, and $39,042 in Illinois.

- The District of Columbia also has a high average loan debt, at $54,561.

- North Dakota has the lowest average student loan debt per student, at $29,115.

Student Loan Data By Type of Loan

There are various types of student loans available in the United States. These come in varying repayment and interest structures. The U.S. Department of Education oversees the disbursement of student financial aid in the form of these loans.

As of Q1 2026:

- Stafford Subsidized: $297.8bn

- Stafford Unsubsidized: $628.8bn

- Stafford (Combined): $926.6bn

- Grad PLUS: $124.7bn

- Parent PLUS: $114.9bn

- Perkins: $2.8bn

- Consolidation: $527.3bn

Student Loan Default, Delinquency, and Forgiveness

Unfortunately, not all those who graduate with student loan debt are able to repay their loans as planned and scheduled. Here are figures related to student loan default, delinquency, and forgiveness.

- 30% of students with an associate or technical degree are behind on their payments.

- Meanwhile, 11% of bachelor's degree graduates and only 8% of graduate degree holders are behind on their payments.

- Borrowers from public institutions have a nonrepayment rate of 15%. Private institution graduates have a nonrepayment rate of 14%.

- In comparison, proprietary institution graduates have a higher nonrepayment rate of 32%.

- 1.28 million borrowers are recorded delinquent for 31-90 days.

- 1.18 are delinquent for 91-180 days.

Alternatives to Federal Student Loans and Their Impact

While federal student loans remain the primary source of funding higher education for many, they are not the only option available to U.S. students. Private loans and scholarships are increasingly becoming significant alternatives. Private college loans, in particular, play a crucial role in bridging the financial gap for students who do not qualify for sufficient federal aid or need additional funding for tuition, living expenses, or other education-related costs. These loans, offered by private lenders, often come with variable interest rates and flexible repayment terms but require a strong credit history or a co-signer.

Understanding these alternatives is essential for students looking to make informed decisions about financing their education. For more details, explore the best options for private college loans and how to utilize them effectively to minimize debt while pursuing your academic goals. Proper financial planning and exploring all available funding sources can empower students to focus on their education without undue financial stress.

What are the long-term financial implications for borrowers?

Long-term student loan obligations affect personal financial planning through delayed home ownership, reduced savings capacity, and postponed retirement preparations. Persistent debt accumulation and interest can constrain credit access and limit investment opportunities. Assessing sustainable repayment strategies and refinancing options is essential to counteract these economic challenges. Furthermore, when evaluating overall educational investments, consider how much is vet school as a benchmark for understanding the broader financial commitments in various professional fields.

What are effective strategies to manage student loan debt?

Effective debt management focuses on structured repayment plans, refinancing options, and alternative education pathways that lower upfront costs. Analyzing individual financial profiles and carefully comparing refinancing offers can secure reduced interest rates and flexible terms. Additionally, exploring education models that emphasize affordability, such as self-paced online colleges, may present opportunities to complete studies at a lower overall expense.

Is a college degree a smarter investment than an associate degree?

Evaluating educational pathways is critical for managing rising tuition costs and mitigating long-term debt burdens. An individual’s choice between pursuing a longer, comprehensive academic track and a shorter, more affordable program can significantly influence future earnings and financial stability. In-depth comparisons between these educational models are available in our analysis of college degree vs associate degree, which examines return on investment and career trajectory differences. This review helps stakeholders determine the optimal balance between immediate affordability and long-term economic benefits.

What are the long-term benefits of investing in high ROI degree programs?

Choosing a degree with strong long-term returns can provide a strategic advantage in managing student loan burdens. High return on investment (ROI) programs often lead to greater lifetime earnings, enabling graduates to more effectively address their repayment obligations. In addition, a focus on these programs supports sustainable financial planning by improving access to higher-paying opportunities, which can offset the high initial costs associated with higher education. For an in-depth look at potential academic routes, consider exploring our guide on the best paying degrees.

What are the recent policy changes affecting student loans?

Recent regulatory and legislative measures have introduced updates that aim to ease repayment pressures and expand borrower relief. Recent reforms include adjustments to income-driven repayment plans, enhanced transparency in loan servicing, and broadened eligibility for targeted forgiveness programs. These initiatives are designed to offer borrowers more predictable repayment options and to improve access to refinancing opportunities, which many consider alongside alternative educational routes such as accelerated college programs.

How can parents with bad credit explore viable student loan options?

Parents facing credit challenges may benefit from specialized funding solutions designed to ease the burden of financing education. Lenders offering student loans for parents with bad credit tailor their underwriting criteria to accommodate unique financial circumstances, often emphasizing overall stability and repayment capacity over traditional credit history. Evaluating distinct repayment terms, interest rates, and associated fees is crucial to ensure these options align with long-term financial strategies. Consulting with a financial advisor can provide additional insights into effective debt management and alternative financing avenues.

How can borrowers secure last-minute student loans for urgent needs?

When unexpected financial challenges arise, borrowers may need rapid funding without jeopardizing long-term financial stability. Evaluating emergency financing solutions should involve a review of one's credit profile, comparing transparent offers, and consulting professional advice. Some lenders specialize in rapid funding options, including quick student loans, which can provide timely relief while maintaining manageable repayment terms. This approach requires careful risk assessment and cost-benefit analysis to ensure that short-term aid aligns with overall debt management strategies.

Can Accredited Online Education Reduce Student Loan Debt?

Accredited online education offers a cost-effective alternative to traditional campus-based programs by minimizing non-tuition expenses and providing flexible learning schedules that help manage work and study commitments. Research indicates that choosing an accredited online degree can reduce overall education costs, potentially limiting the amount needed in student loans. For further verified information on quality education options, review what online colleges are nationally accredited. This approach provides students with a strategic means to alleviate financial pressures while maintaining competitive academic outcomes without compromising institutional integrity.

How Can Enhanced Financial Literacy Improve Student Loan Repayment Strategies?

Greater financial literacy equips borrowers with clear insights into interest accrual, repayment options, and the long-term financial implications of their choices. By understanding the nuances of structured repayment, refinancing, and consolidation, students can tailor strategies that align with their financial profiles and minimize overall debt burdens. Leveraging professional resources and government programs focused on financial education further enables informed decision-making. Additionally, students might consider cost-effective education pathways such as easy online degrees to get, which can help reduce future reliance on substantial student loans.

Student Loan Repayment Facts and Figures

Students take out loans to finance their studies in the hopes that their education will eventually help them land their dream jobs, get hired for high-paying positions, or establish their own practices and businesses, which will then earn them enough to repay their loans. However, it is not very easy for the majority of borrowers. Here are some related facts and statistics.

- Around 14.13 million borrowers are currently in repayment status as of Q1 2026.

- 2.65 million Direct Loan borrowers are under the Income-Based repayment plan.

- Meanwhile, 7.19 million are under the SAVE plan.

- 1.48 million are enrolled under the PAYE plan.

- 12.83 million Direct Loan borrowers are paying their plan in 10 years of less.

Other student loan and funding insights and statistics:

- 38% of college funds of most Americans come from parents' incomes and savings, while 10% are from students' income and savings.

- 11% of college funds come from parent borrowing, and 12% are from student borrowing.

- 27% of college funds come from scholarships or grants.

- In 2024-2025, 52% of parents received the financial aid amount they expected, and 56% of students did. Only 6% of parents and students received more aid than they expected, and a total of 21% got less than what they expected.

- 44% of parents believed their income was too high, so they did not submit FAFSA in 2025-2026.

- 18% did not submit FAFSA due to lack of time.

Student Loan Debt Trends and Predictions

Student loan debt is a $1.6 trillion-issue, and it is disgruntling to think that this debt is shouldered by U.S. students and graduates who simply wanted to acquire quality education and enter the workforce with leverage. As both education costs and student debt rates rise, an action clearly needs to be taken.

The financial returns to investing in a four-year bachelor’s degree have significantly increased, compared to completing a two-year tertiary course or a secondary education. Simultaneously, however, the responsibility to finance college/university education has considerably shifted from federal taxpayers to the students and their families (Callan & Finney, 1997, as cited in Woo & Lew, 2020).

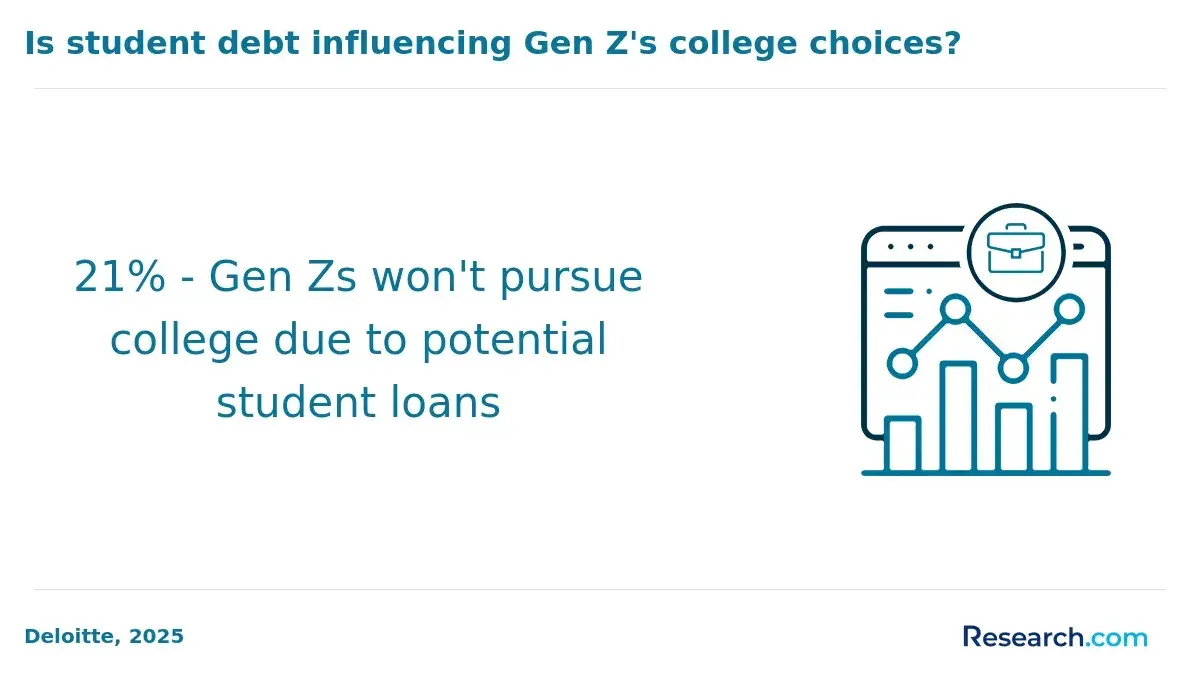

Americans’ opinions on whose fault is it that student loan debt continues to increase also vary. Older generations tend to put blame on the borrowers, while GenZers and Millennials see the government, lenders, and universities as responsible. Because of this, 39% of Gen Zs and Millennials forgo college due to financial constraints, and 21% of Gen Zs won't pursue college due to potential student loans (Deloitte, 2025).

Access to free public college emerges as the most popular solution to lower student debt. However, funding higher education through taxes, although standard in other countries, is unlikely to be practiced in the United States in the near future.

Furthermore, as the U.S. economy shrinks quickly, it is not difficult to see student loan default rates quickly climb. More than 26 million people in the U.S. have already filed for unemployment and it is highly likely that most of those people have outstanding student loan debt.

How are employers responding to the student loan debt crisis?

Employers are increasingly recognizing the impact of student loan debt on their employees' financial well-being and overall job satisfaction. Here's how companies are addressing this issue:

- Employer-Paid Student Loan Repayment Programs: Some companies are offering direct student loan repayment assistance as a benefit. Employers make monthly contributions towards an employee's student loan debt, helping to reduce the loan balance faster. For example, some companies offer payments of $50 to $200 per month towards employees' student loans.

- Student Loan Refinancing Partnerships: Employers partner with financial institutions to offer student loan refinancing options to employees. This can provide lower interest rates and more manageable repayment plans, helping employees reduce their monthly payments and overall interest costs.

- Financial Wellness Programs: Many organizations are expanding their employee benefits to include financial literacy and debt management resources. These programs often include workshops, one-on-one coaching, and tools to help employees create strategies for paying down student loan debt and improving their financial health.

- Tuition Assistance and Loan Forgiveness Programs: In addition to helping employees manage existing student loans, some companies offer tuition assistance for continuing education. There are also programs that forgive a portion of student loans for employees who commit to working at the organization for a certain period.

- Tax-Advantaged Student Loan Repayment Benefits: With recent legislative changes, some employers are taking advantage of tax incentives for student loan repayment contributions. For example, under the CARES Act, employers can contribute up to $5,250 annually towards an employee's student loans tax-free.

What are the financial aid options for cosmetology students?

Pursuing a cosmetology degree can be expensive, but various financial aid options are available to help aspiring cosmetologists manage the costs. Here are some practical solutions to reduce the financial burden:

- Federal Financial Aid: Complete the FAFSA (Free Application for Federal Student Aid) to determine eligibility for federal grants, loans, and work-study programs. Pell Grants, for example, can provide significant support without requiring repayment.

- Scholarships and Grants: Many beauty schools and professional organizations offer scholarships tailored to cosmetology students. Look into programs like the Beauty Changes Lives Foundation or local community grants.

- Private Loans: If federal aid doesn’t cover all expenses, consider private loans. Be cautious of interest rates and repayment terms when choosing a lender.

- Payment Plans: Some cosmetology schools offer in-house payment plans that allow students to spread tuition payments over time, often interest-free.

- Employer Sponsorships: Certain salons and beauty companies may sponsor education in exchange for a commitment to work with them after graduation.

- State-Specific Programs: Many states offer additional financial aid or loan forgiveness programs for students pursuing vocational training like cosmetology.

For more details on funding your education, explore our guide on student loans for cosmetology school, which provides comprehensive advice tailored to beauty school students.

Understanding these options can help aspiring cosmetologists access quality education without accumulating excessive debt, setting them up for a successful and financially stable career in the beauty industry.

U.S. Student Loan Debt Crisis: An Education and Economic Issue

There is no doubt that higher educational attainment brings forth a number of positive outcomes. This is why getting a college degree is important for individuals hoping to get better employment prospects and wages. Furthermore, having more educated citizens is also a good sign for a country’s stature and economy. Because of that, many students begin their steps toward college by considering dual enrollment vs AP.

However, as more students and graduates struggle to fund their education and pay off student loan debt, what does it say about the system in general? Are we brewing educated but financially-burdened citizens?

The student loan debt crisis in the USA is not merely an education issue. For the most part, it is an economic concern that can only be solved through cooperation and a genuine will to eradicate the problem.

Key Insights

- Significant Earnings Advantage: Individuals with a bachelor's degree can earn around $30,000 more than their high school graduate counterparts.

- Rising Education Costs: Over a ten-year period, tuition and fees in public 4Y and 2Y institutions has decreased by 7% and 10%, but it has increased 2% for private nonprofit institutions.

- Student Debt Crisis: There are around 43 million student loan borrowers in the U.S., collectively owing nearly $1.6 trillion in debt.

- Loan Default and Delinquency: 1.28 million borrowers are recorded delinquent for 31-90 days as of February 2026.

- Disparity in Loan Amounts by State: The District of Columbia has a high average loan debt, at $54,561.

- Graduate and Professional Degree Debt: Average debt for graduate school students is $71,000, with some professional degrees resulting in debts as high as $246,000.

- Economic Impact: The student loan debt crisis impacts the U.S. economy significantly, with many borrowers struggling to repay their loans amidst rising education costs and economic downturns.

- Public Perception and Solutions: Opinions on resolving the student loan crisis vary, with younger generations blaming the government and lenders, and older generations blaming borrowers. Free public college is a popular proposed solution, though its implementation is uncertain.

References:

- Chamie, J. (2017). Student Debt Rising Worldwide. Yale.

- Deloitte. (2025). 2025 Gen Z and Millennial Survey: Growth and the pursuit of money, meaning, and well-being. Deloitte.

- Federal Reserve System. (2025). Report on the Economic Well-Being of U.S. Households in 2024 - May 2025. Federal Reserve.

- Federal Student Aid. (2026). Federal Student Loan Portfolio. Federal Student Aid.

- Hanson, M. (2025). Average Student Loan Debt. Education Data Initiative.

- Hanson, M. (2026). Student Loan Debt Statistics. Education Data Initiative.

- Ma, J., Pender, M., & Hu, X. (2025). Trends in College Pricing and Student Aid 2025. College Board.

- Sallie Mae. (2025). How America Pays for College 2025. Sallie Mae.

- Statista. (2025). Average student debt of students at the top 20 U.S. universities in 2024. Statista.

- Woo, J.H., & Lew, S. (2020). Parent borrowing and college completion. Journal of Student Financial Aid, 49 (2). https://ir.library.louisville.edu/jsfa/vol49/iss2/4

Other Things You Should Know About Student Loan Statistics

In 2026, the average student loan debt for U.S. graduates is approximately $35,000. This figure reflects the continuous increase in tuition and associated educational expenses, impacting graduates' financial stability as they enter the workforce.

The cost of an undergraduate degree in the U.S. varies widely. The 2025-2026 tuition and fees in public 4Y universities was $11,950 for an in-state student. Non-resident tuition and fees cost $31,880.

Besides tuition, students incur expenses such as accommodation, food, utilities, internet service, phone service, transportation, and academic books and supplies. For instance, the annual average cost for room and board in U.S. public universities was $13,900.

The student loan debt crisis is substantial, with around 43 million borrowers collectively owing nearly $1.6 trillion. This debt burden affects not only individual borrowers but also the broader U.S. economy, contributing to financial stress and reduced economic mobility for many graduates.

The average student loan debt per borrower is $39,075. To gain a bachelor's degree, many students have a debt of $31,960.

As of 2026, 1.28 million borrowers are delinquent for 31-90 days. 1.18 million have been delinquent for 91-180 days, and 1 million have been delinquent for 271-360 days.

Undergraduate students have an average debt of $25,670. Master's degree-holders owe a debt of around $69,140, and PhD-holders possess about $72,560 of debt.

Student loan debt averages vary by state. The top states with the highest average student loan debt were: $43,781 in Maryland, $42,226 in Georgia, $40,287 in Virginia, $39,574 in Florida, and $39,042 in Illinois.

There are various types of student loans, including Stafford loans (subsidized and unsubsidized), Parent PLUS loans, Grad PLUS loans, and Perkins loans. Each type has different repayment and interest structures, managed by the U.S. Department of Education.

Common solutions include implementing free public college, increasing state funding for higher education, reducing tuition costs, expanding loan forgiveness programs, and improving financial literacy among students. However, there is debate over the feasibility and effectiveness of these solutions.